Cobalt is a critical metal resource that is widely used in various high-tech fields due to its unique physical and chemical properties. As global demand for high-performance materials continues to grow, the strategic importance of cobalt is becoming increasingly prominent. Gaining a deep understanding of cobalt mining, refining, and downstream application value chain helps to grasp its development trends in modern industry and emerging technologies, while also promoting the rational utilization of resources and sustainable development.

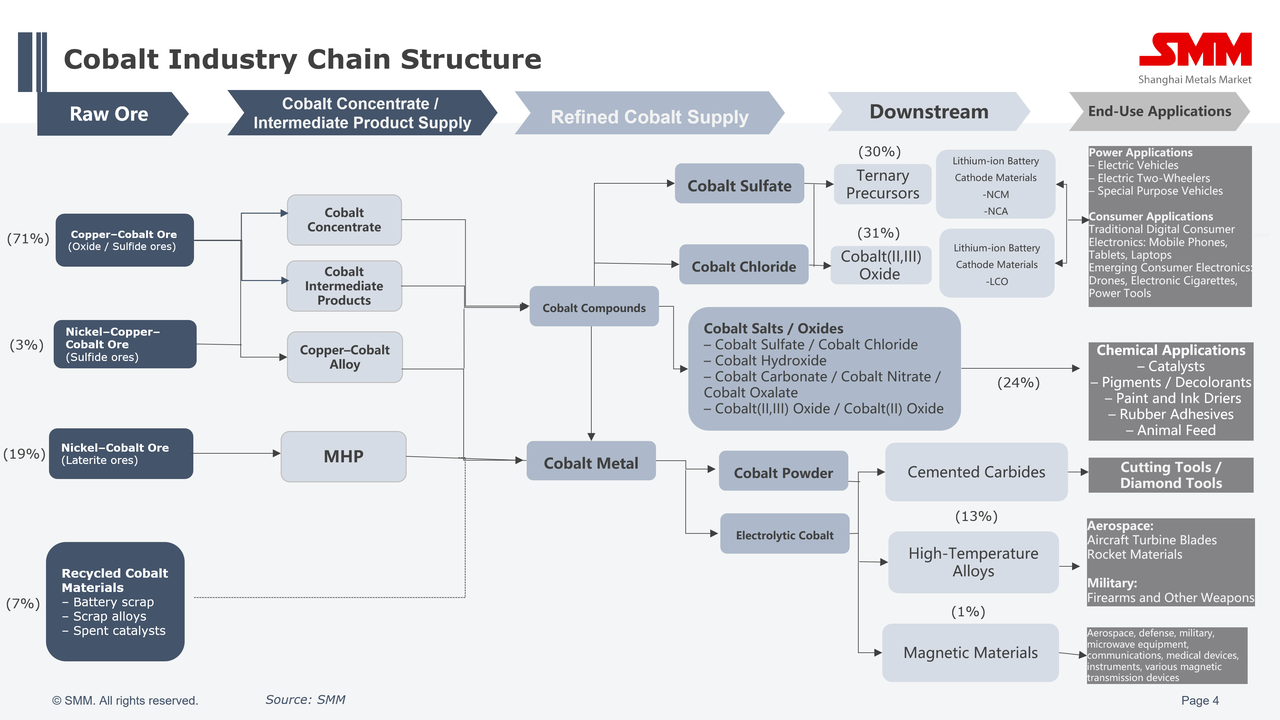

The cobalt industry chain is divided into the upstream mining sector, the midstream refining sector, and the downstream consumption sector.

The cobalt industry chain is divided into the upstream mining sector, the midstream refining sector, and the downstream consumption sector.

I. Upstream Supply Market Structure

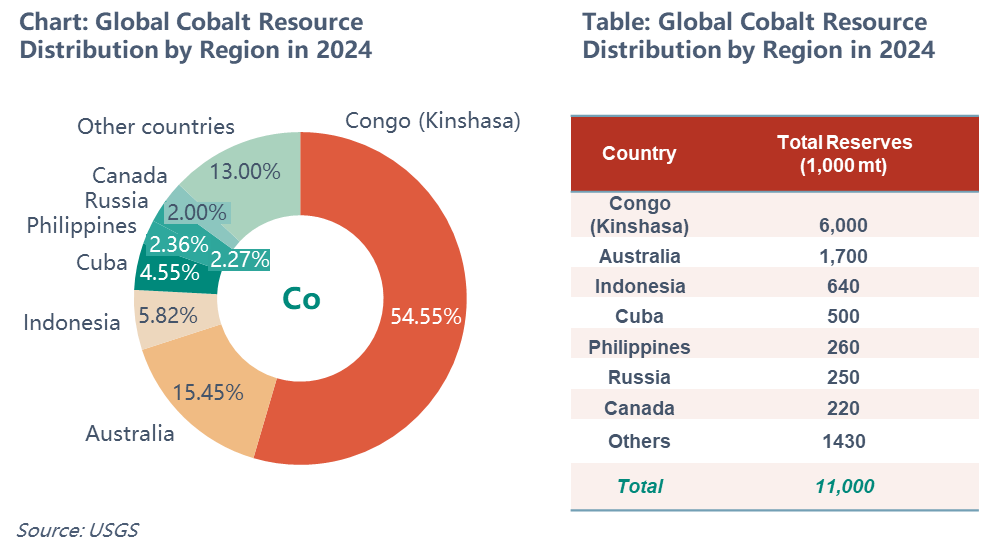

Global cobalt resources are highly concentrated. According to the United States Geological Survey (USGS), the world’s identified cobalt reserves total 11 million tons. The distribution of cobalt resources is extremely uneven, with countries such as the Democratic Republic of Congo (DRC) and Australia being the most resource-rich regions.

China’s cobalt resources mainly come from associated ores, commonly coexisting with copper, nickel, and iron ores. Currently, there are 150 known cobalt mining sites across 24 provinces (autonomous regions) in China. The grade of cobalt ores in China is relatively low, and cobalt is mostly recovered as a by-product. Due to low recovery rates, complex processing, and high production costs, China remains heavily dependent on imports for cobalt resources.

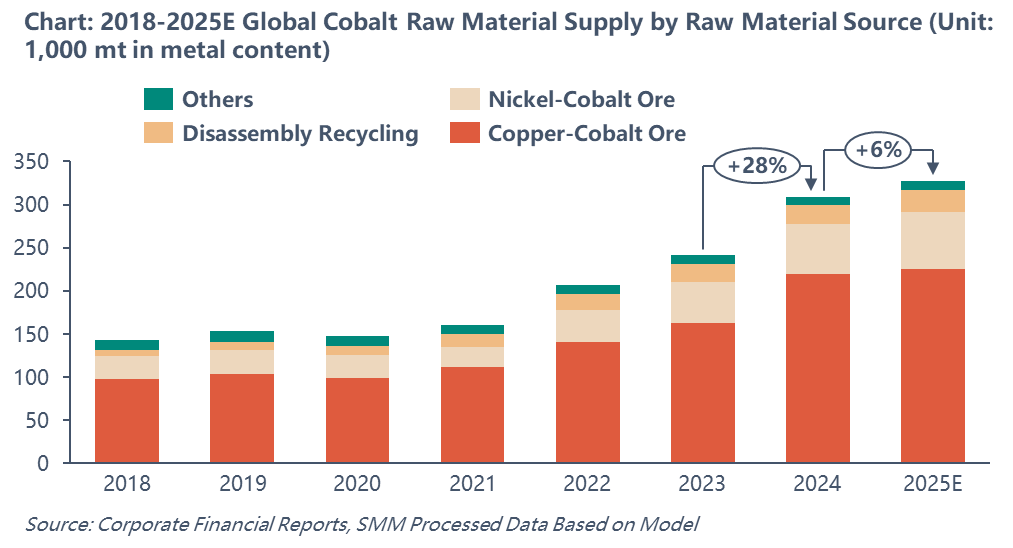

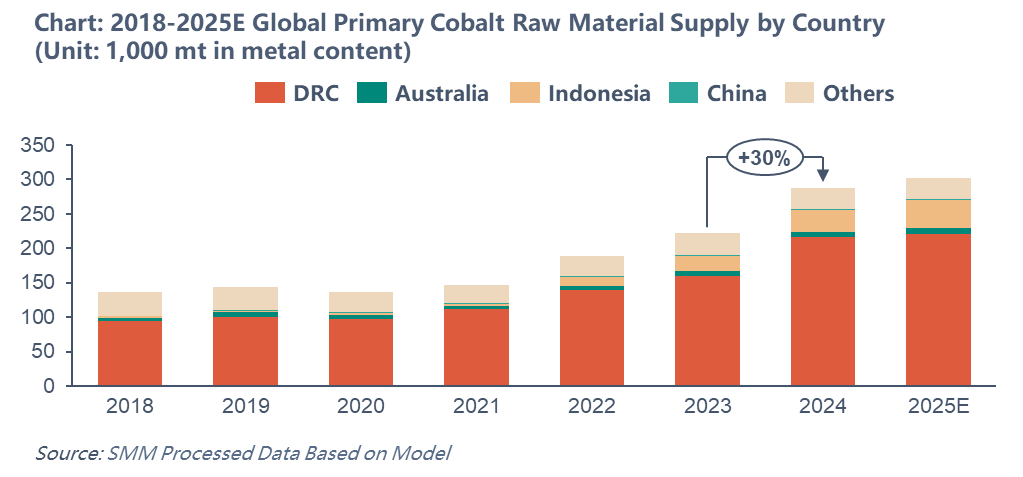

According to SMM’s assessment, in 2024, 71% of the global cobalt raw materials will come from copper–cobalt ores. Currently, cobalt sources are mainly categorized into three types: cobalt ore, recycling, and other channels. As of 2024, 90% of cobalt comes from primary cobalt ores, while recycling and other channels account for 7% and 3%, respectively. Cobalt ores are primarily concentrated in regions such as the Democratic Republic of Congo (DRC), Australia, and Indonesia.

According to SMM’s assessment, in 2024, 71% of the global cobalt raw materials will come from copper–cobalt ores. Currently, cobalt sources are mainly categorized into three types: cobalt ore, recycling, and other channels. As of 2024, 90% of cobalt comes from primary cobalt ores, while recycling and other channels account for 7% and 3%, respectively. Cobalt ores are primarily concentrated in regions such as the Democratic Republic of Congo (DRC), Australia, and Indonesia.

Due to geopolitical issues in the DRC, there are certain restrictions on the export of raw ores. Generally, cobalt intermediate products (i.e., crude cobalt hydroxide with about 30% cobalt content) are shipped to Chinese ports.

Because pyrometallurgical processes cause significant pollution, hydrometallurgical refining is mainly adopted, resulting in more cobalt intermediate products than copper–cobalt alloys. Additionally, recycled raw materials—such as battery scrap and alloy waste—also constitute a part of cobalt raw material supply.

Currently, the leading cobalt mining companies include Luoyang Molybdenum Group Co., Ltd., Swiss-based Glencore, Eurasian Natural Resources Corporation, and China Nonferrous Mining Corporation. The market share of large cobalt mining companies has been steadily increasing. The close competition between Luoyang Molybdenum and Glencore has ended the era when a single mining company could dominate and control cobalt prices.

Currently, the leading cobalt mining companies include Luoyang Molybdenum Group Co., Ltd., Swiss-based Glencore, Eurasian Natural Resources Corporation, and China Nonferrous Mining Corporation. The market share of large cobalt mining companies has been steadily increasing. The close competition between Luoyang Molybdenum and Glencore has ended the era when a single mining company could dominate and control cobalt prices.

II. Overview of Midstream Refining

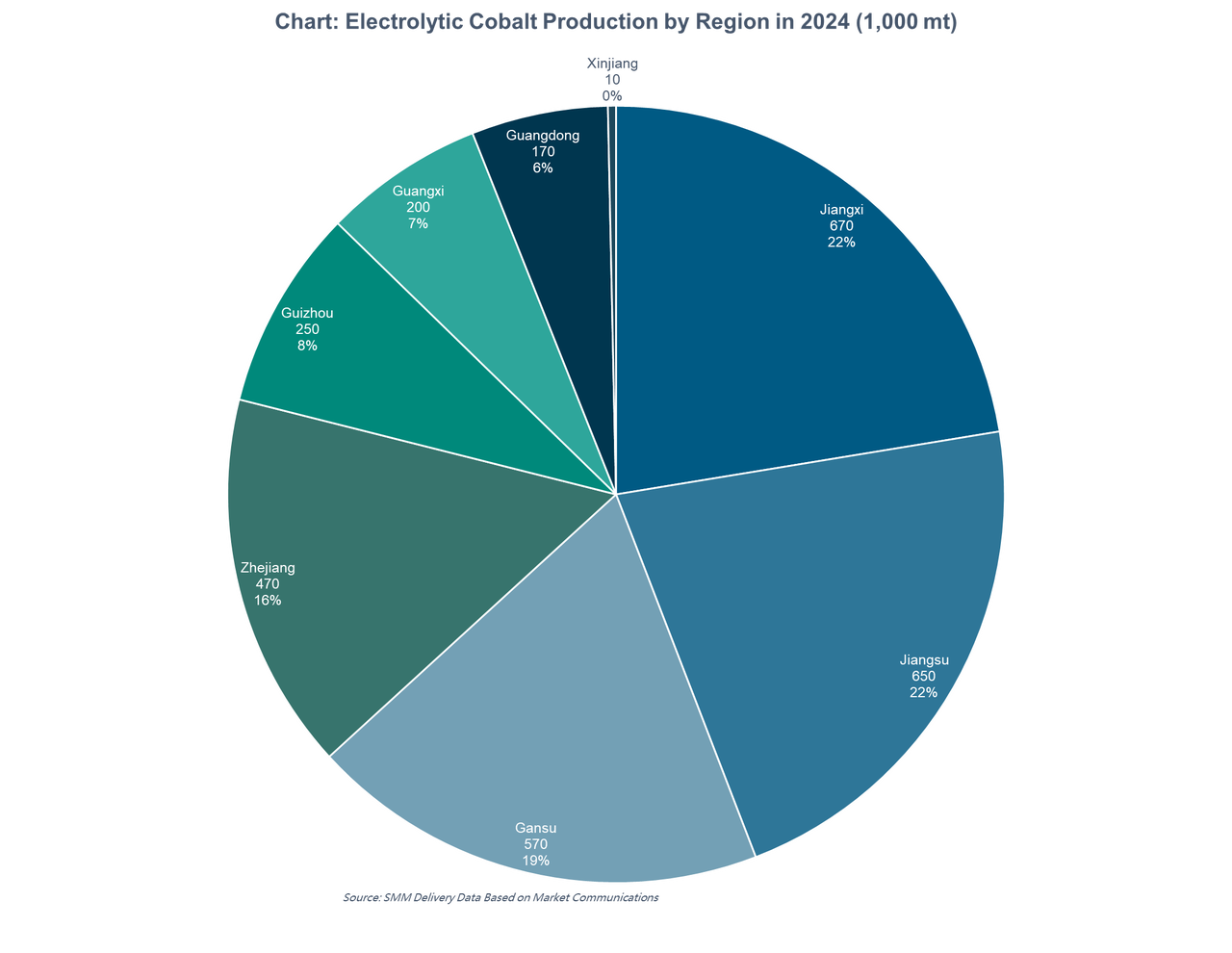

In terms of refined cobalt supply, it is mainly divided into metallic cobalt and cobalt compounds. Metallic cobalt is primarily categorized into cobalt powder and electrolytic cobalt. Cobalt powder is mainly used in cemented carbides (hardmetals), while electrolytic cobalt is mainly used in superalloys, cemented carbides, and magnetic materials. Cobalt compounds mainly include cobalt sulfate and cobalt chloride. Cobalt sulfate is primarily used in ternary precursors, and cobalt chloride is mainly used in cobalt(II,III) oxide (Co₃O₄). Both are important components of lithium-ion battery cathode materials. Additionally, there are other compounds such as cobalt carbonate, cobalt nitrate, cobalt oxalate, and cobalt hydroxide.

Cobalt salts are chemical compounds of cobalt. Common cobalt salt products include cobalt sulfate, cobalt chloride, cobalt nitrate, cobalt acetate, cobalt carbonate, and cobalt oxide. Among them, cobalt sulfate (CoSO₄) is the most widely used cobalt salt, mainly used in the production of ternary precursors for lithium-ion battery cathode materials NCM and NCA, which ultimately serve electric vehicles, electric two-wheelers, and special-purpose vehicles. Cobalt chloride (CoCl₂) is commonly found in consumer applications, including traditional digital consumer electronics such as mobile phones, tablets, and laptops, as well as emerging consumer products like drones, electronic cigarettes, and power tools. Cobalt carbonate (CoCO₃), cobalt nitrate (Co(NO₃)₂), and cobalt oxalate (CoC₂O₄) are mainly used in chemical applications such as catalysts, pigments/decolorants, paint and ink driers, rubber adhesives, and animal feed.

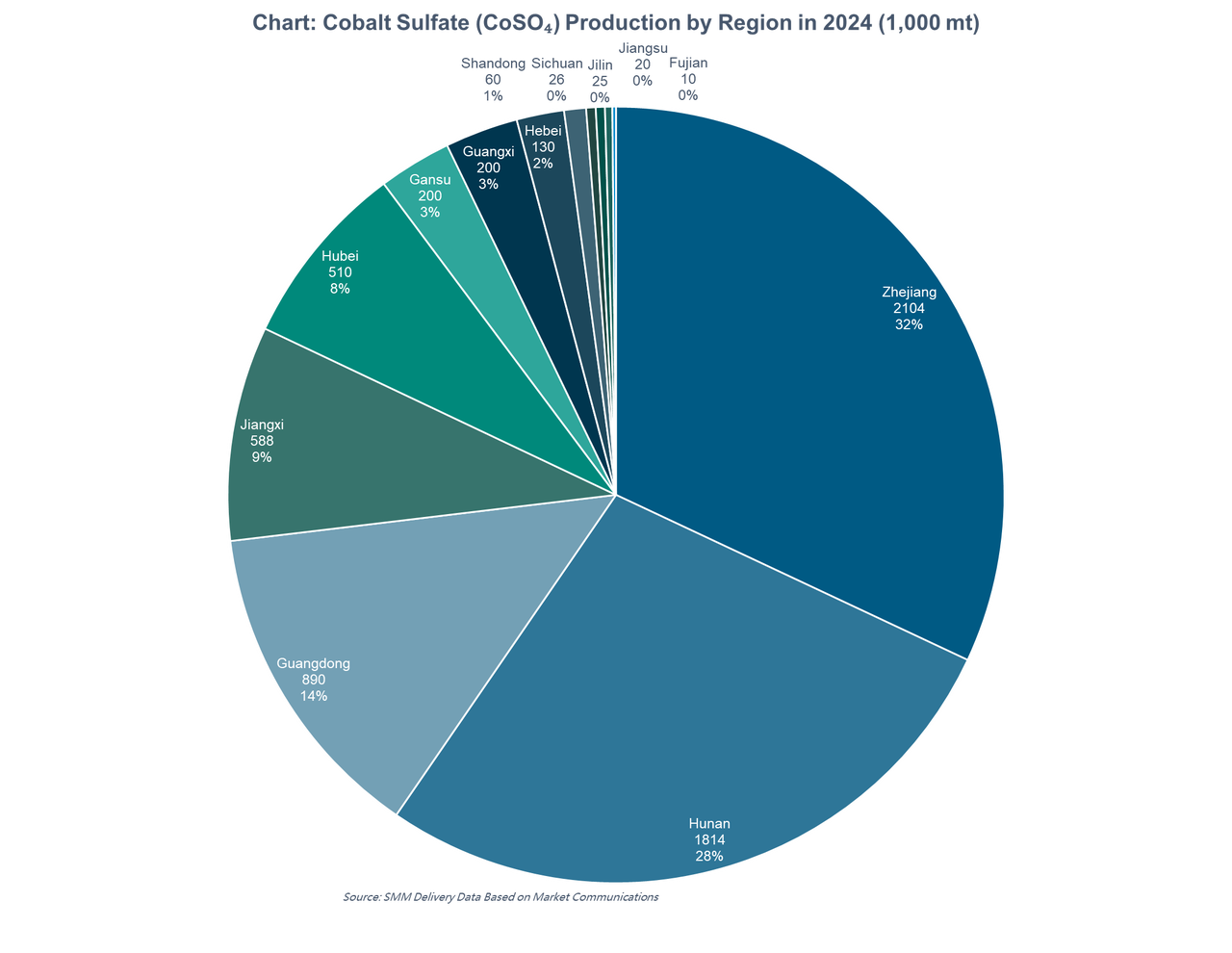

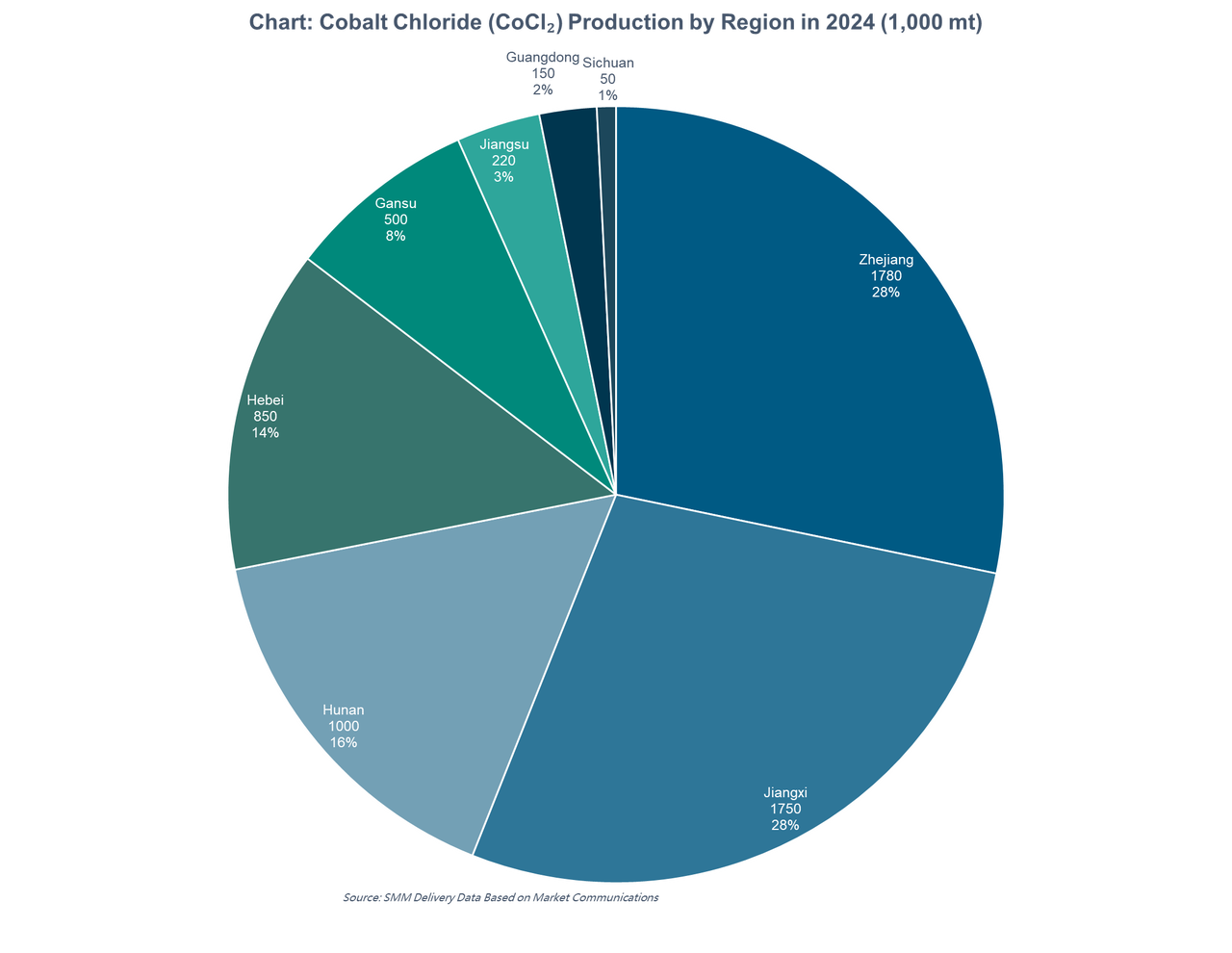

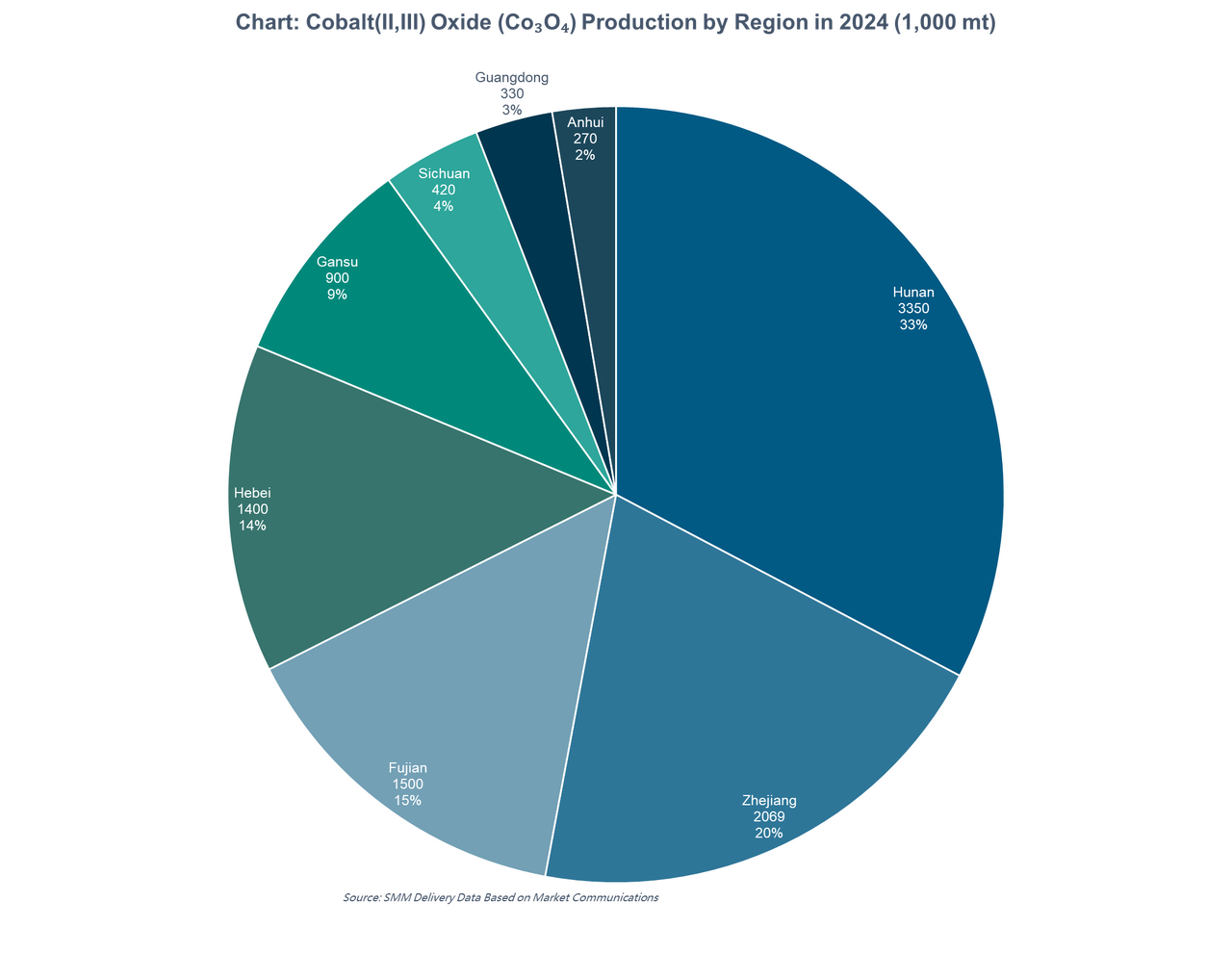

Globally, cobalt salt production is dominated by China, which is currently the world’s largest producer and exporter of cobalt salts. Major production areas in China include Hunan, Jiangxi, Guangxi, Jiangsu, and Zhejiang provinces. Among these, Zhuzhou and Hengyang in Hunan are traditional cobalt salt production bases, home to leading companies such as GEM Co., Ltd. and China Cobalt New Materials; Ganzhou and Yichun in Jiangxi have developed rapidly relying on local resources and the lithium battery industry chain; Jiangsu and Zhejiang mainly host high-end material processing enterprises.

III. Distribution of Downstream Demand Sectors

III. Distribution of Downstream Demand Sectors

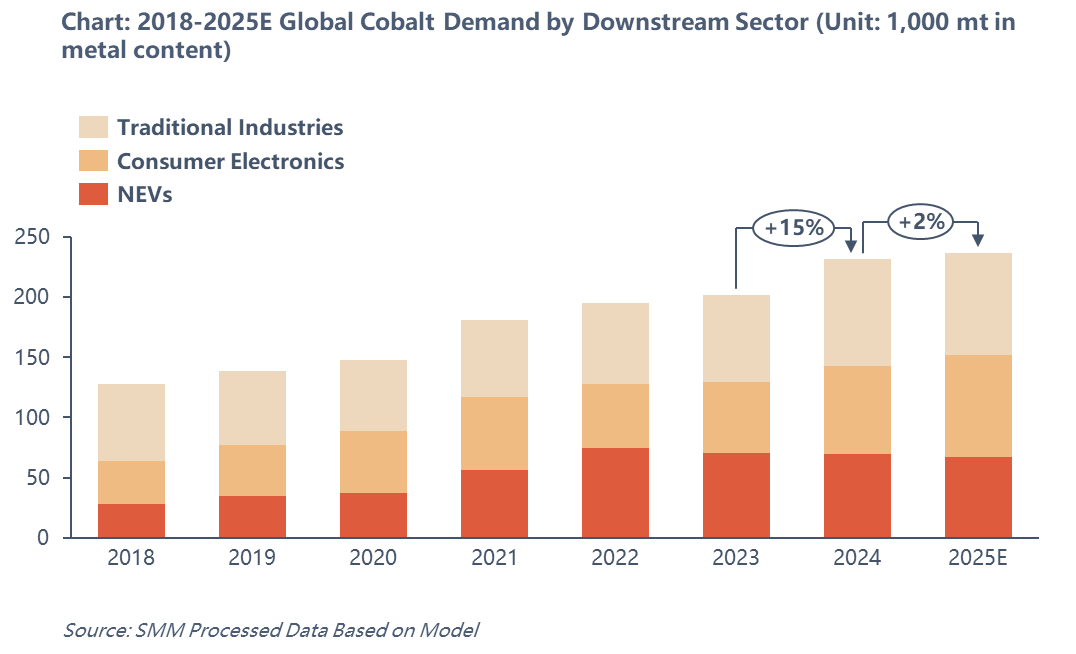

Global cobalt demand mainly comes from the lithium battery sector—including digital devices, new energy vehicles (NEVs), and energy storage applications—as well as traditional industries such as superalloys, cemented carbides, catalysts, ceramic pigments, magnetic materials, and organic materials.

With the widespread adoption of smartphones, cobalt demand in digital batteries and magnetic materials is accelerating, while the demand share in traditional industries remains relatively stable. The explosive growth of the new energy vehicle market once drove up cobalt demand in the electric vehicle sector. However, in recent years, the impact of lithium iron phosphate (LFP) battery systems and the trend toward lower cobalt content in nickel-cobalt-manganese (NCM) battery chemistries have gradually weakened cobalt demand in the electric vehicle sector.

It is forecasted that by 2025, driven by growth in consumer electronics and traditional sectors, global cobalt demand will moderately increase to approximately 236,569 tons. Among this, cobalt demand in the new energy vehicle battery industry is expected to decline to a 28% share. Meanwhile, under the influence of China’s national subsidy policies, the AI boom, and rapid iteration of electronic devices, cobalt demand in the consumer electronics sector is expected to grow, potentially increasing its share to 36%.

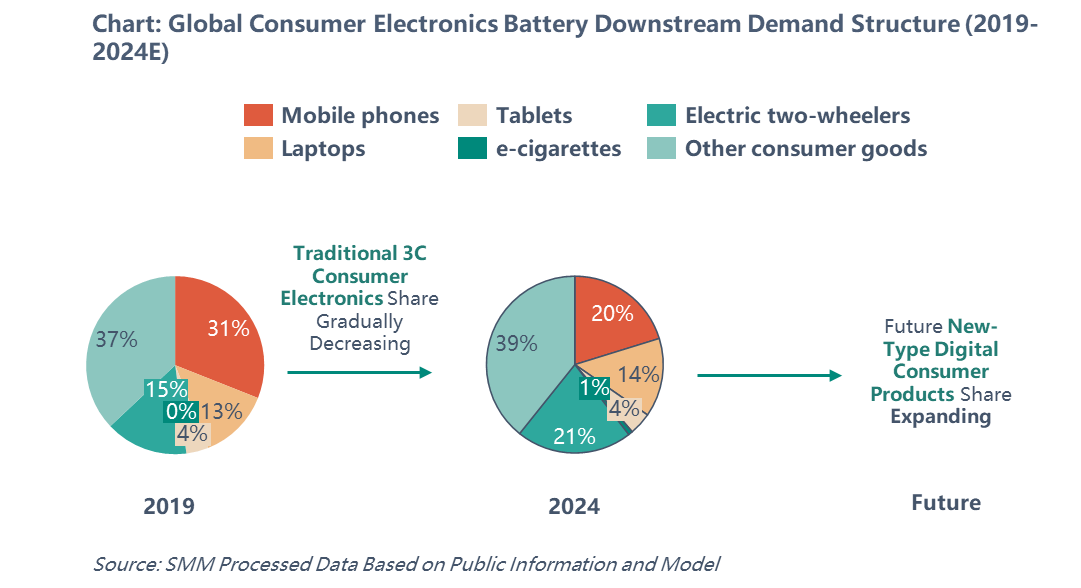

Beyond traditional 3C digital products such as mobile phones, laptops, and tablets, the rapid development of emerging sectors has brought new growth opportunities to the lithium battery market. For example, the rapid expansion of power tools, electric two-wheelers, and drones, along with the continuous emergence of new consumer electronics such as wearable devices, smart speakers, and portable medical devices, has further expanded end-use application scenarios, thereby driving the demand for lithium-ion batteries.

Beyond traditional 3C digital products such as mobile phones, laptops, and tablets, the rapid development of emerging sectors has brought new growth opportunities to the lithium battery market. For example, the rapid expansion of power tools, electric two-wheelers, and drones, along with the continuous emergence of new consumer electronics such as wearable devices, smart speakers, and portable medical devices, has further expanded end-use application scenarios, thereby driving the demand for lithium-ion batteries.

In the future, global demand for consumer lithium batteries will be dominated by new electronic consumer products, while the share of traditional digital consumer electronics will gradually decline. Due to fast technological iteration and broad application scenarios, new electronic products are expected to become the main growth drivers of the consumer lithium battery market.

In 2024, demand from the new digital consumer sector is expected to account for 39% of lithium battery demand, with this proportion continuing to rise. Among these, the drone industry is currently in a rapid development phase and is an important component of the new consumer electronics market. With technological advancements and expanded application scenarios, the drone market is expected to maintain rapid growth.

In recent years, driven by the development of the military and aerospace industries, China’s refined cobalt production capacity has gradually been released. Refined cobalt is primarily used in superalloys. Benefiting from the rapid growth of China’s aviation sector and increased demand from the defense industry, the cobalt-based superalloy market is expected to achieve notable growth, with annual demand projected to rise significantly in 2024.

In recent years, driven by the development of the military and aerospace industries, China’s refined cobalt production capacity has gradually been released. Refined cobalt is primarily used in superalloys. Benefiting from the rapid growth of China’s aviation sector and increased demand from the defense industry, the cobalt-based superalloy market is expected to achieve notable growth, with annual demand projected to rise significantly in 2024.

In addition, refined cobalt is also used in the field of magnetic materials, mainly driven by demand for samarium–cobalt (SmCo) permanent magnets. In 2024, SmCo magnets are expected to be primarily used in communication base stations, high-temperature motors, and other specialized motor applications. The market still holds considerable growth potential.

Looking ahead, as the superalloy and magnetic materials markets continue to expand, cobalt consumption is expected to increase further.