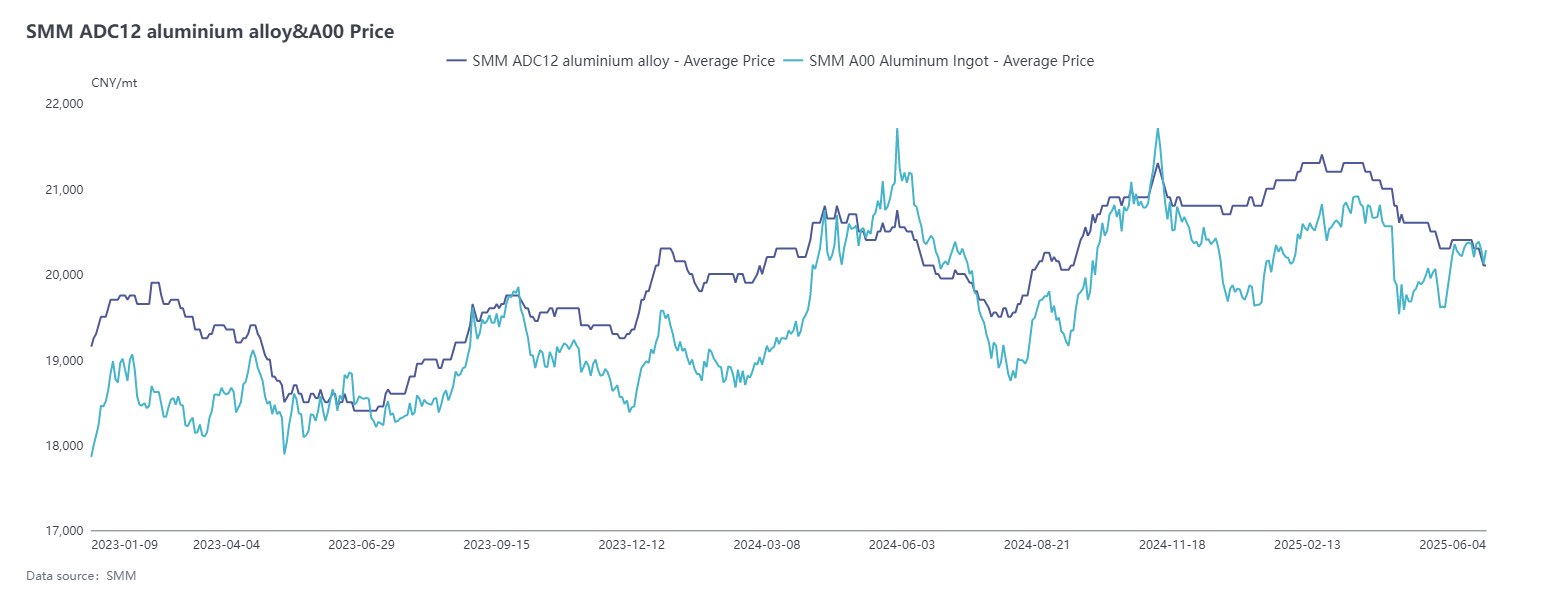

In May, the price center of aluminum prices gradually rebounded above 20,000 yuan/mt. The monthly average spot aluminum price (calendar month) recorded by SMM in May was 20,126 yuan/mt, up 0.9% MoM from the previous month. However, ADC12 prices followed declines but not increases, with the average price in May falling 1.5% MoM against the trend. As of June 4, the SMM ADC12 quote fell 300 yuan/mt MoM to 20,000-20,200 yuan/mt.

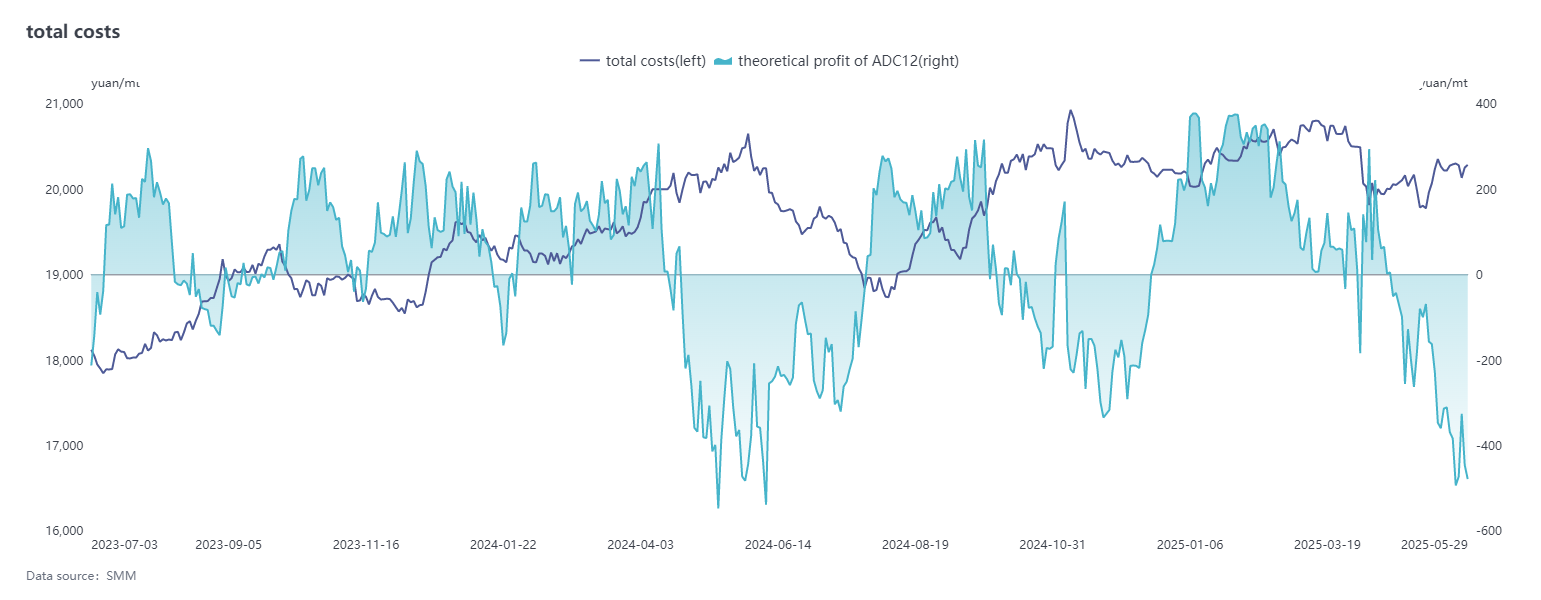

On the cost side, aluminum scrap accounts for nearly 90% of the main cost components of ADC12, and its price trend has a significant impact. Although prices pulled back at the beginning of the month, the contraction in market liquidity triggered traders to refuse to budge on prices and hold back on sales, resulting in strong cost support. The continuous rise in primary aluminum prices in central China during the month further pushed up aluminum scrap prices, increasing the cost transfer pressure on enterprises. On the silicon cost side, the price of oxygen-blown #553 silicon continued to decline, falling by a cumulative 1,100 yuan/mt to 8,300 yuan/mt in May, gradually shrinking its share in the cost structure. Overall, although the prices of some raw materials on the cost side decreased, the overall cost burden remained heavy due to aluminum scrap prices fluctuating at highs. Throughout the month, the industry's theoretical losses on production persisted and widened again at month-end as the price decline of finished alloy ingots outpaced the cost decline.

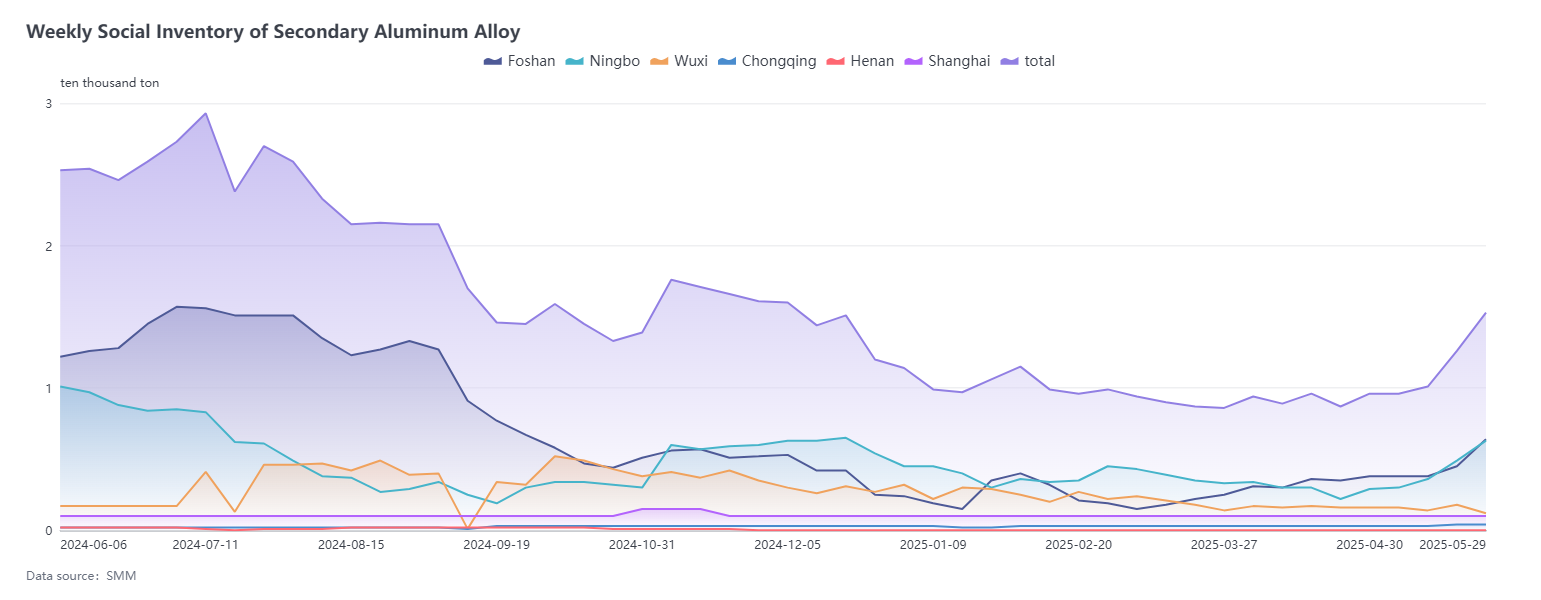

Demand side, demand continued to face pressure in May, becoming the primary factor constraining prices. The characteristics of the traditional off-season gradually emerged and intensified, with a decrease in both domestic and overseas orders, leading to sluggish overall market trading. Additionally, aluminum prices fluctuated significantly in May, exacerbating downstream buyers' wait-and-see sentiment. This increased sales pressure on secondary aluminum enterprises, resulting in a continuous buildup of finished product inventories. Consequently, secondary aluminum alloy prices were trapped in a dilemma of being "more likely to fall than rise." Although a joint statement was released during the Sino-US Geneva economic and trade talks in mid-May, announcing mutual tariff reductions and establishing an observation period, which sent positive signals, there was no significant boost in secondary aluminum consumption. Furthermore, constrained by the off-season, the social inventory of aluminum alloy at month-end increased significantly by 5,740 mt from the beginning of the month to 15,339 mt, accelerating the pace of inventory buildup.

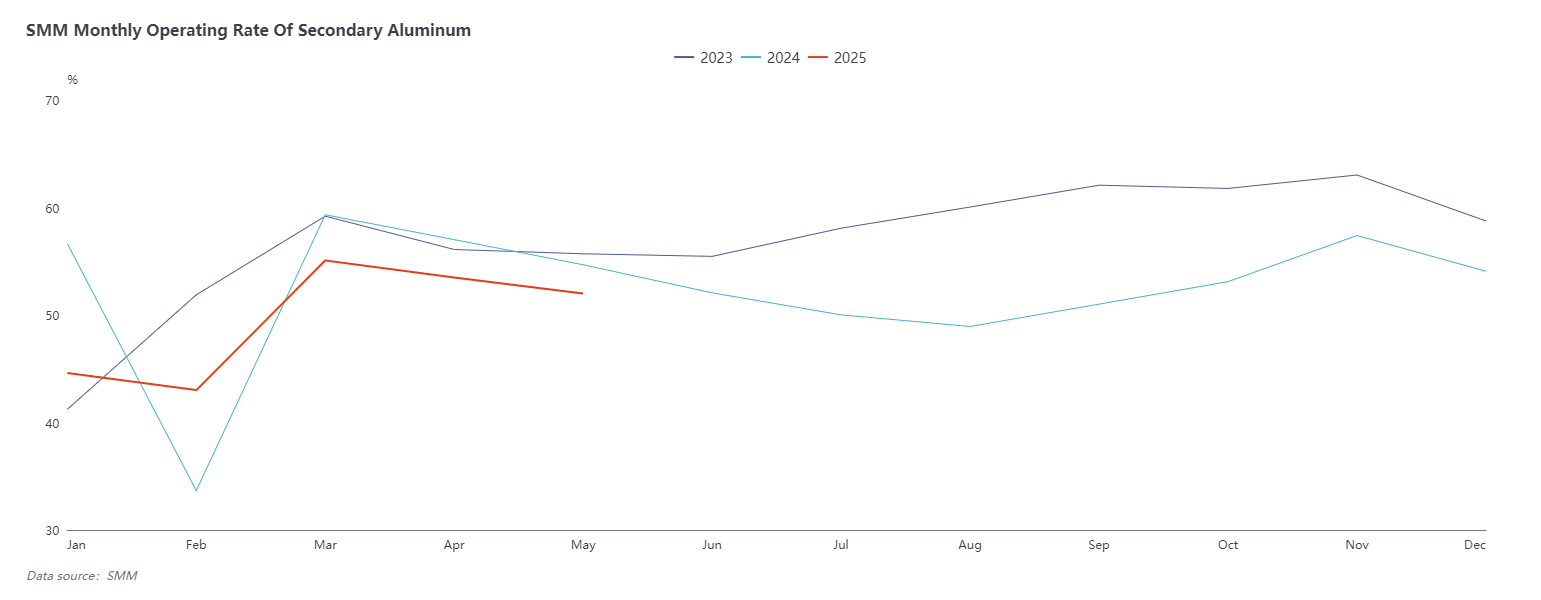

In terms of supply, the operating rate of the secondary aluminum alloy industry in May dropped back slightly by 1.49 percentage points MoM from April to 52.01%, and declined by 2.67% YoY. Although the operating rate recovered slightly in the early days after the Labour Day holiday, under the triple pressure of high costs, insufficient orders, and continuous losses on production, the overall operating rate of the industry showed a downward trend, with frequent production cuts and suspensions. In particular, small and medium-sized enterprises were severely affected, with a significant decline in operating rates, and some enterprises were basically in a state of suspension. In contrast, large enterprises maintained relatively stable production due to their own advantages. Entering June, the traditional off-season continued. Given that the operating rate of enterprises had already declined significantly in April and May, the decline in June was expected to be limited. On June 10, cast aluminum alloy futures will be officially listed on the SHFE, with the first listed contract being AD2511. As the delivery period is still far away, secondary aluminum enterprises, which are delivery brands, will not expand their production scale for the time being, and the supply landscape will not change significantly in the short term due to the listing of futures.

Overall, the secondary aluminum market in May remained in a phase of struggle between intensifying weak demand and strengthening cost support. Among these factors, weak demand was the main driver pulling prices down. Despite the cost side providing some support to prices, under the influence of sluggish end-use consumption and insufficient purchase willingness, SMM ADC12 prices ultimately fluctuated within a narrow range of 20,100-20,400 yuan/mt, in the doldrums. Looking ahead to June, demand is expected to remain weak, particularly as the traditional off-season deepens and end-user orders decrease, which will continue to constrain the upside room for prices. However, cost support, formed under the tight supply of aluminum scrap raw materials, is expected to persist. Going forward, it is crucial to focus on the raw material supply situation and changes in order volumes. Meanwhile, after the listing of cast aluminum alloy futures on June 10, it may lead to increased short-term price volatility in the market. Attention should be paid to the impact of the listing on domestic spot prices and market trading patterns.