SHANGHAI, May 5 (SMM) - This is a roundup of China's metals weekly inventory as of May 5.

SMM Weekly Updates on China Aluminium Ingot and Billet Social Inventories as of May 4

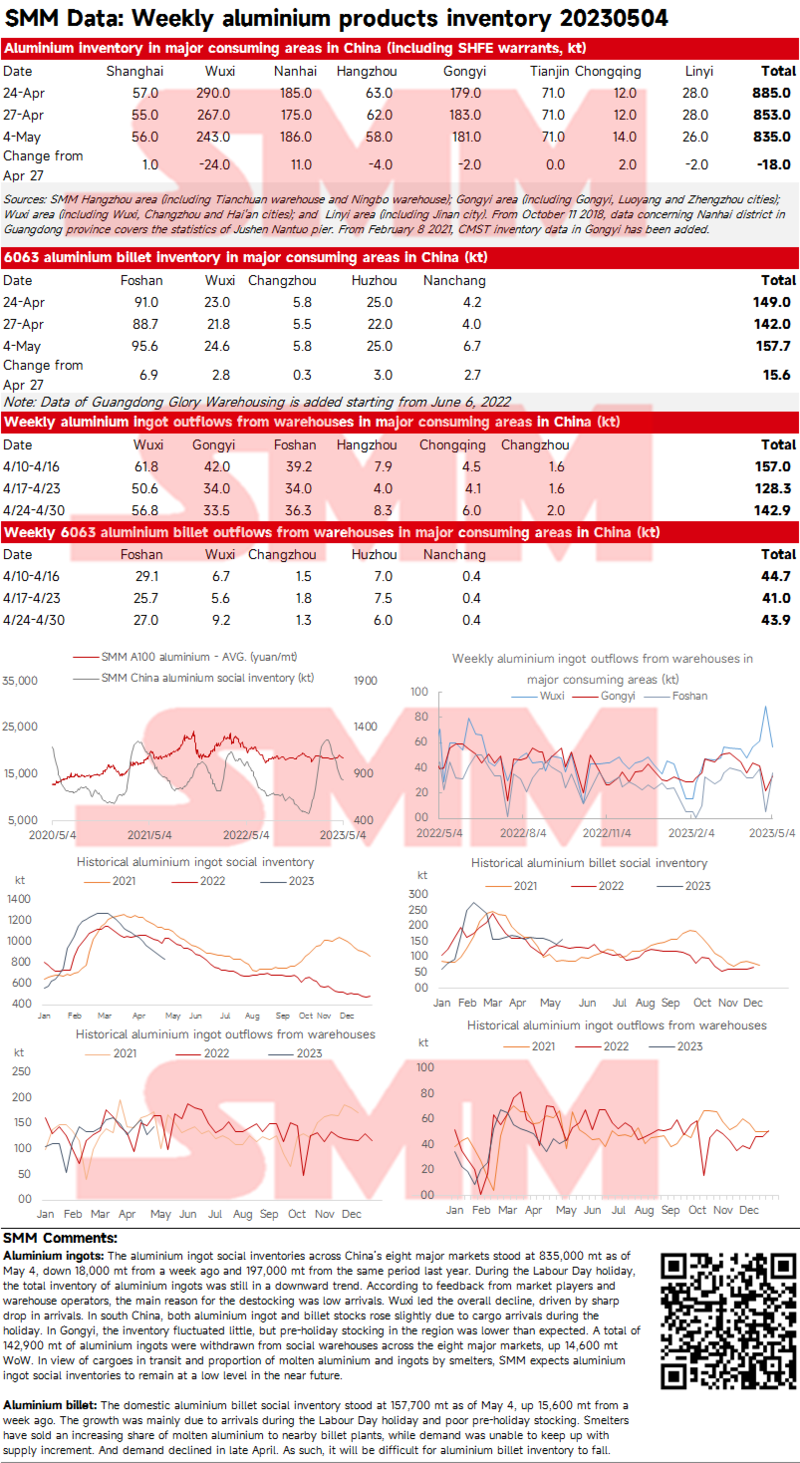

Aluminium ingots: The aluminium ingot social inventories across China’s eight major markets stood at 835,000 mt as of May 4, down 18,000 mt from a week ago and 197,000 mt from the same period last year. During the Labour Day holiday, the total inventory of aluminium ingots was still in a downward trend. According to feedback from market players and warehouse operators, the main reason for the destocking was low arrivals. Wuxi led the overall decline, driven by sharp drop in arrivals. In south China, both aluminium ingot and billet stocks rose slightly due to cargo arrivals during the holiday. In Gongyi, the inventory fluctuated little, but pre-holiday stocking in the region was lower than expected. A total of 142,900 mt of aluminium ingots were withdrawn from social warehouses across the eight major markets, up 14,600 mt WoW. In view of cargoes in transit and proportion of molten aluminium and ingots by smelters, SMM expects aluminium ingot social inventories to remain at a low level in the near future.

Aluminium billet: The domestic aluminium billet social inventory stood at 157,700 mt as of May 4, up 15,600 mt from a week ago. The growth was mainly due to arrivals during the Labour Day holiday and poor pre-holiday stocking. Smelters have sold an increasing share of molten aluminium to nearby billet plants, while demand was unable to keep up with supply increment. And demand declined in late April. As such, it will be difficult for aluminium billet inventory to fall.

Copper Inventories in China Bonded Zone Increased

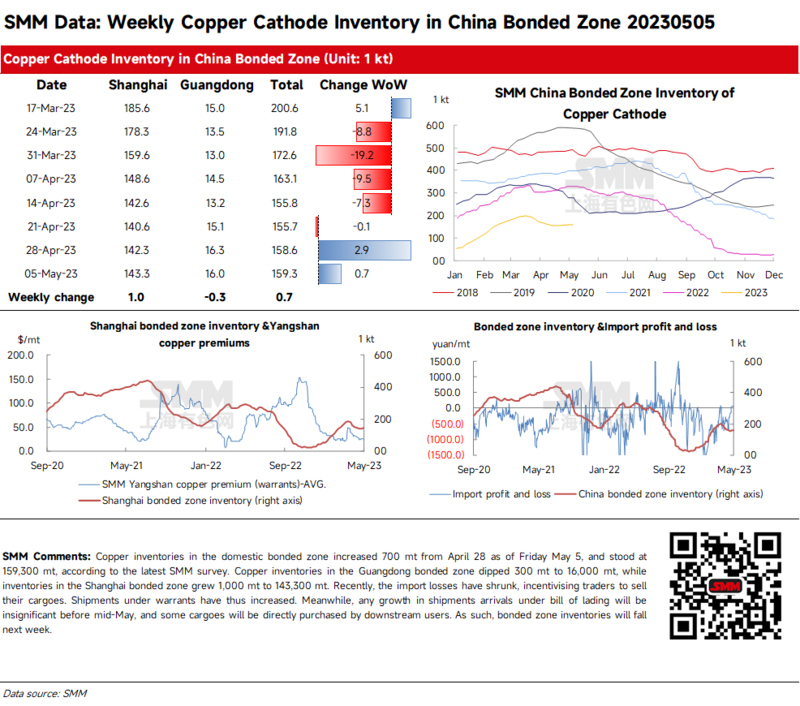

Copper inventories in the domestic bonded zone increased 700 mt from April 28 as of Friday May 5, and stood at 159,300 mt, according to the latest SMM survey. Inventory in the Guangdong bonded zone dipped 300 mt to 16,000 mt, and inventory in the Shanghai bonded zone grew 1,000 mt to 143,300 mt.

Recently, the import losses have shrunk, incentivising traders to sell their cargoes. Shipments under warrants thus increased. Meanwhile, any growth in shipments arrivals under bill of lading will be insignificant before mid-May, and some cargoes will be directly purchased by downstream users. As such, bonded zone inventories will fall next week.

Social Inventory of Lead Ingot Increase amid Supply Recovery and Weak Demand

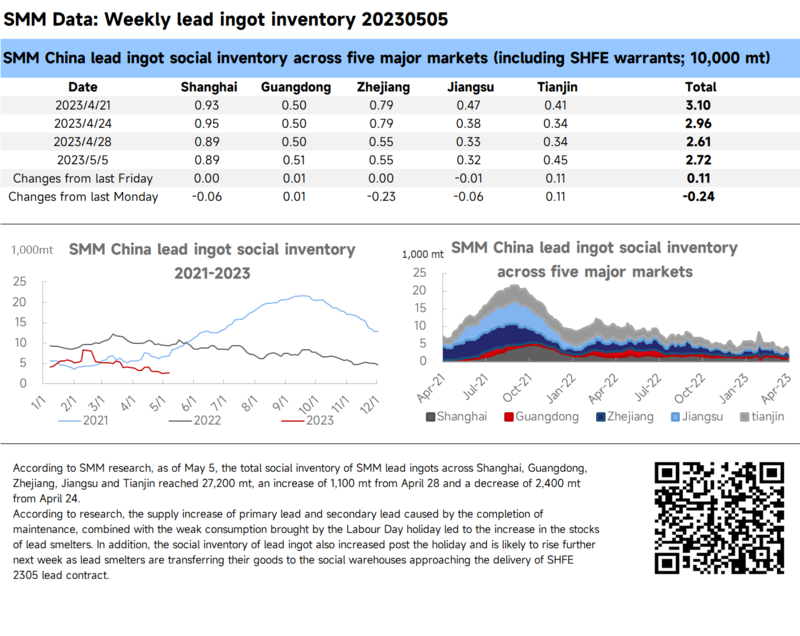

According to SMM research, as of May 5, the total social inventory of SMM lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin reached 27,200 mt, an increase of 1,100 mt from April 28 and a decrease of 2,400 mt from April 24.

According to research, the supply increase of primary lead and secondary lead caused by the completion of maintenance, combined with the weak consumption brought by the Labour Day holiday led to the increase in the stocks of lead smelters. In addition, the social inventory of lead ingot also increased post the holiday and is likely to rise further next week as lead smelters are transferring their goods to the social warehouses approaching the delivery of SHFE 2305 lead contract.

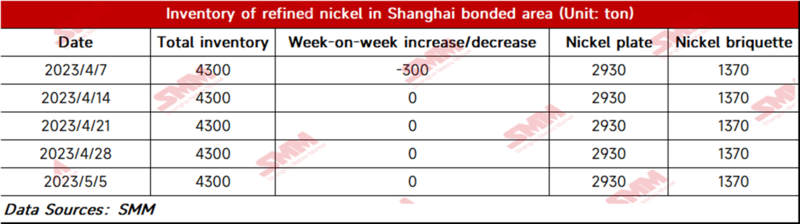

Pure Nickel Bonded Zone Inventory Stood Flat from Apr 28

As of May 5, bonded zone inventory of nickel stood flat WoW at 4,300 mt. The inventory of nickel briquettes was 1,370 mt, and that of nickel plates was 2,930 mt. The import window remained closed amid the decline in the SHFE/LME nickel price ratio, but some spots were still shipped to the domestic market as some traders locked in the price ratio earlier, greatly easing the supply tightness of imported pure nickel in China.

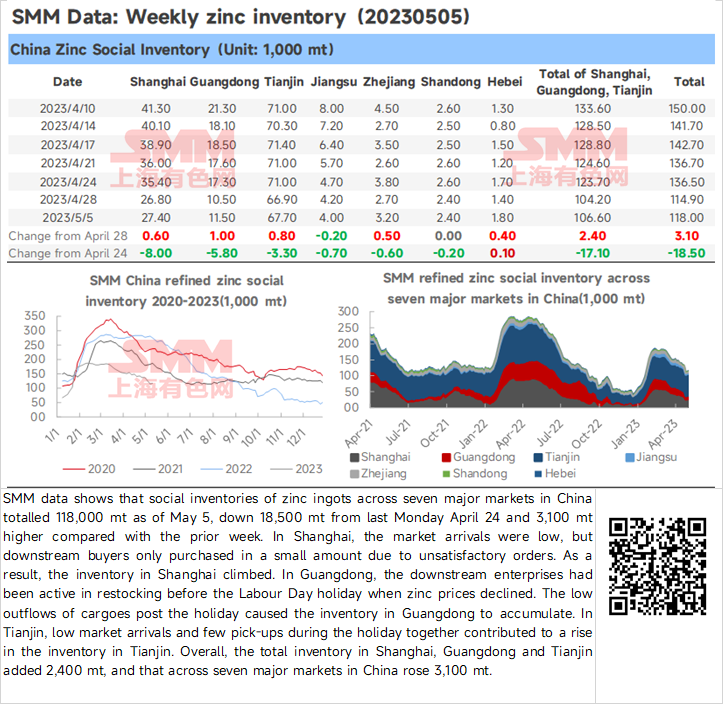

Zinc Ingot Social Inventory Up 3,100 mt on the Week

SMM data shows that social inventories of zinc ingots across seven major markets in China totalled 118,000 mt as of May 5, down 18,500 mt from last Monday April 24 and 3,100 mt higher compared with the prior week. In Shanghai, the market arrivals were low, but downstream buyers only purchased in a small amount due to unsatisfactory orders. As a result, the inventory in Shanghai climbed. In Guangdong, the downstream enterprises had been active in restocking before the Labour Day holiday when zinc prices declined. The low outflows of cargoes post the holiday caused the inventory in Guangdong to accumulate. In Tianjin, low market arrivals and few pick-ups during the holiday together contributed to a rise in the inventory in Tianjin. Overall, the total inventory in Shanghai, Guangdong and Tianjin added 2,400 mt, and that across seven major markets in China rose 3,100 mt.

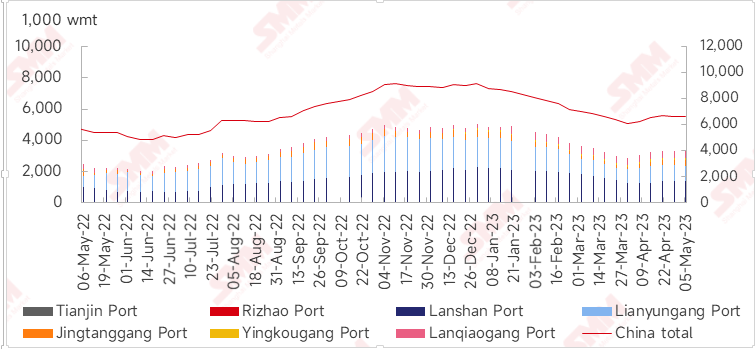

Nickel Ore Inventories at Chinese Ports down 40,000 wmt WoW

As of May 5, the nickel ore inventories at Chinese ports dropped 40,000 wmt from a week earlier to 6.6 million wmt. The total Ni content stood at 52,000 mt. The port inventory of nickel ore across seven major Chinese ports stood at 3.31 million wmt, down 10,000 wmt WoW. The prices of nickel ore rose slightly this week driven by the buyers' rigid demand, and the mines also held their prices firm. Mines in the Philippines will ship spot ore gradually in May. Therefore, the port inventory may maintain an upward track in the near future.