SMM July 10 News:

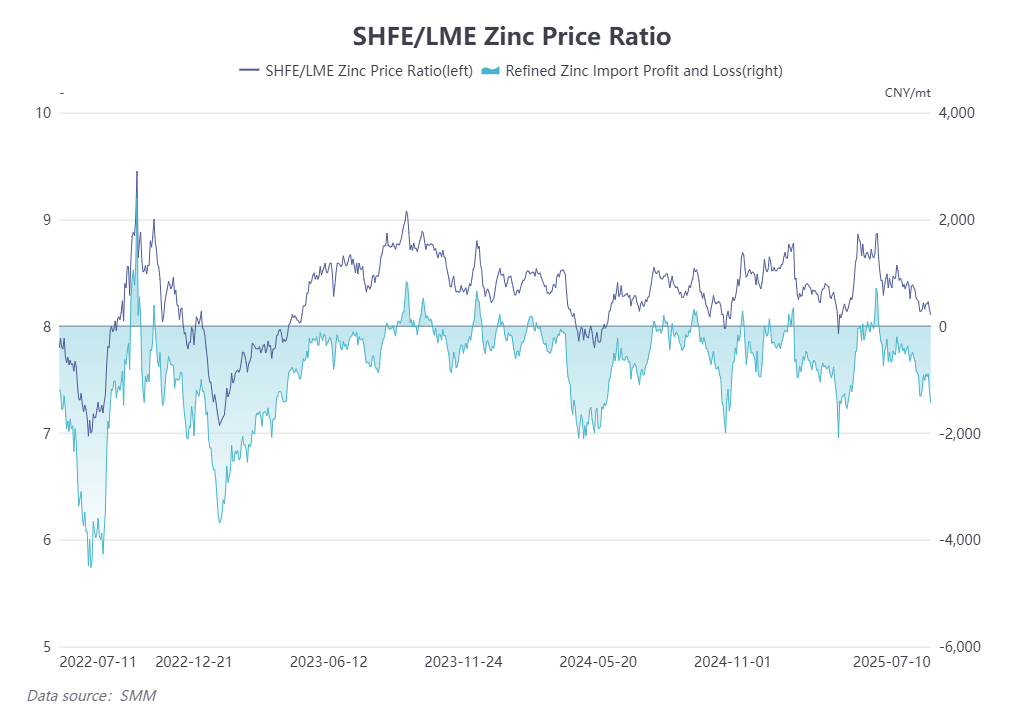

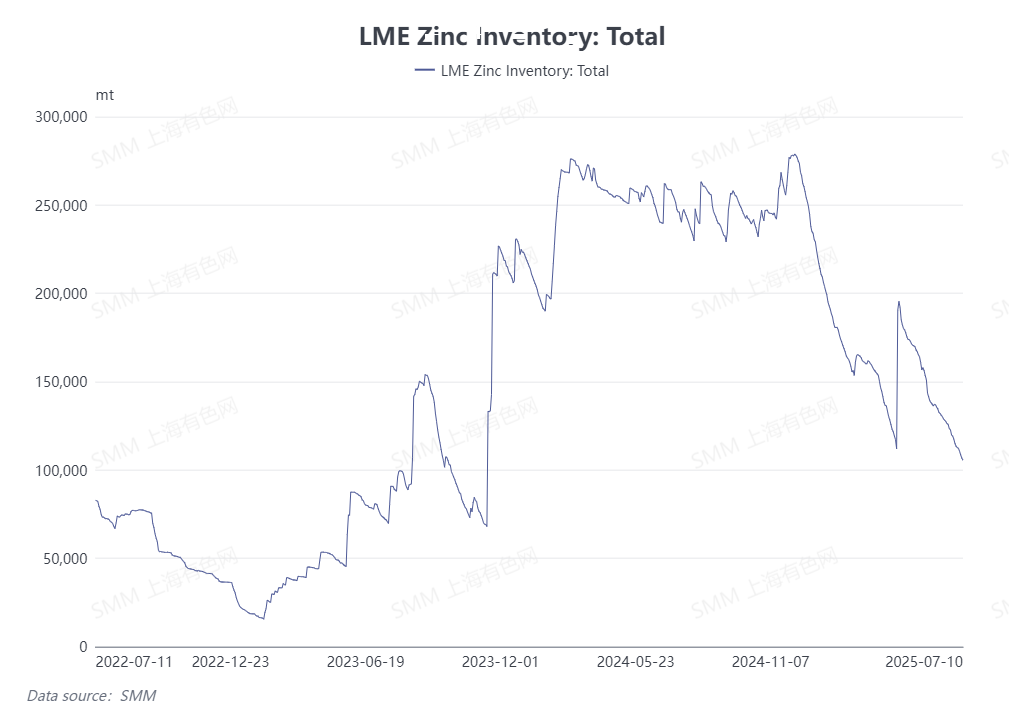

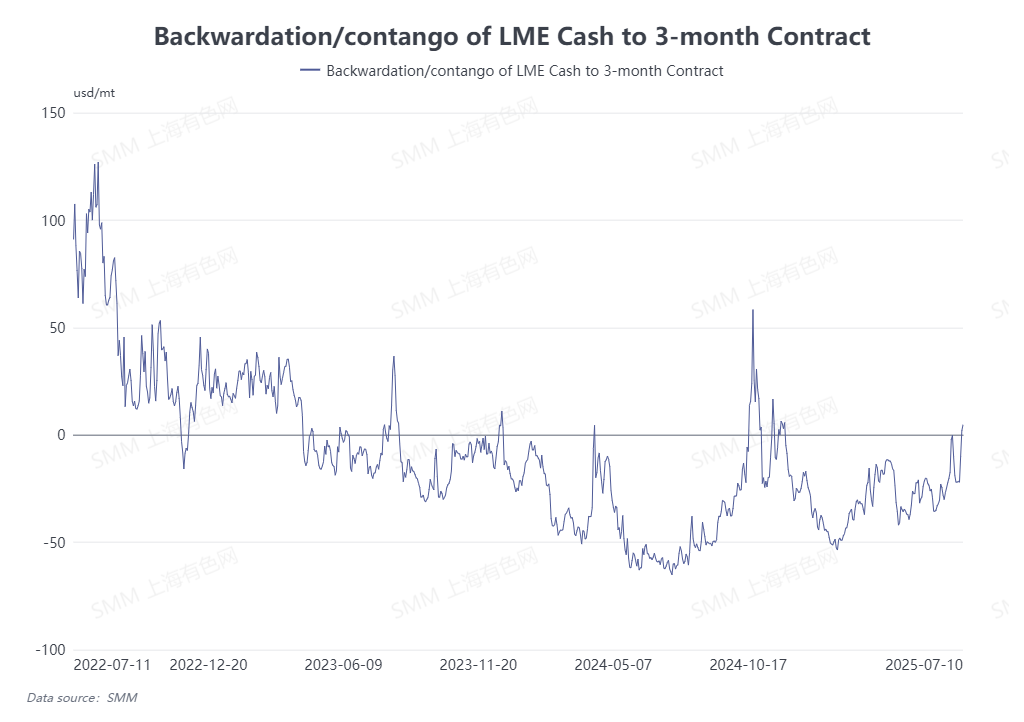

As of July 9, the total LME zinc ingot inventory stood at 106,700 mt, reaching a low since November 2023. Meanwhile, on July 9, the LME zinc 0-3 premiums and discounts rose to $1.96/mt, ending a six-month contango structure. In contrast, the recent price spread between futures contracts of SHFE zinc has narrowed significantly, highlighting the overseas market outperforming domestic market situation. The loss in zinc imports has continued to widen, raising market concerns about a potential "short squeeze" in LME zinc ingots.

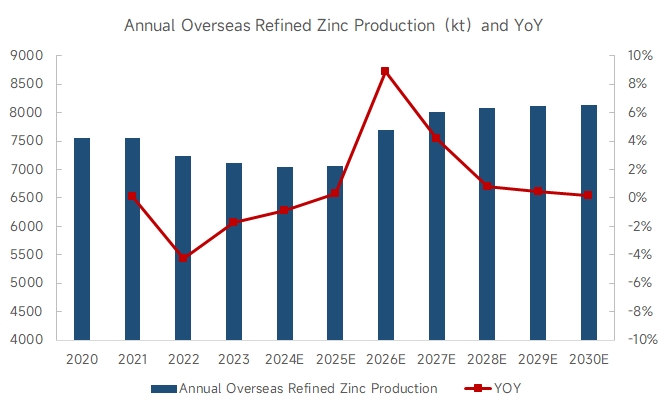

From the perspective of zinc ingot supply, this year's Asian zinc concentrate Benchmark was recorded at $80/dmt, hitting a new all-time low. Meanwhile, zinc prices have also declined YoY. Affected by the decline in processing fees and zinc prices, overseas smelters' production profits have contracted significantly, and overall market production enthusiasm has been weak. Additionally, in the first half of the year, some smelters in South Korea and Japan reduced or halted production, and Nyrstar's Hobart zinc smelter in Australia also announced a reduction of approximately 25% in production from April 2025. With ongoing supply disruptions, SMM predicts that overseas smelters will see no significant increase in production this year.

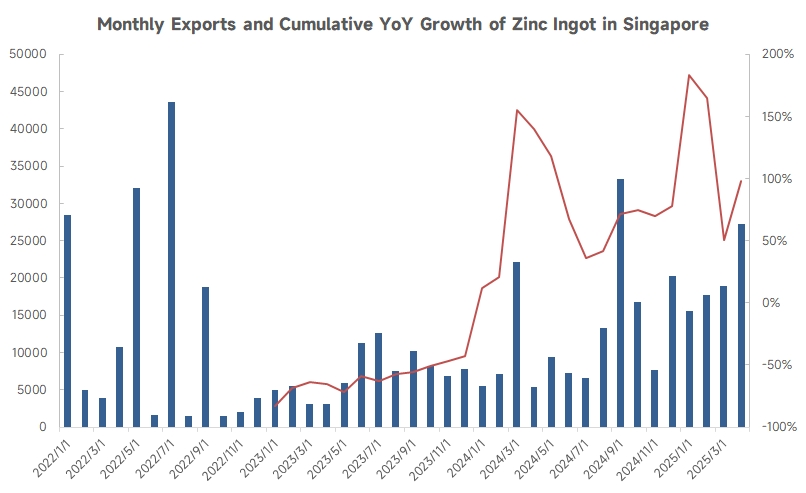

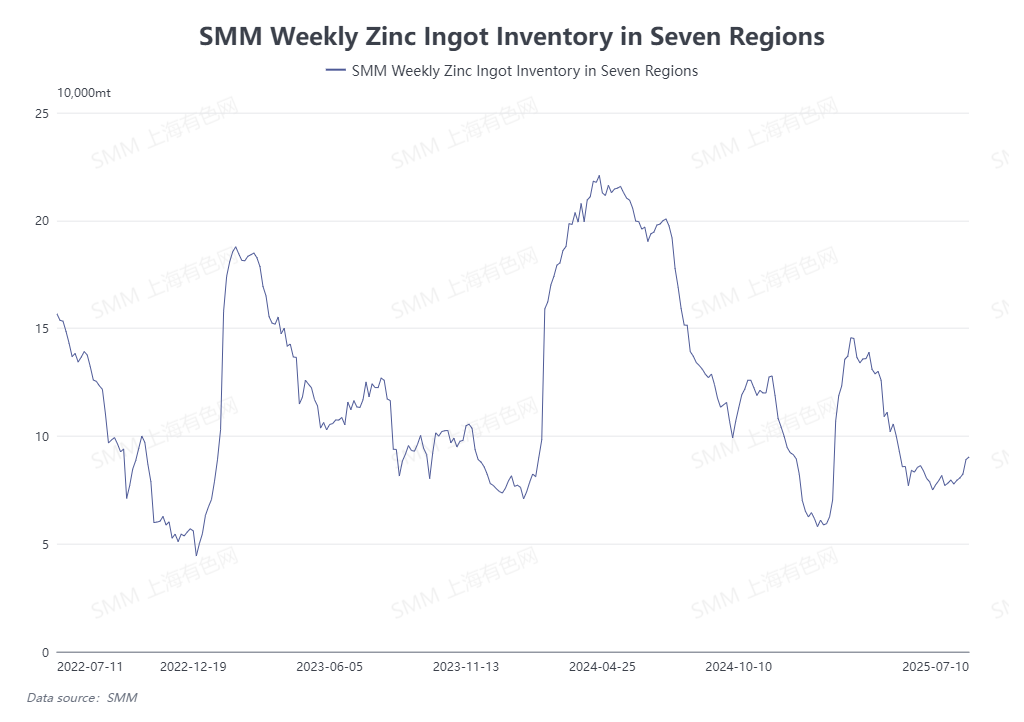

From the perspective of zinc ingot inventory, as of July 9, 2025, LME zinc ingot inventory has decreased from 234,100 mt at the beginning of the year to 106,700 mt, a total decline of 127,400 mt. Most of the inventory changes primarily originated from Singapore warehouses. According to trade map data, Singapore's cumulative zinc ingot exports from January to April 2025 reached 79,500 mt, up 98% YoY from 40,100 mt last year. Among them, Singapore's zinc ingot exports to Southeast Asia have increased significantly, indicating robust zinc ingot consumption in the region. Overseas zinc ingot demand remains strong, providing certain support to LME zinc prices.

Currently, China is in the off-season for consumption. Domestic zinc ingot inventory has started to build up since mid-June. With the gradual increase in production from domestic smelters and the weakening of downstream zinc consumption, SHFE zinc has been in the doldrums, hovering around 22,000 yuan/mt. In contrast, LME zinc prices have been relatively strong, supported by low inventory. Over the past two months, the SHFE/LME price ratio has declined rapidly, and the loss in domestic zinc imports has continued to widen, currently exceeding 1,000 yuan/mt.

Overall, overseas refined zinc production has shown little growth, coupled with the continuous decline in LME zinc ingot inventory. The overseas zinc market is exhibiting a "weak supply, strong demand" situation. If the downward trend in inventory continues, excessively low zinc ingot inventory may exacerbate the risk of a "short squeeze" in the overseas zinc market.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)