With frequent tariff disputes and intense price competition, the copper cathode rod market in 2025 has experienced multiple fluctuations, even witnessing zero or negative processing fees in mid-year. Now that half of 2025 has passed, how are downstream consumption and processing fees performing? What are the differences or similarities in the YoY operating rate performance in H1? Below is a summary of the semi-annual review of the copper cathode rod market:

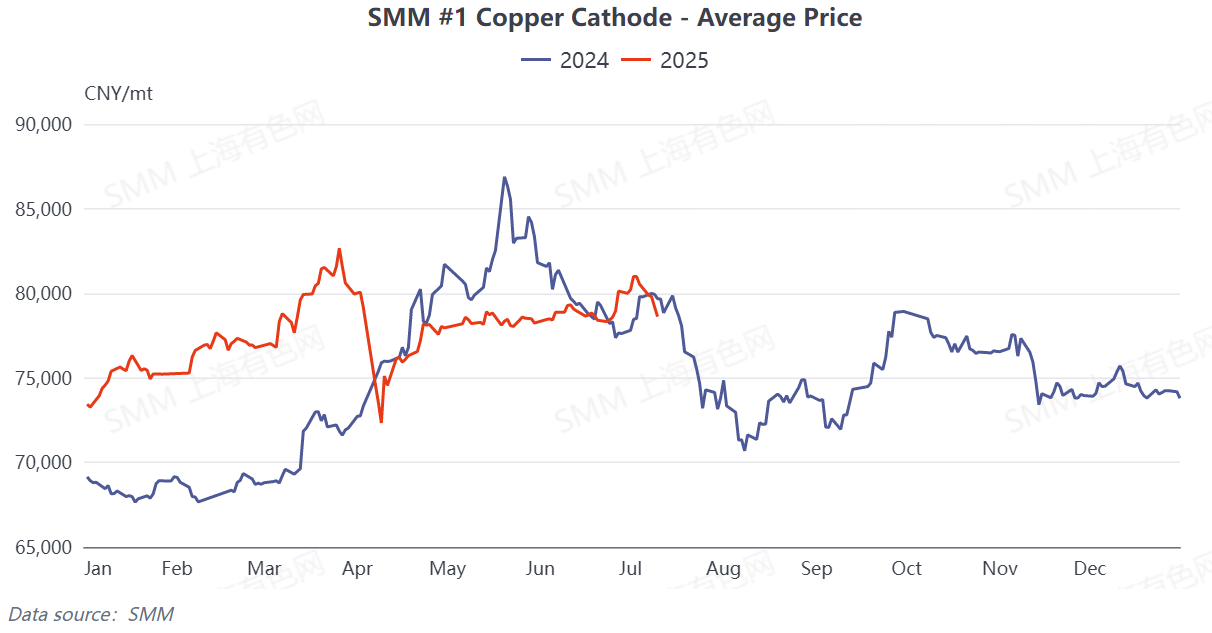

First, from the perspective of copper price trends in H1, the center of copper prices in Q1 2025 was significantly higher than that in the same period of 2024. However, since copper prices have been rising sharply since April last year, downstream industries have gradually become accustomed to the high copper prices. Additionally, Q1 includes the Spring Festival holiday, so there was no significant impact on the overall operating rate. The biggest difference in copper prices in 2025 was the limit-down trading in April, with a trend completely opposite to that in April 2024. This led to the early release of a large number of orders, and the production of orders on hand continued into April and early May. In contrast, last year, under the pressure of rising copper prices in April and May, a large number of orders were postponed, causing pressure on the operating rate.

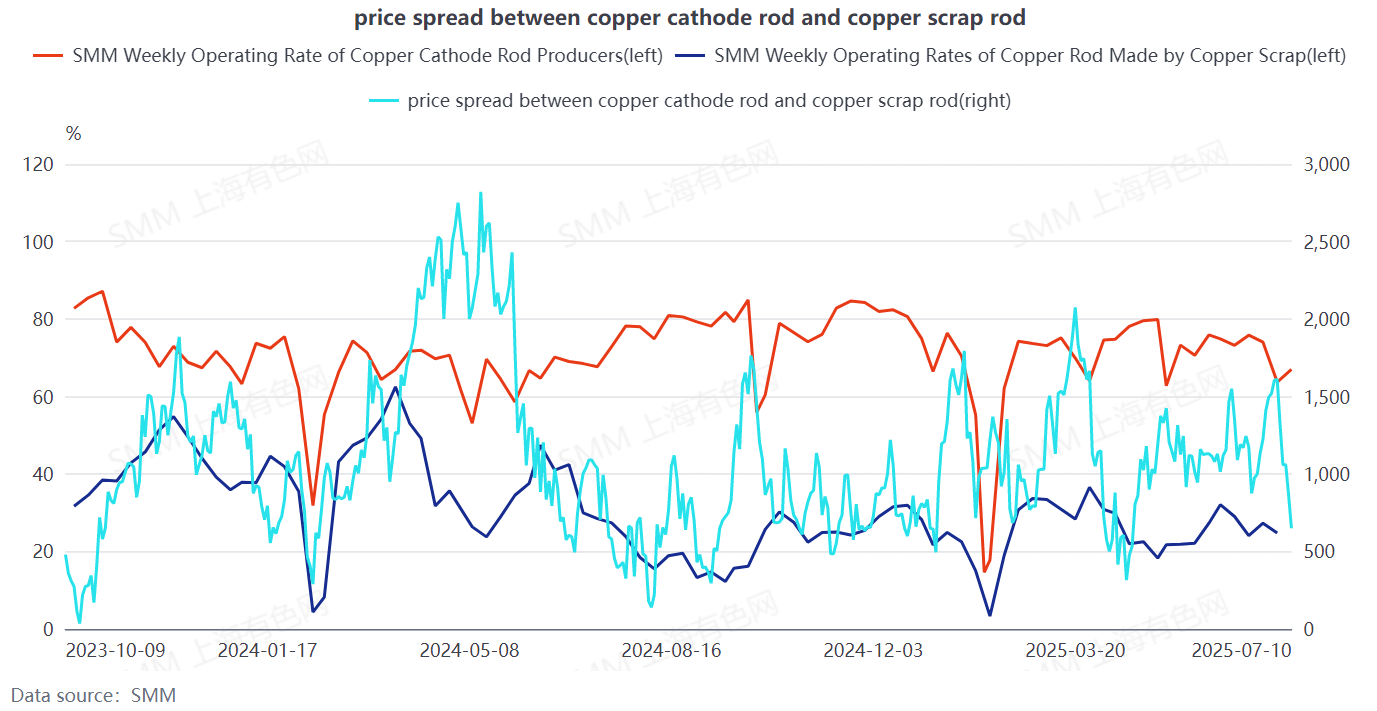

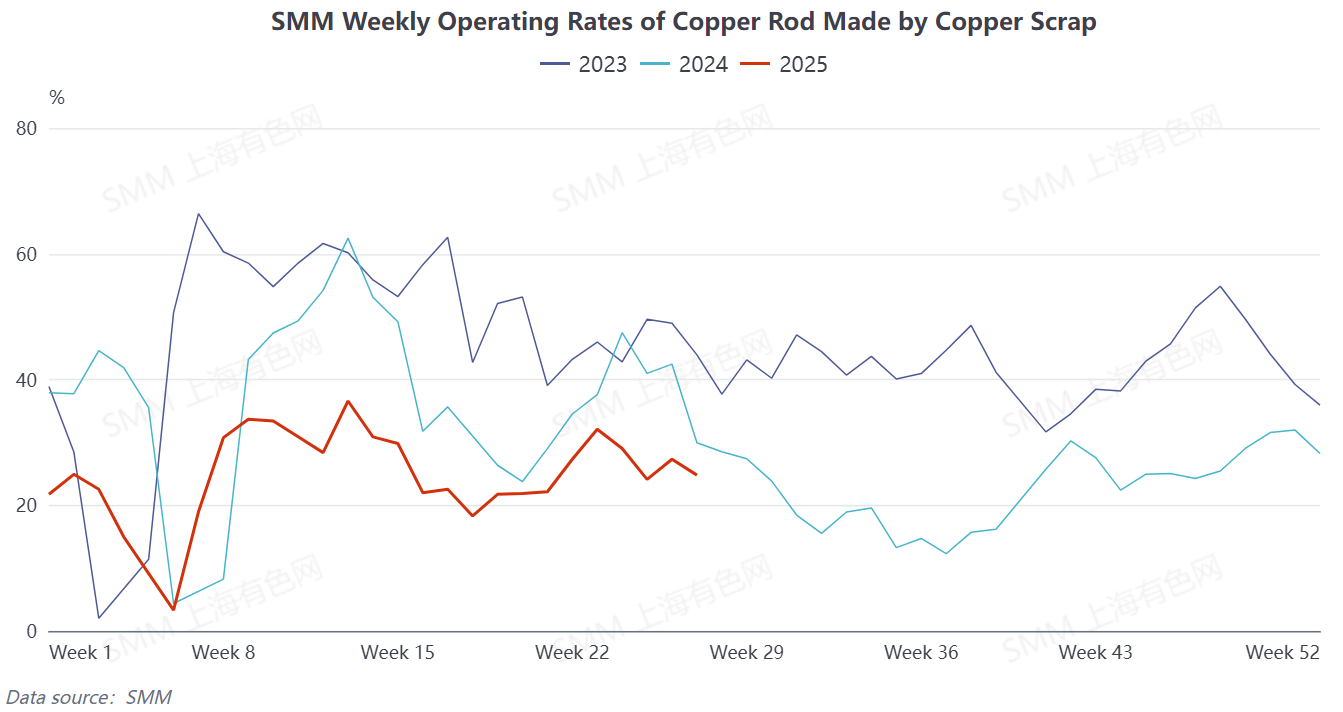

On the other hand, although for most of 2025, except for the limit-down trading in April, the price difference between primary metal and scrap was above 1,000 yuan/mt (as shown in Chart- above), making secondary copper rod more economically advantageous, due to the new policy being in the exploratory stage of implementation, there was a shortage of secondary copper raw material, and the operating rate of secondary copper rod plants remained at a low level compared to the same period, as shown in Chart- below:

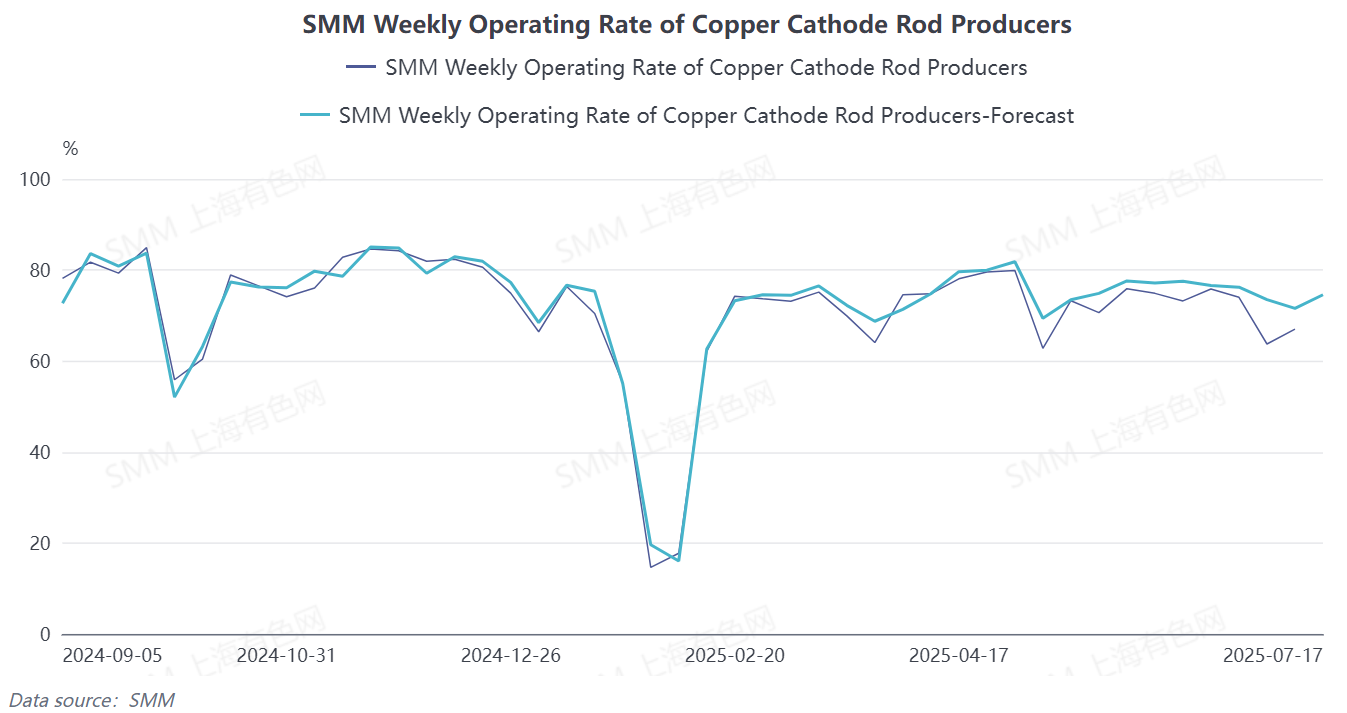

Therefore, although copper cathode rod had no price spread advantage, it was only slightly squeezed by secondary copper rod in the first half of the year. Ultimately, the average operating rate from January to June 2024 was 63.4%, and from January to June 2025, it was 65.63%, representing a YoY increase of 2.23 percentage points.

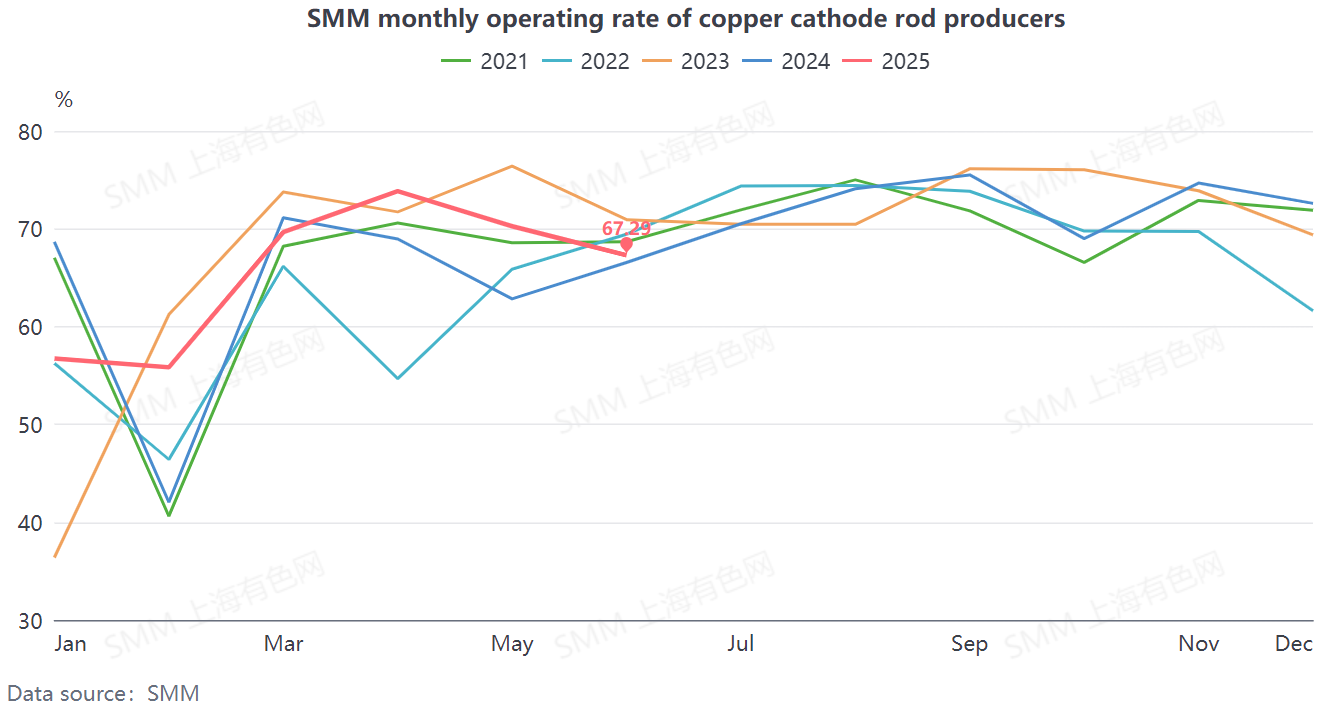

Looking specifically at Q2 2025, after a significant release of orders in advance in April, the monthly operating rate of copper cathode rod enterprises reached its peak in H1 in April, and subsequently declined month by month under the pressure of rising copper prices and the difficulty in securing new orders.

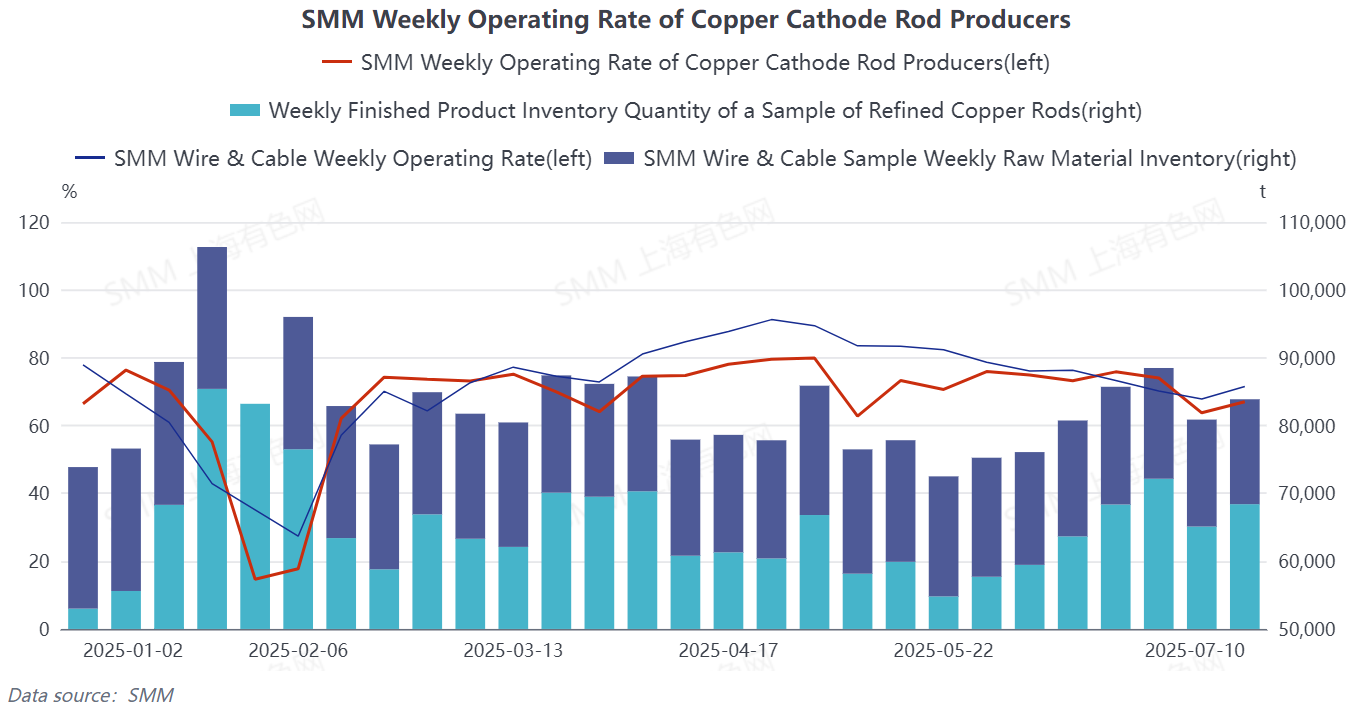

Looking specifically at the actual supply and demand situation of copper cathode rods in June, as June approached, the peak season gradually ended, and the weekly operating rate of downstream wire and cable enterprises continued to decline. Coupled with high copper prices and weak downstream consumption, the pace of cargo pick-up slowed down. At the same time, as the semi-annual period approached, a large number of copper cathode rod enterprises maintained high operating rates to meet their semi-annual targets. Against the backdrop of weakened demand and increased supply, the finished product inventories of copper cathode rod enterprises continued to build up. However, under the pressure of semi-annual targets, most copper cathode rod enterprises reduced their processing fees to maintain operating rates. Meanwhile, the deep involvement of traders exacerbated price competition in the copper cathode rod industry. Influenced by multiple factors in June, there were instances of zero processing fees and even negative processing fees.

Meanwhile, as can be seen from the above figure, under the continuous pressure of inventory buildup, in the first week of July, copper cathode rod enterprises significantly cut production and halted operations to destock. However, after resuming production, their finished product inventories rose again, indicating that the destocking pressure for copper cathode rod enterprises still existed in July.

Looking ahead, copper prices fell to 78,500 yuan/mt after breaking through the 80,000 yuan/mt mark in July, but according to SMM, copper cathode rod enterprises actually received fewer new orders, with most increases coming from previously provisionally priced orders and forward orders. The current pace of shipments remains under pressure, and the weekly operating rates of copper cathode rod enterprises continue to fall short of expectations. Most enterprises hold a pessimistic outlook for July, expecting the industry's overall operating rate to continue declining in July, reaching the lowest level for the same period.

In summary, supported by the early release of consumption in the first half of 2025 (H1), operating rates increased YoY. However, from a full-year perspective, the annual targets and profitability pressures of copper cathode rod enterprises are like a heavy burden. The increasing degree of overcapacity and changes in the supply chain model are both suppressing the enterprises' survival space. SMM predicts that by the end of 2025, the national copper cathode rod capacity will reach 18.292 million mt. Enterprises will face more severe overcapacity and losses in processing fees. SMM hereby calls on the industry to step out of price competition, find directions for self-improvement, and expand domestic and external demand channels.

![The Price Spread Between High-Quality Copper and Standard-Quality Copper Continued to Narrow, While SHFE Copper Spot Discounts Gradually Stabilized [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/YIaMU20251217171711.jpg)

![Inventory Continued to Decline, Suppliers Held Prices Firm Accordingly, and Spot Trades Were Better Than Yesterday [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/KtfdC20251217171713.jpeg)