SHANGHAI, Dec 24 (SMM) - This is a roundup of China's metals weekly inventory as of December 24.

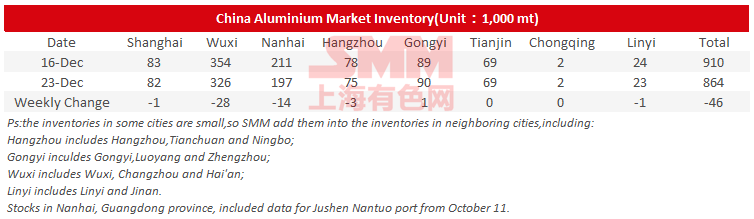

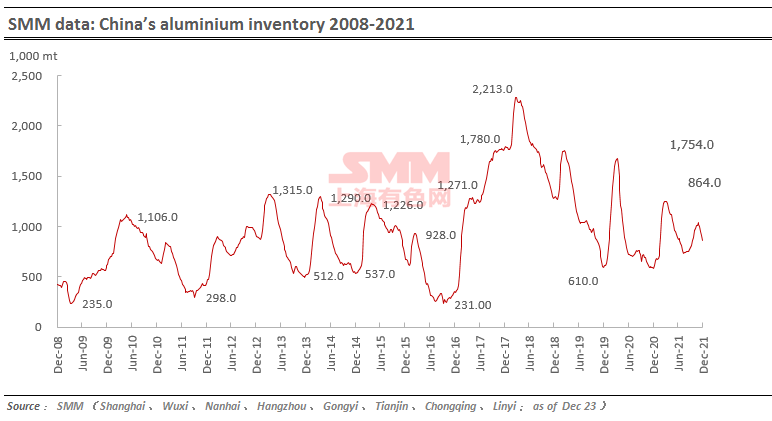

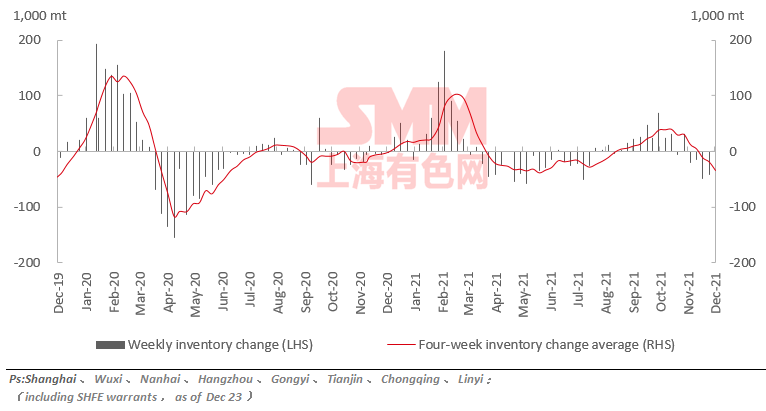

Aluminium Social Inventories Dropped 46,000 mt on Week

SMM data showed that China's social inventories of aluminium across eight consumption areas dropped 46,000 mt on the week to 864,000 mt as of December 23, mainly contributed by Wuxi and Nanhai. The inventory in Gongyi rose slightly on the week.

The social inventories dropped 27,000 mt from Monday December 20 mainly owing to the declining arrivals in Wuxi.

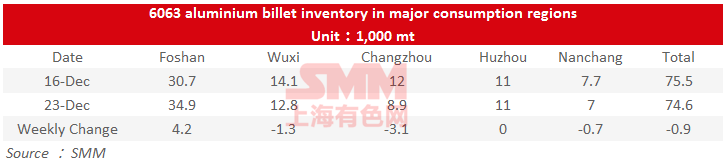

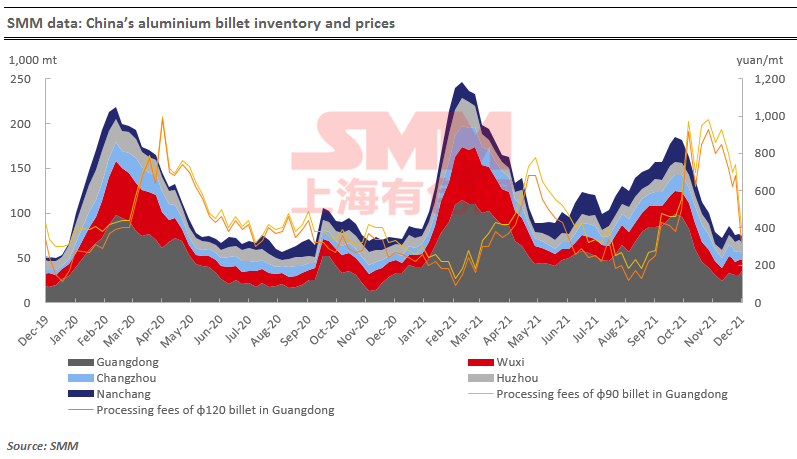

Aluminium Billet Inventories Down 900 mt on Week

The stocks of aluminium billet in five major consumption areas dropped 900 mt to 74,600 mt on December 23 from a week ago, a decrease of 1.19%.

Only the inventory in Foshan rose on the week by 4,200 mt or 13.68%, and the inventories in Wuxi, Changzhou and Nanchang all declined, with Changzhou (down 3,100 mt or 25.83%) contributing most of the decreases. According to the warehouses, the weekly arrivals of aluminium billet were still at a low level as the manufacturers were less interest in making shipments amid falling RCs. Some aluminium billet manufacturers even planned to reduce their production.

Looking into next week, the downstream market was muted in demand by the year-end. Hence there is a higher possibility that the weekly social inventory of aluminium billet will rise.

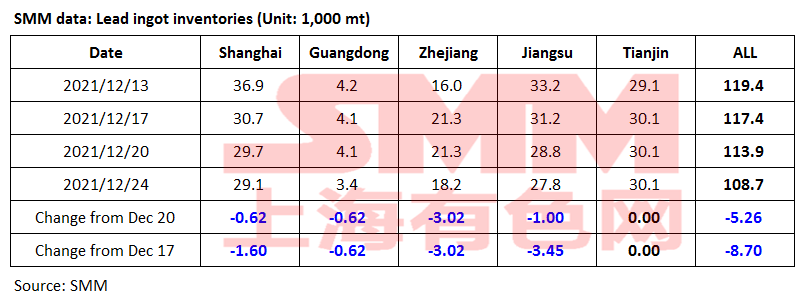

Lead Ingot Social Inventory Dropped 5,300 mt on Week

The social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin decreased 8,700 mt from December 17 and 5,300 mt from December 20 to 108,700 mt as of December 24.

The enterprises from the lead industry chain are collecting funds more actively in late December. The smelters and traders increased shipments. The traders mostly shipped goods at discounts to reduce the product inventories. The quotations of lead ingots in Jiangsu, Zhejiang, and Shanghai stood at discounts of 70-0 yuan/mt over SHFE 2201 lead contract. The discounts of goods from smelters expanded to 200-250 yuan/mt. The smelters quoted for small orders at discounts of 150-0 yuan/mt over the average price of SMM 1# lead, and the downstream users purchased on demand. Some downstream enterprises advanced their purchases for restocking as they would close for settlement this week.

The primary lead smelters will further resume the production after maintenance next week, and the lead ingot social inventory may drop more significantly as the enterprises may close the trade.

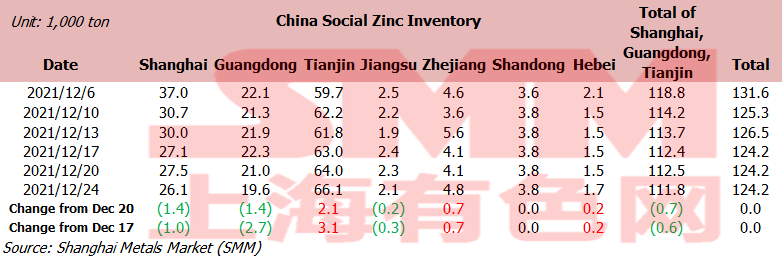

Zinc Social Inventories Flat on Week

Total zinc inventories across seven Chinese markets stood at 124,200 mt as of December 24, flat from December 20 and December 17.

The inventory in Shanghai declined as the imported zinc available in the market thinned and some leading producers reduced the production. Stocks in Guangdong continued to decline as the arrivals of goods declined after the price spread between Shanghai and Guangdong widening. The inventory in Tianjin continued to accumulate amid stable arrivals of goods at smelters and falling demand from downstream producers. Inventories in Shanghai, Guangdong and Tianjin fell 600 mt, and inventories across seven Chinese markets were flat.

Imports of Spot Nickel Saw Slight Profits

The SHFE/LME nickel price ratio stood at 7.44 this week, and the import profits stood at 250 yuan/mt. Traders continued to move cargoes into the domestic market from bonded zone inventories. But the inventory growth in Shanghai was not significant as some of the cargoes had been presold and delivered to the downstream buyers.

The domestic pure nickel inventory will remain at a low level next week. And the low inventory will not improve fundamentally until large volumes of imported cargoes arrive. The shipments arrivals are expected to stand at 1,500-2,000 mt next week, which is not large. The SHFE/LME nickel price ratio is expected to remain high.

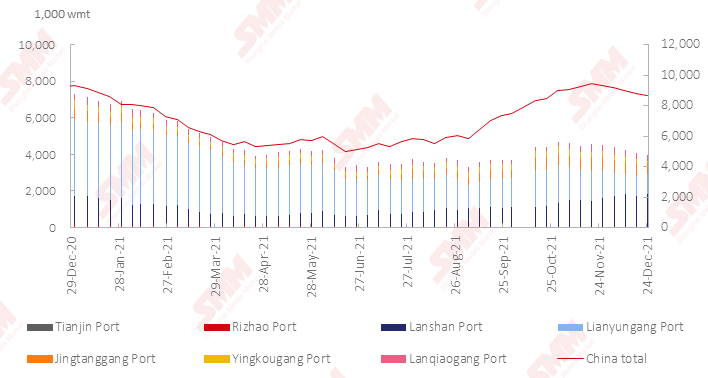

Nickel Ore Inventories at Chinese Ports Fell 118,000 wmt

The nickel ore inventory at Chinese ports dipped 118,000 wmt from a week earlier to 8.66 million wmt as of December 24. Total Ni content stood at 68,000 mt. The total inventory at seven major ports stood at around 3.96 million wmt, a drop of 108,000 wmt from a week earlier.

The nickel ore inventories have fallen for five consecutive weeks since the end of November as the imports have decreased significantly. However, the downstream demand is also relatively weak due to the current high costs and the impact of environmental protection and production restrictions in some areas. Hence the inventory decline was not noticeable.

It is expected that the production situation of downstream plants will remain unchanged before the Chinese New Year, and the decline of nickel ore port inventory will continue.

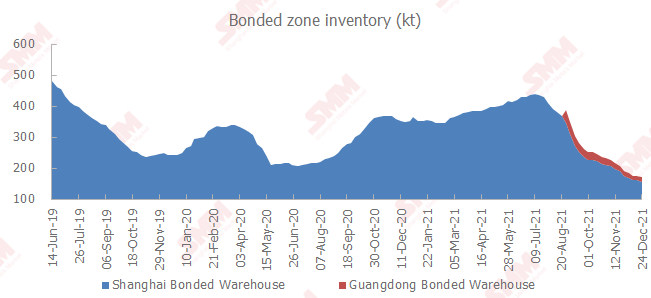

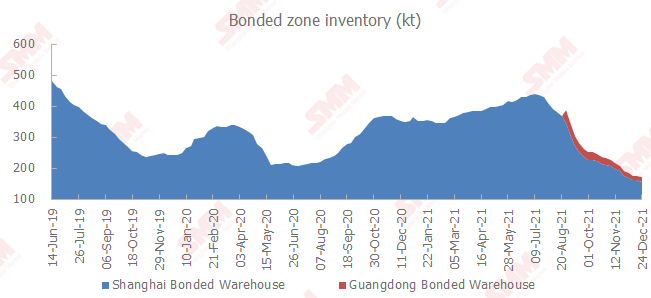

Copper Inventory in Domestic Bonded Zone Declined 2,200 mt on Week

The copper inventories in the domestic bonded zones decreased 2,200 mt from December 17 to 171,700 mt as of December 24, falling for 11 consecutive weeks, according to SMM survey.

The inventory in the Shanghai bonded zone dipped 3,700 mt to 156,800 mt, and the inventory in the Guangdong bonded zone grew 1,500 mt to 14,900 mt. The spot trades are sluggish at the year-end. The import losses exceeded 500 yuan/mt due to the poor SHFE/LME copper price ratio, weakening the demand for customs declaration.

As far as SMM understood, there were concentrated arriving shipments this week and those cargoes are expected to go to the bonded zone next week. The bonded zone inventories will thus grow.

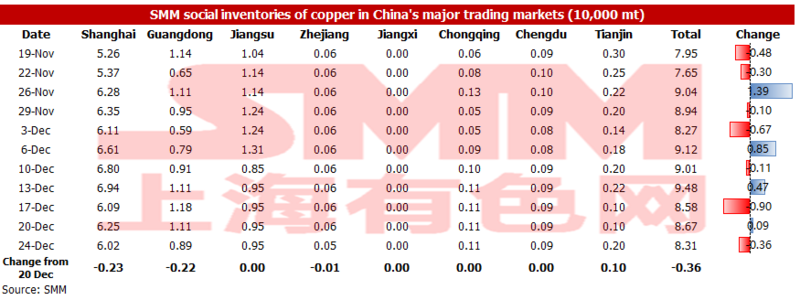

Copper Inventory in Major Chinese Markets Dipped 3,600 mt on Week

As of Friday December 24, copper inventory across major Chinese markets fell 3,600 mt from Monday to 83,100 mt. The inventory decline was milder than the previous week. The inventory in Tianjin increased slightly by 1,000 mt, while the inventory decreased across Shanghai, Guangdong and Zhejiang. And there was little change in the inventories in other regions.

Specifically, the inventory in Shanghai decreased by 2,300 mt to 60,200 mt, the inventory in Guangdong dipped 2,200 mt to 8,900 mt, and the inventory in Zhejiang fell 100 mt to 500 mt. The consumption was weak in various regions this week. And lower arriving shipments drove the inventory decline. The shipments arrivals of imported copper decreased due to the tax control issues. And the logistics efficiency for domestic copper decreased noticeably due to the COVID-19 pandemic in various regions.

Consumption is expected to weaken further in the last week of the year. The market shall pay attention to whether the shipments arrivals will increase next week. SMM expects the shipments arrivals of imported copper will increase next week, and the delivery volume from smelters will also increase at the end of the year. Therefore, SMM expects that domestic inventories will increase slightly next week.