Post-CNY Copper Cathode Market Supply-Demand Pattern and Price Forecast

SMM has done a thorough research regarding post-CNY (Chinese New Year) copper cathode supply and demand pattern as well as the potential changes of inventory, which, we assume, must be the key concern of the market participants. The result of the research comes as follows:

Supply:

Maintenance will not be the key word in February and March. There are four smelters planning to carry output maintenance in late March, which will reduce the output by around 8,000 mt, according to SMM research. In other words, it will have insignificant impact on post-holiday inventory accumulation, and serves as a bullish factor for the whole inventory to drop smoothly. SMM believes that the output in February and March will stand at 850,000 mt and 860,000 mt respectively, up 28,200 mt and down 5,000 mt year-on-year respectively, or a combined increase of 25,200 mt.

As of copper cathode imports, the import volume is expected to fall 20,000-30,000 mt in February and March 2022 year-on-year as the baseline in 2021 was high and the recent SHFE/LME price ratio has not been favourable.

Demand:

The spread between copper cathode and copper scrap is likely to expand post the CNY holiday amid rapidly rising copper prices. Hence the downstream demand for copper cathode will be suppressed, and the relative purchases will drop drastically as well. It can be told from the constantly low post-holiday demand in Guangdong in 2021 compared with the previous years.

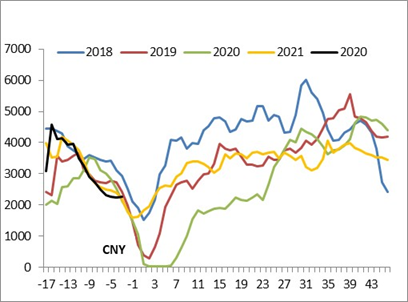

Five-day Average Shipments in Guangdong around the CNY Holiday

Looking into 2022, copper prices are more likely to fall instead of rising ahead of the expected interest rate hike of the US Federal Reserve in March. As such, copper scrap will be less favoured by the market as a substitute for copper cathode. Besides, the central government has increased the liquidity at the beginning of 2022 in order to stabilise the economy, and a series of infrastructure construction projects have been initiated for the same purpose. Meanwhile, the short-term export market is expected to maintain the prosperity, and will not see palpable bearish development in the near future. To sum up, SMM believes that the post-holiday demand in China will rally steadily, and the consumption of copper cathode will also outperform the previous year.

Inventory

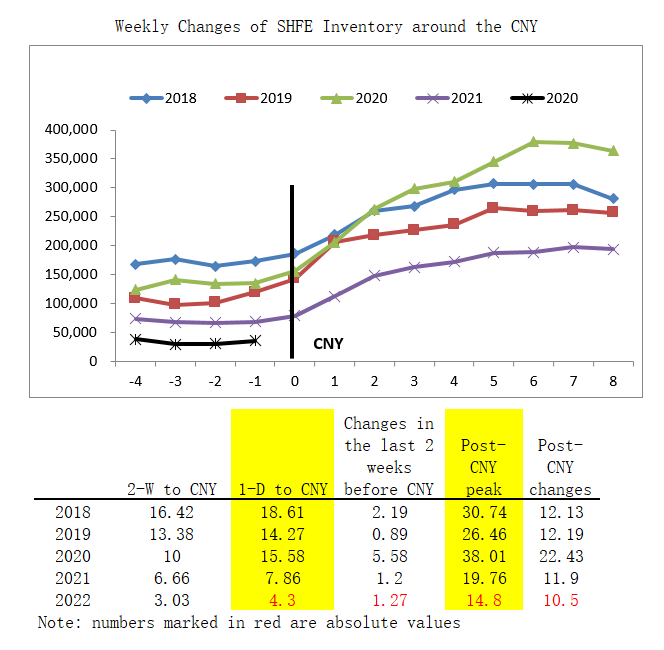

The copper inventory rose ahead of the CNY holiday in 2022, which is in line with market estimate. The increase in total inventories recorded 12,700 mt, flat from 2021. Nonetheless, though the post-holiday inventory is still likely to rise, the actual increase is estimated to be less than in the same period in 2021 (the high in total inventories usually comes in the 6th week post the CNY), the causes, as is mentioned above, lie in the forecast that the demand will grow more quickly than the supply. As such, the post-holiday inventory is likely to rise by around 10,500 mt, below the level of 11,900 mt seen in 2021, which is also the lowest in the past few years. The inventory changes are as follows:

Price forecast:

The copper prices are more likely to drop after the CNY holiday as the market broadly believes that the US Fed will hike the interest rate in mid-March, according to SMM forecast. However, there is also lower possibility that copper prices will experience drastic falls on the ground of better-than-last-year post-holiday demand as well as the low inventories. The market, though, shall keep an eye on the unexpected liquidity tightening of the Fed. From a technical point of view, the current copper prices are about to walk out the triangle consolidation range. It is expected that there will be a breakthrough in 1 or 2 weeks after the holiday, and the focus is on whether the prices will move upwards or downwards.

If the prices move upwards and break through the resistance, the copper prices are expected to hit a high of 75,400 yuan/mt, or meet support at 66,600 yuan/mt first and then 64,000 yuan/mt the other way round.

Post-holiday Aluminium Prices Will Maintain Upside Momentum

As of the second to the last week ahead of the Chinese New Year (CNY), the domestic aluminium inventory stood at 72,500 mt, marking a combined fall of around 300,000 mt in seven consecutive weeks. The continuous fall in inventory was partly caused by the slow resumption of the curbed capacities in 2021. On the other hand, the aluminium ingot imports were drastically reduced after the import window closed. The resilient consumption after the New Year’s Day also contributed to the decrease in total inventories. The inventory increase is likely to be less than 450,000 mt during the CNY holiday, a low in the past five years. Hence, aluminium prices will still carry support post the holiday. In the mid-term, the overseas production restrictions will keep supporting LME aluminium prices, while domestic aluminium supplies will fall by more than 100,000 mt on a monthly basis after the import window closes. In other words, the short-term inventory accumulation will soon turn to post-holiday reduction. The spot premiums over SHFE aluminium contract will stay firm, evidencing the comparatively tight supply of aluminium ingot post the CNY holiday. The high end of aluminium prices are likely to rise above 220,000 yuan/mt after the CNY holiday.

Lead Prices Are Likely to Pull Back from Highs after the CNY Holiday

The base metals prices are unlikely to sustain their upside momentum amid strong expectation of interest rate hike by the Federal Reserve in March as well as the geopolitical threatens. On the other hand, lead ingot inventories are expected to rise post the CNY holiday. On the whole, the lead smelter will take shorter holidays than the downstream participants during the CNY. The large-sized primary lead smelters, mostly located in Henan, will take shifts to produce during the holiday, while other smelters will take the time to conduct maintenance. The total output during the CNY holiday is likely to drop by around 30-40%. For secondary lead, the mid and small-sized smelters will almost all be closed for the holiday during the period from January 25 to February 15. Meanwhile, the large-sized smelters, mostly in Anhui, will take shifts to produce. Hence around 50-60% of the output will be affected by the holiday factor. The downstream participants will also take the CNY holiday during the period from January 22 to February 15, and will be closed for 5 days the shortest. Around 90% of the downstream output will be affected during the CNY holiday. As such, the post-holiday lead ingot inventory is highly likely to rise by around 20,000 mt (especially the in-plant inventories of smelters). Nonetheless, lead prices will have support at 15,000 yuan/mt amid routine restocking post the holiday, and the lead ingots exports in February subject to orders signed in January.

Zinc Investors Shall Go Long on Dips amid Less-than-Expected Inventory Accumulation

Currently, apart from the production suspensions in answering to environmental protection requirements, some smelters also cut the production amid pressures from the mining side. In addition, some mid and small-sized smelters in Hunan underwent longer-than-usual maintenance. The domestic refined zinc output is likely to stand at 523,000 mt in January, and 487,000 mt in February due to the CNY holiday factor, according to SMM research. The seasonal increase in zinc inventories has already surfaced as the downstream was closed for CNY holiday one after another. And the rising inventory will increasingly weigh on the prices. SMM believes that the inventory will rise by around 119,000 mt in February post the holiday, a low compared with the past few years. How fast the inventory will drop after the demand side returns to normal post the holiday is also worth of attention. SMM still advises the investors to go long on dips. Zinc prices are expected to move between 24,000-25,500 yuan/mt.

Absolutely Low Inventory Supports Nickel Prices

Nickel sulphate spot supplies have been tight currently as the production was cut on operating losses previously, according to SMM. Meanwhile, many PCAM (precursor of cathode active material) manufacturers managed to produce normally, and will maintain its output by way of self-dissolution or outsourced nickel sulphate post the CNY holiday. In this scenario, the demand for raw materials of nickel sulphate will stay high. And as the current increase in wet-process nickel intermediates and nickel matte is still limited, the raw materials that can be directly purchased and used are still mainly nickel briquettes. As such, SMM believes that the nickel briquette demand will stay resilient, and SHFE and LME nickel briquette will keep dropping with a monthly decrease of over 5,000 mt. For nickel plate, domestic nickel plate supply was still tight, and the spot premiums have been high. Though Nornickel output has been resumed, the exports to China were still unchanged. Therewith, SMM believes that the futures contract will maintain a great backwardation on the ground of continuously falling pure nickel inventory. The futures market still favours the longs amid absolutely low inventory.

Inventory Accumulation Post the CNY Holiday Will Suppress Tin Prices

The entire tin industry chain participants will gradually be closed for CNY holiday as the festival is already around the corner. Meanwhile, the tin supply and demand have remained weak. The mainstream upstream smelters will mostly be shut after January 25, according to SMM. As such, the refined tin output in January will be less impacted by the holiday factor. And the smelters will intensively resume the production around the Lantern Festival, which is expected to have a greater impact on the output in February. SMM believes that the smelters’ output in February will drop to 11,540 mt. The holiday season of downstream enterprises shows obvious regional differences. The holiday time in the Pearl River Delta region starts around the 20th of this month, and will end around the tenth of February. The enterprises in other regions will take the holiday later than those in the Pearl River Delta region, and will mostly resume the production earlier around February 8. Generally speaking, though the smelters will mostly be closed during the CNY holiday, some large-sized smelters that take up the largest shares of domestic tin output, will maintain the production during the holiday. As such, the output in February will drop only slightly from January. On the demand side, the solder companies in SMM sample will see concentrated holiday period, hence the demand will drop more palpably during the holiday. There is higher possibility that domestic tin inventory will rise amid short-term supply surplus, weighing on tin prices.

Stricter Environmental Protection Policies in Producing Areas Likely to Prompt Up Magnesium Prices

As the Chinese New Year is approaching, the downstream restocking activities have basically ended. Large-scale magnesium factories have stopped taking orders and suspended quotations. Some magnesium factories with high spot inventories chose to sell at lower prices, pulling down market prices further. According to SMM research, China's magnesium ingot output is expected to be about 75,000 mt in January. During the CNY, there is currently no production suspension or reduction plans. It is expected that China's total magnesium ingot output will remain at a high level in February. In terms of prices, considering the downstream restocking demand post the CNY holiday and the strict environmental protection rectification in Fugu, the prices of magnesium are expected to rise to a high of 45,000 yuan/mt amid laggard increases triggered by the policy end.

Post-holiday Restocking on Rigid Demand Will Underpin Silicon Metal Prices

Domestic silicon metal output in January is likely to stand at 260,000 mt as the producing areas in south-west China are still in the dry season. The silicon metal manufacturers’ operating rates post the CNY holiday will be basically flat from January. On the demand side, with the new capacities of 500,000 mt of silicone monomers and 136,000 mt of polysilicon gradually ramping up the production, and the seasonal recovery of aluminium alloy production, the overall demand for silicon metal in February will increase both year-on-year and month-on-month. It is expected that after the short-term wait-and-see sentiment arising from the holiday factor, the marginal growth of on-demand restocking and new demand will drive up the prices of silicon metal. It is expected that the prices of 553# silicon metal with oxygen will rise above 20,000 yuan/mt, and 421# silicon metal will rise above 22,000 yuan/mt, where the product has been hovering around for nearly a month.

Lithium Prices Likely to Hit New Highs amid Supply Shortage Post the CNY Holiday

Intraday carbonate lithium prices recorded high ahead of the Chinese New Year holiday. The supply side was affected by the shutdown and maintenance of the upstream lithium salt manufacturers and the production reduction of the brine lake. The output in January is expected to be about 18,700 mt, a decrease of 5% from the previous month. On the demand side, the rush to install NEV batteries and the substantial expansion of the lithium battery sector at the end of the year led to a significant increase in the demand for upstream lithium salts, with a raw material supply deficit of up to 28%, which in turn led to a jump in the market prices of lithium carbonate. It is expected that after the CNY holiday, the supply of lithium carbonate will rebound slightly as lithium salt manufacturers gradually resume work. The downstream 3C digital market has stabilised. In terms of power battery, with the continuous growth of the NEV market, the demand for NMC and LFP batteries and relative materials will rise further, sustaining the supply shortage of lithium carbonate. It is estimated that the transaction prices may continue to rise approaching the 400,000 yuan/mt mark post the CNY holiday.

Post-CNY Holiday Cobalt Prices Will Move Upwards with Rising Overseas Quotes

The output of cobalt sulphate in January will be about 5,900 mt in metal content, and the output of cobalt chloride will stand at 4,400 mt in metal content. With the approaching of the Chinese New Year, the downstream has basically completed their pre-holiday restocking, and the price has demonstrated steady increases. However, the prices of cobalt salts jumped slightly recently due to a temporary surge in demand generated by terminal orders. A number of cobalt salt manufacturers will take holidays or undergo maintenance during the CNY. It is expected that the output of cobalt sulphate and cobalt chloride will drop by about 630 mt and 380 mt in metal content respectively. The costs of cobalt salt post the CNY holiday will continue to rise slightly following the hike of overseas refined cobalt quotes. And the supply of cobalt salt will rise slightly with the resumption of work. The demand side is likely to pick up driven by the post-holiday resumption of production, but will shrink soon with the arrival of the off-season in the electronics sector. In terms of prices, considering that there is still great uncertainty in the arrivals of intermediate products from overseas after the CNY holiday, the prices of cobalt salt may remain stable or rise slightly. The prices of cobalt sulphate are expected to move between 108,000-110,000 yuan/mt, and the prices of cobalt chloride will be 126,000-128,000 yuan/mt.

Rebar Prices Will Gain Strong Support from the Demand Side Post the CNY

On the supply side, the restrictions of domestic steel production in 2022 have not yet been clarified. It is expected that the blast furnace (BF) mills in south China may maintain normal production. However, the profits and sales of steel plate/sheet have been slightly better than those of rebar recently, and the production enthusiasm for rebar has weakened slightly.

In the short term, it is expected that the output of rebar will remain at a low level in February under the influence of factors such as the production restrictions for Beijing Winter Olympics, the early holiday of electric arc furnace (EAF) and rolling mills that produce rebar, as well as the slow resumption of production.

In terms of demand, the terminals and steel traders are on holiday one after another approaching the CNY, and many markets have been closed, hence the demand is basically stagnant. In the medium and long term, the People’s Bank of China cut the one-year and five-year LPR, which will help revive the supply and consumption ends of the real estate market. The director of the Financial Market Department of the People's Bank of China said that recently, the real estate sales, land purchases, financing and other activities have gradually returned to normal, and market expectations have improved steadily. The Bureau of Statistics also stated that the investments in infrastructure construction are being carried out ahead of time when deemed appropriate, and significant projects in many places have started intensively. According to the government work reports that have been released of local authorities and the 2022 work plans announced by the development and reform commissions of various places, it has become a key task to actively promote the construction of projects and ensure that the investment in the first quarter. Hence the post-holiday demand can be expected.

On the whole, the short-term spot prices may remain stable and run in a narrow range. And with the recovery of demand post the CNY holiday, the prices of steel will show upside potentials. However, a slow recovery in the real estate sector will limit the upside room of prices. The international market has been relatively turbulent recently, and the market shall stay cautious about the influences of the peripheral markets. The SMM average price of rebar was 4,746.3 yuan/mt as of January 25, and is expected to move between 4,650-5,250 yuan/mt post the CNY holiday.

HRC Prices Will Be Strongly Supported by the Infrastructure Construction

On the supply side, the recent Winter Olympics-oriented production restrictions have been issued one after another. Taking Tangshan City as an example, in the first quarter of 2022, the total crude steel output affected by the off-peak production scheme in Tangshan City will be around 8.91 million mt, close to 30% of the output in the same period in 2021. The 2+26 cities that demand off-peak production during the Winter Olympics cover 47% of the domestic RHC production capacity. Under the influence of the Winter Olympics and environmental protection production restrictions, the supply of HRC will drop significantly in the first quarter of 2022.

On the demand side, a series of macro policies, including infrastructure investment, newly-started construction projects, interest rate and RRR cuts, tax and expense cuts, etc., have served as a combination tool to the demand. To sum up, HRC will see narrowing supply and gradual recovery of demand after the CNY holiday. The SMM average price of domestic HRC stood at 4,882 yuan/mt as of January 25. It is expected that in the first quarter after the holiday, the HRC prices will fluctuate between 4,810-5,400 yuan/mt with strong upside momentum.

Coke Prices Likely to Drop amid Weakening Demand

On the supply side, after three consecutive rounds of coke price hikes in January, the profits of coking enterprises have increased significantly, heightening the enthusiasm for production. However, considering that coking enterprises may face stricter environmental protection inspections around the Chinese New Year, there is limited room for improvement in coke supply.

In terms of demand, affected by the repeating COVID-19 pandemic and adverse weather like rain and storm, the shipments of coke have been poor recently. From February to mid-March, the Winter Olympics-related production restrictions on steel mills in north China will lead to a decrease in the demand for coke, and the bargaining power is mainly in the hands of steel mills in north China, hence there is few possibility that coke prices will rise post the CNY holiday. The prices of quasi-first-grade metallurgical coke (CDQ) will move between 3,300-3,500 yuan/mt.

Iron Ore Prices Will Encounter Pressures from Weakening Demand

Supply: The mining blocks in Brazil have resumed the production from the heavy rains, and overseas shipments will gradually return to normal in the future. In addition, the current port inventory is still at a high level of 150 million mt, hence the overall supply in the first quarter will remain sufficient.

Demand: As the Winter Olympics are approaching, the production of steel mills in north China will be restricted since January 31. Meanwhile, as the probability of heavy air pollution in north China is high during the Winter Olympics, temporary control could be expected. It is expected that the environmental protection requirements and production restrictions in Beijing, Tianjin and Hebei and surrounding areas will be more stringent during the Winter Olympics, and the output of pig iron will drop significantly and stand at 2.1 million mt in February.

Iron ore prices will hence pull back amid sluggish demand in the first week post the CNY holiday. And the prices will remain flat over the pre-holiday level. After the Lantern Festival, the steel mills in east China and south China will basically exhaust the stocks built ahead of the holiday, and the demand will increase slowly. The steel mills in the northern region will resume the production intensively in early March after the Winter Olympics, which is expected to provide strong support for iron ore prices. To sum up, SMM believes that the iron ore prices will fluctuate between 115-140 yuan/mt throughout the entire first quarter.

![Titanium Market Structure Becomes Clearer: Upstream Consolidates at Weak Levels, Midstream and Downstream Strength Expected [SMM Titanium Weekly Review]](https://imgqn.smm.cn/usercenter/tjmLW20251217171722.jpeg)