SHANGHAI, Feb 18 (SMM) - This is a roundup of China's metals weekly inventory as of February 18.

Copper Inventory in Major Chinese markets Added 13,600 mt from Monday

As of Friday February 18, the copper inventories in major domestic markets stood at 211,800 mt, up 13,600 mt from Monday February 14, and up 113,100 mt from pre-CNY holiday level of 98,700 mt.

From the date of Chinse New Year (CNY) until the 12th calendar day post the CNY holiday, the increment of inventory was 14,200 mt more than the same period in 2021, when the inventory recorded an increase of 98,900 mt. Apart from the slow resumption of production after the holiday, the resurging pandemic in east China was also among the major causes.

Most markets in China saw rising inventory compared with Monday, which was even greater in some places with the delivery from smelters for SHFE 2202. In details, the inventory rose 10,400 mt to 126,100 mt in Shanghai, added 1,000 mt to 20,200 mt in Jiangsu, climbed 1,600 mt to 2,200 mt in Zhejiang, jumped 3,000 mt to 3,000 mt in Jiangxi, and advanced 800 mt to 3,800 mt in Chongqing. The inventory dropped 1,900 mt to 53,600 mt in Guangdong, fell 300 mt to 900 mt in Chengdu, and decreased 1,000 mt to 2,000 mt in Tianjin.

Looking forward, the inventory is likely to increase more slowly in the third week post the CNY holiday.

Copper Inventory in Domestic Bonded Zone Up 20,850 mt on Week

The copper inventories in domestic bonded zones rose 20,850 mt from last Friday to 286,100 mt as of February 18, according to SMM survey.

The inventory in the Shanghai bonded zone rose 19,200 mt to 250,200 mt, while that in Guangdong added 1,650 mt to 35,900 mt on the week.

The foreign trade market was quiet recently, and the import losses were around 800 yuan/mt, hence the customs clearance demand was rare. The arrivals ports had to be stored in the bonded zone. Meanwhile, domestic smelters kept exporting copper cathode to the bonded zone as well. The bonded zone inventory rose.

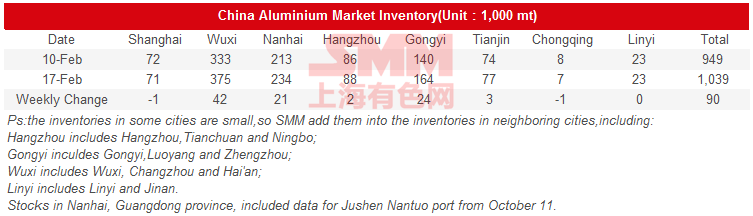

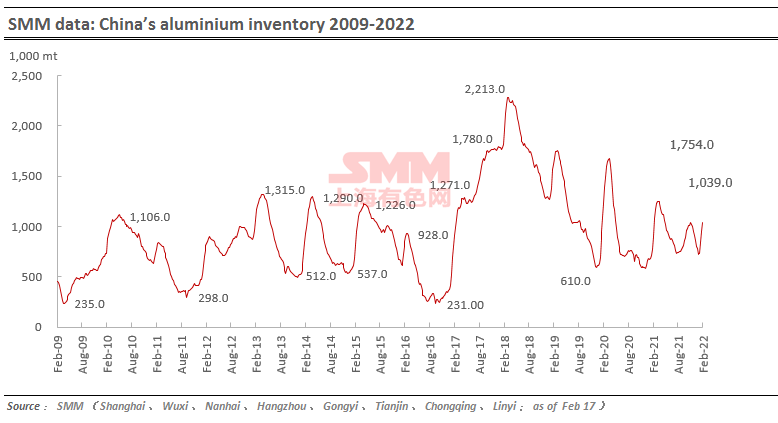

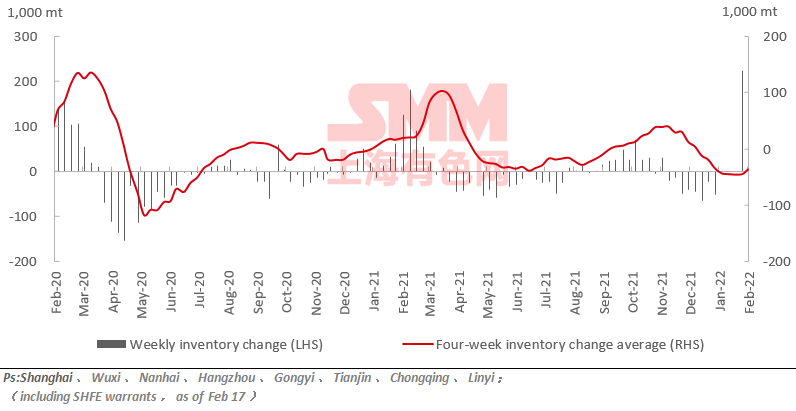

Aluminium Ingot Social Inventory Up 90,000 mt on Week

SMM data showed that the aluminium ingot social inventory in China totalled 1.04 million mt as of February 17, 2022, up 90,000 mt from last Thursday February 10, with Wuxi (+42,000 mt), Gongyi (+24,000 mt), Nanhai (+21,000 mt) being the major contributors to the overall increase.

Aluminium Billet Inventories in China Dropped 2,900 mt on Week

The domestic aluminium billet inventory stood at 264,600 mt on February 17, a decrease of 2,900 mt or 1.08% week-on-week, falling for the first time post CNY.

Among them, the inventory in Foshan dropped the most by 8,700 mt or 6.45%, followed by Nanchang where the local inventory fell 6,300 mt or 25.71%. The inventory in Foshan dropped as the arrivals in south China were low amid disputed logistics owing to the COVID pandemic in Guangxi. Meanwhile, the conversion margins rallied, resulting in more purchases amid worries over possible tight supplies in the near future. The warehouses in Nanchang also indicated less arrivals, and the shipments leaving the warehouses were also sluggish. The shipments in other markets were also less satisfactory as the downstream has not fully resumed the production.

Zinc Ingot Social Inventory in Seven Major Regions Rose 20,400 mt

As of February 18, the zinc ingot inventory across the seven major regions in China totalled 263,100 mt, up 8,800 mt from Monday February 14 and up 20,400 mt from last Friday February 11, according to SMM data. The domestic inventories continued to accumulate this week. In Shanghai, downstream producers restocked after they resumed production, but the inventory rose significantly as many cargoes arrived. In Guangdong, downstream demand improved, allowing the inventory growth to slow down. In Tianjin, the inventory continued to increase amid large arrivals and modest downstream restocking. The total inventories across Shanghai, Guangdong, and Tianjin rose by 19,600 mt from February 11.

Lead Ingot Social Inventory Rose by 3,100 mt on Week

The social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin increased 3,100 mt from last Friday February 11 and up 100 mt from Monday February 14, and stood at 96,200 mt as of February 18.

According to SMM survey, most enterprises from the lead industry chain basically completed the resumption of work last week. However, the resumption of lead-acid battery enterprises was more slowly, and the lead prices kept rising last week, causing the downstream users to stay wait-and-see or purchase secondary lead for the higher cost effectiveness. Therefore, the lead ingot social inventory continued to increase.

The production will continue to recover across the lead industry, but the enterprises may not expand the production significantly considering the modest consumption in the lead-acid battery market. The consumption of lead ingots is expected to be relatively low. SMM will monitor the SHFE/LME lead price ratio as well as the export chances.

Silicon Metal Social Inventory Decreased 3,000 mt on Week

The social inventory of silicon metal across Huangpu port, Kunming city and Tianjin port decreased 3,000 mt from the previous week to 80,000 mt as of Friday 18.

The transactions were active in the market, and the silicon metal stocks were transferred from silicon plants to ports or other regions. The inventory in Yunnan dropped more significantly due to the low local operating rates. The total social inventory is expected to drop further this week.

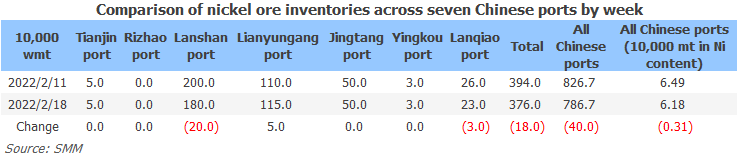

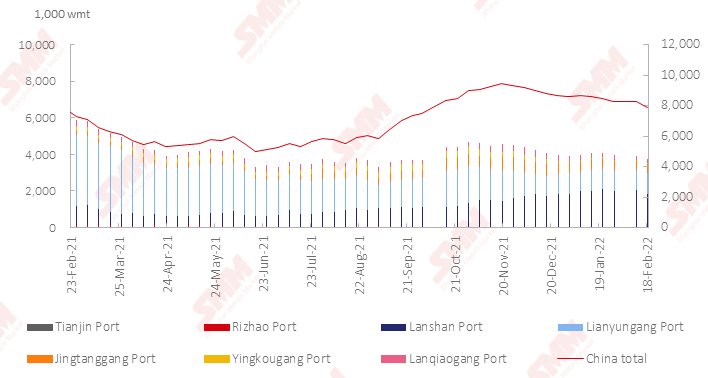

Nickel Ore Inventories at Chinese Ports Fell 400,000 wmt on Week

The nickel ore inventory at Chinese ports dipped 400,000 wmt on week to 7.88 million wmt as of February 18. Total Ni content stood at 61,800 mt. The total inventory at seven major ports stood at around 3.76 million mt in Ni content, 400,000 mt in Ni contentlower than Friday February 11.

The port inventory of laterite nickel kept falling. The shipments leaving the Philippines were low in January and February at a level of less than 50 ships in each month. Downstream demand, on the other hand, picked up recently with the lift of environmental protection-related restrictions, hence the inventory is likely to drop more quickly.

![Inventory Hit a New Low for the Year with Premiums Staying High, but Beware of Weakening Consumption Dragging Down Premiums [SMM South China Copper Cathode Spot Weekly Review]](https://imgqn.smm.cn/usercenter/LbxVx20251217171714.jpeg)

![Inventory and Copper Prices Both Declined, Spot Trades Better Than Yesterday [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/Bwtty20251217171714.jpeg)