SHANGHAI, Dec 31 (SMM) - This is a roundup of China's metals weekly inventory as of December 31.

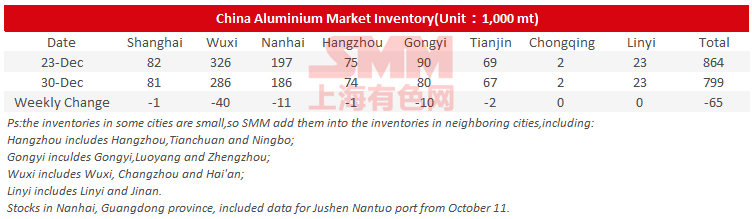

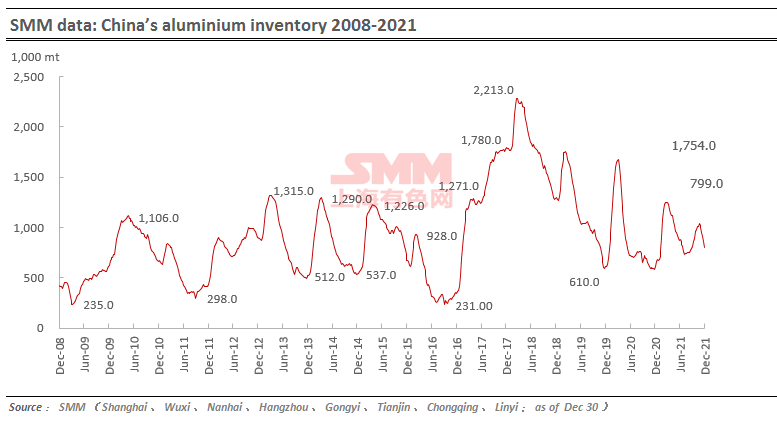

Aluminium Social Inventories Dropped 65,000 mt on Week

SMM data showed that China's social inventories of aluminium across eight consumption areas dropped 65,000 mt on the week to 799,000 mt as of December 30, mainly contributed by Wuxi, Nanhai and Gongyi. The social inventories dropped 40,000 mt from Monday December 27 largely because the arrivals in Wuxi declined significantly.

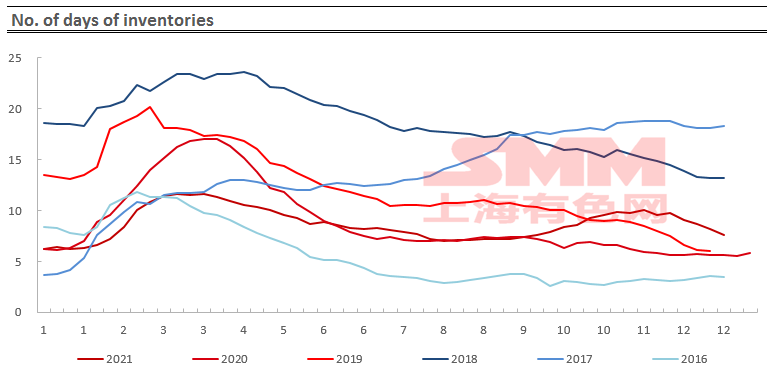

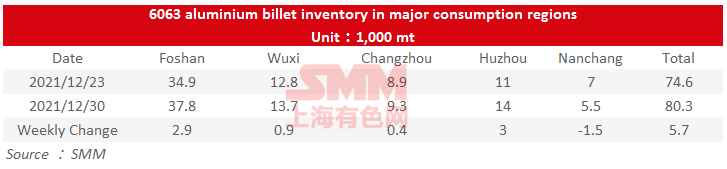

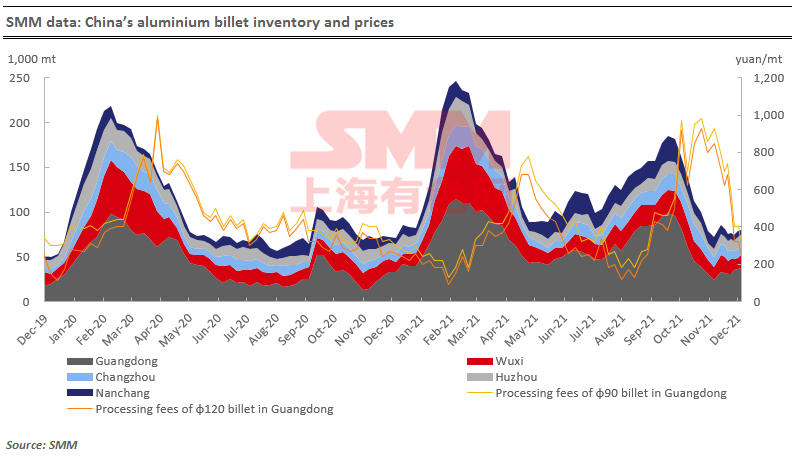

Aluminium Billet Inventories Up 5,700 mt on Week

The stocks of aluminium billet in five major consumption areas added 5,700 mt to 80,300 mt on December 30 from a week ago, an increase of 7.64%.

The inventories across four major markets rose on the week except for Nanchang. Among them, the inventory in Huzhou rose 3,000 mt or 27.27% from last Thursday, and that in Foshan added 2,900 mt or 8.31%, both of which contributed most of the weekly gains. The aluminium billet market was subdued by the year-end as most companies were busy with managing cash flows and reduced the orders taken, resulting in a quiet market.

Looking into next week, the downstream market was sluggish in demand, coupled with the upcoming New Year’s Day holiday. It is expected that the weekly inventory of aluminium billet will continue to rise.

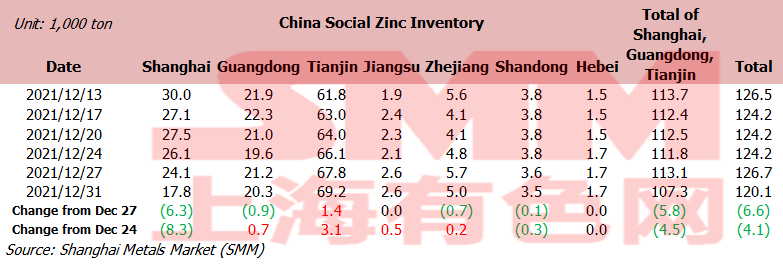

Zinc Social Inventories Down 4,100 mt On Week

SHANGHAI, Dec 31 (SMM)—Total zinc inventories across seven Chinese markets stood at 120,100 mt as of December 31, down 6,600 mt from December 27 and 4,100 mt from December 24.

Shanghai saw a decrease in the stocks as the inflows of imported zinc thinned, some domestic zinc brands were still in transit and the arrivals of goods in the market declined sharply, and downstream producers properly restocked before the holiday. The inventory in Guangdong rose slightly amid muted arrivals of goods in the market and falling demand from downstream producers. The stocks in Tianjin continued to increase as the arrivals of goods stabilised, downstream demand was sluggish and traders have demand of delivering futures goods. Inventories in Shanghai, Guangdong and Tianjin fell 4,500 mt, and inventories across seven Chinese markets decreased 4,100 mt.

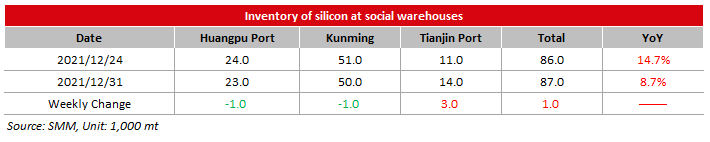

Silicon Metal Social Inventory Increased 1,000 mt on Week

The social inventory of silicon metal across Huangpu port, Kunming city and Tianjin port increased 1,000 mt from the previous week to 87,000 mt as of Friday December 31.

The inventory in north China increased, while the inventory in south China declined.

The arrivals at Tianjin port increased significantly as all people from other cities will have to obtain a COVID-19 negative certification within 48 hours to enter Tianjin from January 1 to March 15, 2022. At the same time, the shipments from Tianjin port remained sluggish. The inventory at Tianjin port rose.

The shipments in south China were high this week, and the arrivals at Kunming and Huangpu port declined. Therefore, the inventory in south China decreased.

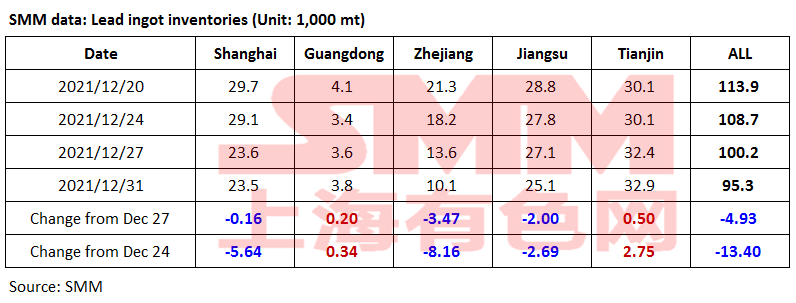

Lead Ingot Social Inventory Fell 13,400 mt on Week

The social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin decreased 13,400 mt from December 24 and 4,900 mt from December 27 to 95,300 mt as of December 31.

The supply of secondary lead shrank in Jiangxi, Anhui, and other major consuming markets due to environmental protection inspections and maintenance. However, the lead prices declined during the week, and the primary lead smelters’ shipments were modest, mainly shipping the goods under long-term orders. The downstream users restocks raw materials on demand approaching the New Year's Day, so they increased the purchases from traders. As such, the social inventory continued to decline.

The smelters will gradually resume the supply after the New Year's Day holiday next week, and the downstream users will keep restocking for the CNY. The social inventory of lead ingots is expected to keep falling.

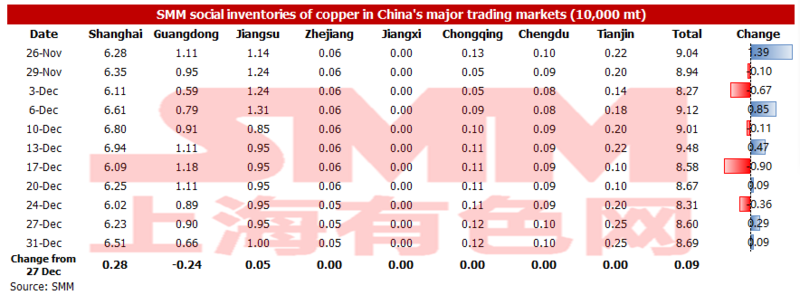

Copper Inventory in Major Chinese Markets Added 900 mt over Weekend

As of Friday December 31, the copper inventory across major Chinese markets increased 900 mt from Monday December 27 to 86,900 mt. The increase in the inventory this week was mainly seen in Shanghai and Jiangsu. The inventories in Guangdong declined, and there has been little change in the inventories across other regions.

Specifically, the inventory in Shanghai increased by 2,800 mt to 65,100 mt, the inventory in Jiangsu added 500 mt to 10,000 mt, and the inventory in Guangdong fell 2,400 mt to 6,600 mt. The consumption in various regions was poor this week. The arriving shipments in east China increased due to the influx of imported copper and the cargoes from north China. On the other hand, the lower efficiency of transportation in Guangxi due to the COVID-19 pandemic and the maintenance at smelters reduced the shipments arrivals in Guangdong.

The consumption is expected to be weak next week. The supply will grow. The inventories are expected to increase further.

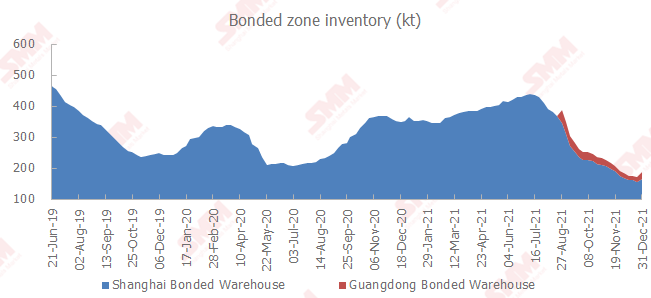

Copper Inventory in China Bonded Zone Grew 15,600 mt on Week

The copper inventories in the domestic bonded zones grew 15,600 mt from December 24 to 187,300 mt as of Friday December 31, the first increase after 11 consecutive weeks of decline, according to the most recent SMM survey.

The inventory in the Shanghai bonded zone increased 7,700 mt to 164,500 mt, and the inventory in the Guangdong bonded zone increased 7,900 mt to 22,800 mt.

The trades in the import market was subdued at the end of the year. The severe import losses also depressed the import demand, reducing the shipments from bonded zone inventories. The concentrated arriving shipments over the past two weeks went to the bonded warehouses. Therefore, the inventory in China’s bonded zones stopped falling and rebounded.

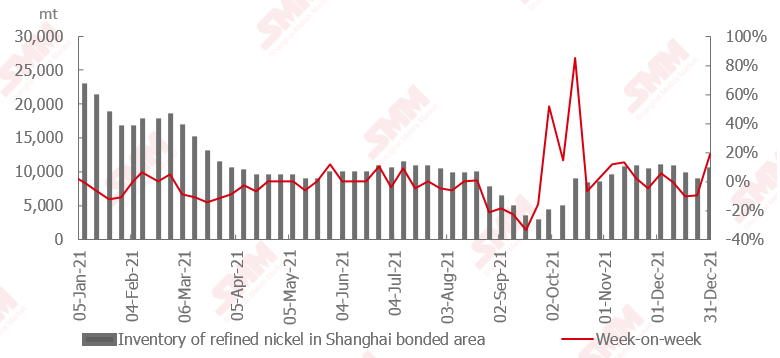

Nickel Ore Inventories at Chinese Ports Fell 65,000 wmt

The nickel ore inventory at Chinese ports dipped 65,000 wmt from a week earlier to 8.59 million wmt as of December 31. Total Ni content stood at 67,500 mt. The total inventory at seven major ports stood at around 3.89 million wmt, a drop of 65,000 wmt from a week earlier.

The port inventory continued its downward trend, but the decline was relatively slow. The arriving shipments and loading both slowed down. The port unloading pressure has weakened compared with the previous period. Some NPI plants may have plans to undertake maintenance in January. The port inventory may rebound slightly.

Imports of Spot Nickel Saw Slight Profits

The SHFE/LME nickel price ratio hovered at highs this week, rising to 7.49 before falling, and then stabilising at 7.44. The import saw small profits of 250 yuan/mt.

As the long-term contracts of pure nickel for 2021 were completed, most of the traders were busy with annual settlements and stopped business operations. Therefore, the import volume of pure nickel from bonded zone inventories was small even as the import window opened. There were 2,000 mt of shipments arrivals of nickel plate this week. It is expected that those shipments will be offered for sale in the domestic market next week. But the SHFE/LME nickel price ratio is expected to remain profitable for the import due to the low domestic inventories.