SHANGHAI, Nov 12 (SMM) - This is a roundup of China's metals weekly inventory as of November 12.

Copper Inventory in Major Chinese Markets Decreased 12,600 mt on Week

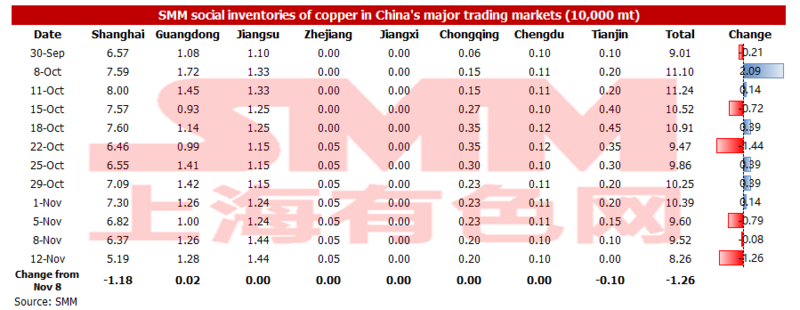

The copper inventories across major Chinese markets fell 12,600 mt from a week earlier to 82,600 mt as of Friday November 12, according to SMM data, which is also the first time the inventory fell below 90,000 mt this year.

The declines were mainly contributed by Shanghai and Tianjin, with the inventory of the former city reducing 11,800 mt to 51,900 mt amid less arrivals from domestic market (some has been exported) and decreased volume of imported copper that cleared customs. The inventory in Tianjin dropped 1,000 mt to around 0 mt, as the downstream sector mostly consumed copper from social and in-house warehouses in a time when the copper cathode in north China was unable to be transported to south China amid cold weather. Guangdong saw an increase of 200 mt in inventory, which rose to 12,800 mt amid more arrivals from overseas and domestic market, including Fujian and Jiangxi.

Going forward, the copper inventory will probably drop again due to limited arrivals of imported copper, export plans of domestic smelters and news that there will be no releases of national reserves this month. And the consumption is likely to pick up after the delivery of SHFE contracts.

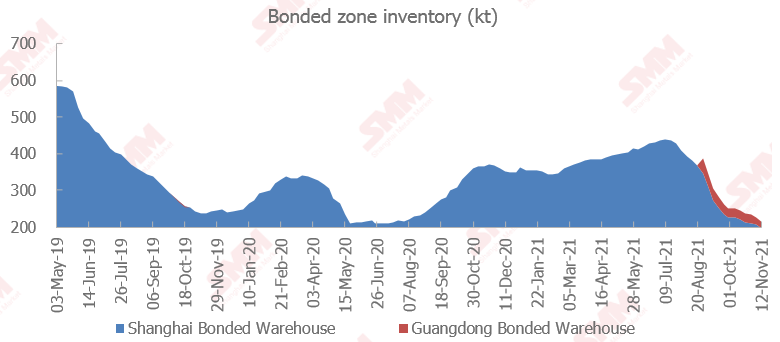

Copper Inventory in China Bonded Zone Dipped 10,700 mt on Week

The copper inventories in the domestic bonded zones declined 10,700 mt from November 5 to 216,200 mt as of Friday November 12, the fifth consecutive week of decline, according to the most recent SMM survey.

Among them, the inventory in Shanghai bonded zone dropped 8,700 mt to 187,700 mt, and that in Guangdong declined 2,000 mt to 18,500 mt. The total inventories in the bonded zones remained the downward trend, mainly as the arrivals at ports were at a low level. While the exports by domestic smelters continued, pushing down the inventory in bonded zone.

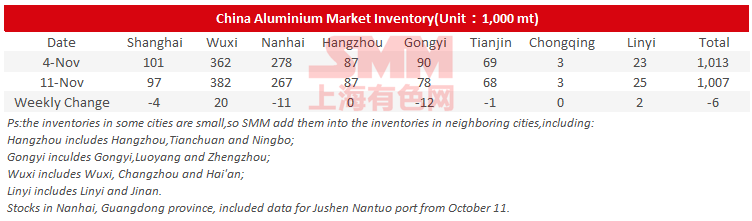

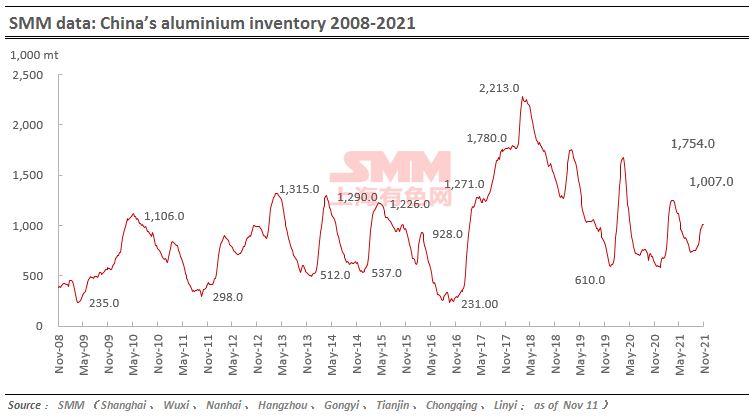

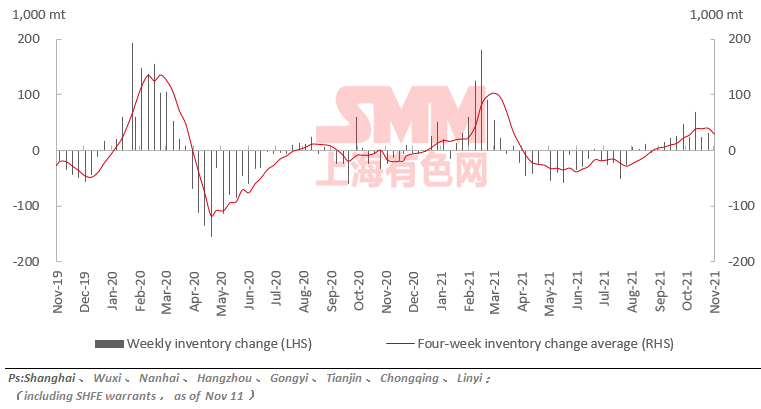

Aluminium Social Inventories Dropped 6,000 mt on Week

SMM data showed that China's social inventories of aluminium across eight consumption areas dropped 6,000 mt on the week to 1.007 million mt as of November 11, mainly contributed by Nanhai, Shanghai and Gongyi. The inventory in Wuxi continued to rise. And how the blizzard in north China will impact the transportation is worth constant attention.

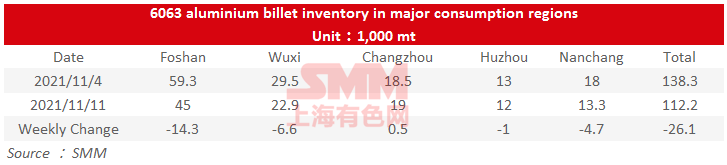

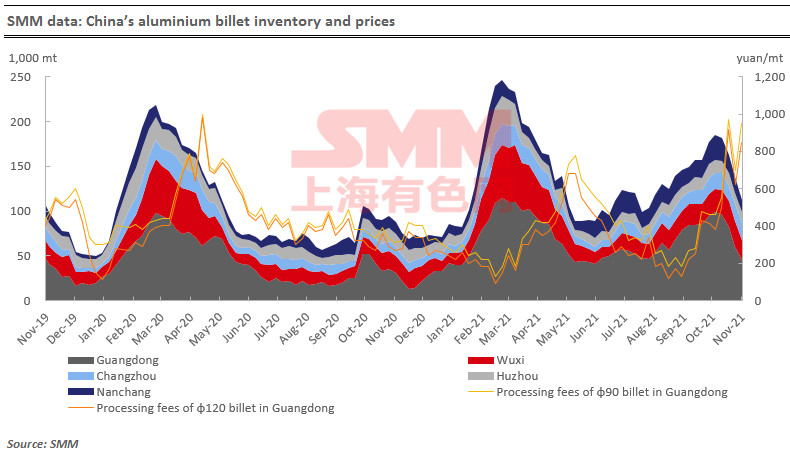

Aluminium Billet Inventories Down 26,100 mt on Week

The stocks of aluminium billet in five major consumption areas dropped 26,100 mt to 112,200 mt on November 11 from a week ago, a decrease of 18.87%. And the inventory has been falling for four straight weeks.

The decline still mainly came from Foshan, whose inventory dropped 14,300 mt or 24.11% on the week, followed by Wuxi (down 6,600 mt or 22.37%). The inventories in Nanchang and Huzhou also declined slightly, while that in Changzhou rose mildly from a week ago by 500 mt or 2.7%. According to SMM, the transportation of aluminium billet was partly disrupted by blizzard in north-west China and resurging COVID, leading less arrivals at social warehouses. While the easing power rationing, especially n Zhejiang and Jiangsu, has created more demand.

Looking forward, the orders and production activities across all aluminium extruders have been moderate according to SMM research. While the warehouses reported that there will be no extra arrivals of aluminium billet next week. As such, the aluminium billet inventory is likely to remain in the downward trend.

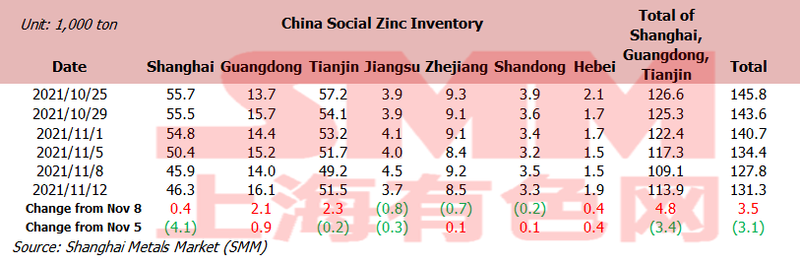

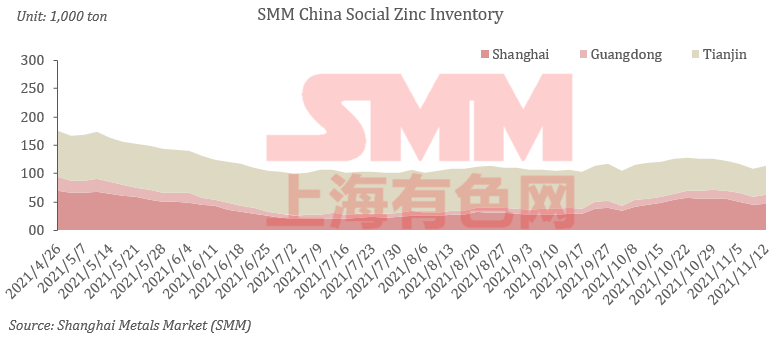

Zinc Social Inventories Down 3,100 mt on Week

Total zinc inventories across seven Chinese markets stood at 131,300 mt as of November 12, down 3,100 mt from November 5 and up 3,400 mt from November 8. The inventory added within the week, but dropped from last Friday.

In Shanghai, the downstream sector purchased on dips, leading to more shipments from warehouses over the weekend; while the demand has been modest this week. The inventory in Guangdong rose slightly amid more arrivals after the power rationing toward smelters loosened. Tianjin saw less declines in inventory as the arrivals picked up while downstream demand weakened.

As such, the combined inventory in Shanghai, Guangdong and Tianjin dropped 3,400 mt on the week, and that across seven regional declined 3,100 mt.

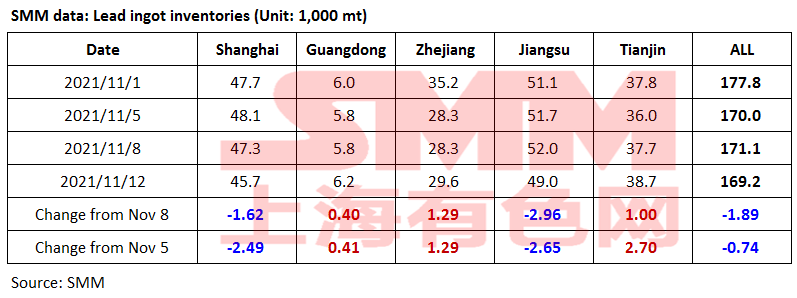

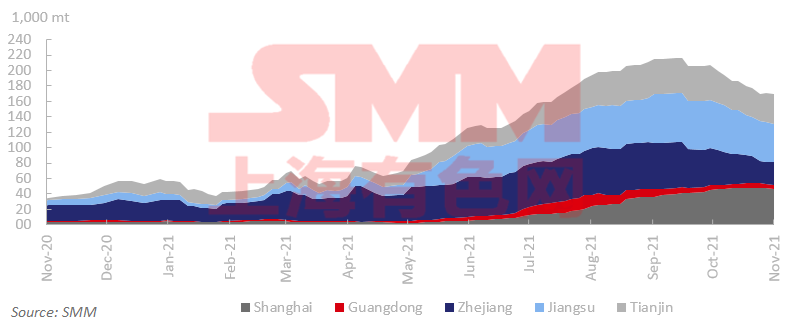

Lead Ingot Social Inventory Fell 700 mt on Week

The social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin decreased 700 mt from November 5 and dropped 1,900 mt from November 8 to 169,200 mt as of Noember 12.

The lead ingot supply varied by region. The power rationing in Anhui was alleviated, but the technological transformation and maintenance suppressed the production. The secondary lead smelters in Shanghai and Jiangsu lowered the operating rates due to the technological transformation, and the downstream users turned to consume the in-house inventories. The lead ingots shipped from the plants gradually arrived at the social warehouses before the delivery of SHFE 2111 lead contract. The social inventory of lead ingots may not increase next week amid power rationing, maintenance, and technological transformation.

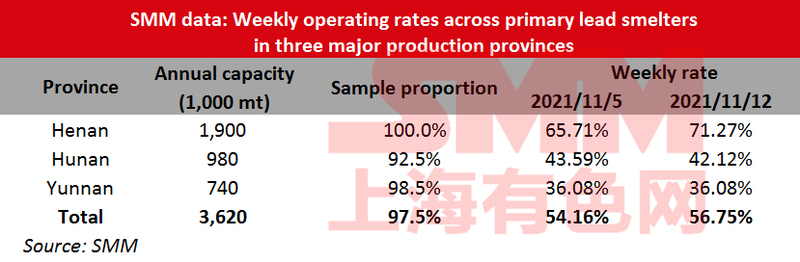

Operating Rate across Primary Lead Smelters Rose 2.59% on Week

The average operating rate across primary lead smelters in Henan, Hunan and Yunnan provinces gained 2.59 percentage points from the previous week to 56.75% in the week ended November 12, an SMM survey showed.

Henan Jinli Co., and Wanyang Co. in Jiyuan City resumed the normal production this week. Wanyang started the maintenance for crude lead production lines, which had little impact on the refined lead production. Wanyang will maintain the normal production of refined lead next week. In Hunan, Shuikoushan Zhihui has not resumed the production, while other smelters maintained the normal production. Jiangxi Jinde, and Jianxi Copper were remained under maintenance.

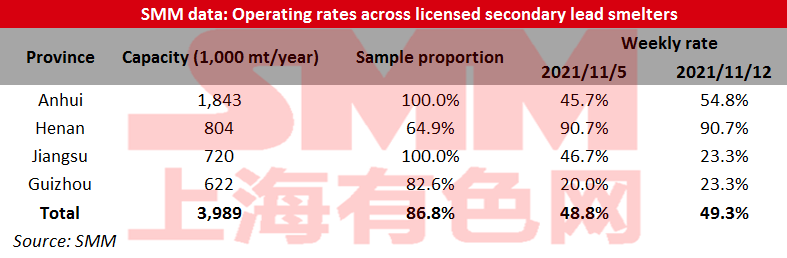

Operating Rate across Secondary Lead Smelters Up 0.43% on week

The operating rates across licensed smelters of secondary lead in Jiangsu, Anhui, Henan and Guizhou averaged 49.28% in the week ended November 12, up 0.43 percentage point from the previous week, an SMM survey showed.

The operating rates of secondary lead smelters rose on the week as estimated partly because the production of smelters in Anhui resumed in an orderly manner as the high voltage power supply adjustment in some industrial parks came to an end. On the other hand, the output in Anhui also picked up as the production resumed after the environmental impact assessment was completed. Meanwhile, the production of new capacities ramped up in Guizhou amid moderate profits. The power rationing in Jiangsu was not impacting the local production, but the output still dropped due to the technique update of some smelters. As such, the operating rates of the four regions rose slowly.

Going forward, more smelters will recover from the power rationing. But the technique upgrade may result in another week’s suspension of production. Hence, the overall output will maintain minimal gains.

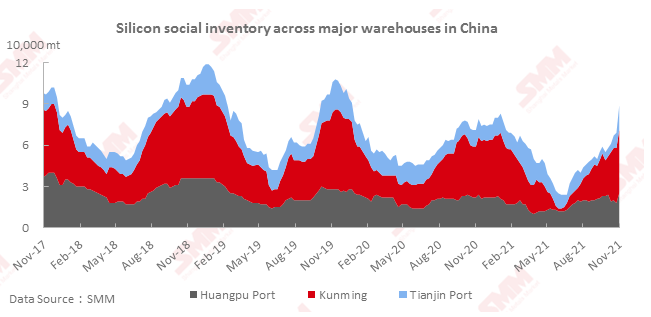

Silicon Metal Inventory Expanded 20,000 mt on Week

The social metal inventory of silicon metal across Huangpu port, Kunming city and Tianjin port increased 20,000 mt from the previous week to 89,000 mt as of Friday November 12.

The inventory at Tianjin Port increased as the shipments from silicon metal factories in Xinjian arrived. Huangpu Port saw palpable increase in inventory as the traders actively made shipments to the port as the scheduled delivery is approaching. The silicon metal factories in Yunnan maintained high operating rates, and the in-plant inventory kept being transported to Kunming.

It is worth noticing that the YoY growth of social inventory has changed from negative growth to positive readings for the first time since May, 2021. The inventory at ports may decline in the following week after the goods were shipped to overseas markets. But the inventory in Kunming is likely to rise.

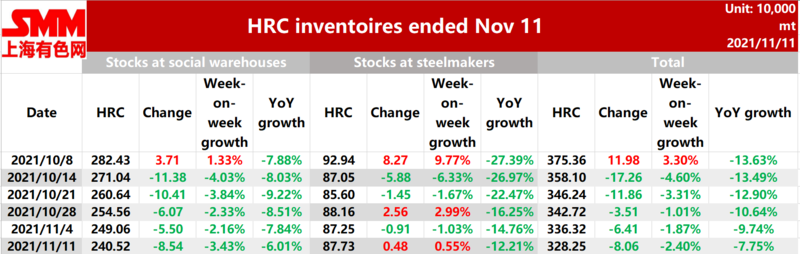

China HRC Stocks Down 80,600 mt on Week

SMM data showed that HRC stocks across social warehouses and steel makers fell 80,600 mt or 2.4% on the week, a decrease of 7.75% than a year ago, to 3.28 million mt in the week ended November 11.

The social and total HRC inventories both dropped more quickly this week, while in-plant inventory rose slightly. From the supply side, the output in east China picked up slightly, and south China also saw ramped up production amid loosening power rationing and end of maintenance. Only the output in north China dropped from a week ago. And in terms of demand, the market was in panic amid wild volatility of prices, and the traders in some regions rushed to sell off, especially east China. As such, the HRC inventory kept falling.

The inventory across social warehouses decreased 85,600 mt or 3.43% week on week to 2.41 million mt, which is 6.01% lower than a year ago.

The social HRC inventory declined at a faster pace this week, and the declines were mainly contributed by east China. The traders in Shanghai and Zhangjiagang lowered their offers to promote the sales, and the terminal sector also purchased more goods when the spot market saw wild fluctuations in prices. The social inventory in north, central and south-west China maintained normal speed of consuming goods. The inventory in south China rose slightly as the transaction in the region has been poor. In general, the social inventory continued to decline.

HRC stocks at social warehouses

The stocks at Chinese steel makers came in at 877,300 mt, up 4,800 mt or 0.55% week on week and down 12.21% year on year.

The in-plant inventories in east and south China were stable or rose slightly this week, except north China. The in-plant inventory rose slightly as a whole amid plummeting spot HRC prices, losses among traders, and broad bearish sentiment.

HRC stocks at steelmakers

The apparent consumption of HRC was still on the rise, while the supply and demand were both weak. The near-term HRC inventory is likely to sustain the downward trend should there be no palpable increase in supply.

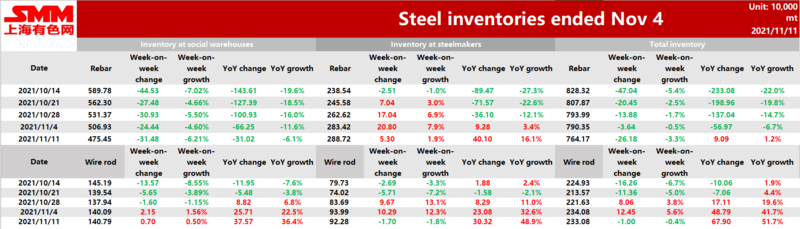

China Rebar Inventory Shrank 261,800 mt on Week

The inventory of rebar across Chinese steel makers and social warehouses stood at 7.64 million mt as of November 11, down 261,800 mt or 3.3% from a week earlier. Stocks are 90,900 mt or 1.2% higher from a year earlier.

The inventory at Chinese steel makers increased 53,000 mt or 1.9% from a week earlier, and stood at 2.89 million mt. And stocks are 401,000 mt or 16.1% higher than the same period last year.

The in-plant inventory increased more slowly from a week ago. The spot prices in north China dropped significantly, and downstream demand also weakened amid extreme weather, resulting in slightly rising inventory. Meanwhile, some steel mills in Shanxi said that they will mostly reduce their output if the profits keep shrinking. Hence, the follow-up inventory in north China will face less pressures. The demand in east China has been modest, and some traders in mainstream cities reports tight supply and insufficient supply of products with certain specification. Thus the local inventory rose much slowly compared with last week. The transaction in south China improved greatly from a week ago, and the downstream actively purchased on dips, pushing the originally rising inventory to the downward trajectory.

The inventory at social warehouses declined 314,800 mt or 6.21% on the week and stood at 4.75 million mt, down 310,200 mt or 6.1% from a year ago.

The social inventory dipped more significantly from a week ago, but the situation diverged by region. The social inventory in east China declined the most. The market supply dropped, and terminal demand performed moderately. While the traders in north China actively sold off, leading a palpable declines in social inventory. While the terminal demand in north-east China shrank drastically, resulting in slight increase in social inventory.

The apparent consumption of construction steel picked up this week, boosting market confidence. On the supply side, the slumping spot prices have fallen below the break-even point of most steel mills, thus some mills in east and north China are planning to reduce their output. And the output may decline further should the profits continue to fall. Hence, the follow-up supply will remain at a low level or even drop to some point.

On the demand side, the downstream demand was sluggish ahead of the winter and amid resurging COVID, which is likely to stay weak in the short term. In general, the near-term construction steel prices may gain some support from unchanged demand and shrinking supply. And the inventory may keep falling in the short term.

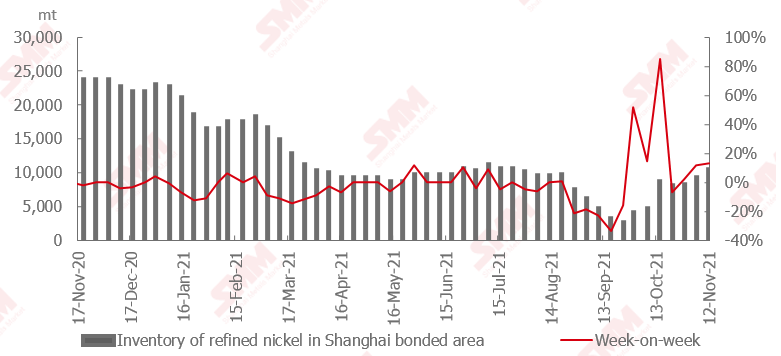

Pure Nickel Inventories in China Bonded Zone Continued to Increase

The SHFE/LME nickel price ratio did not give the opportunity to import this week. Therefore, the shipments arrivals of pure nickel directly went to the domestic bonded zone, and this is in line with SMM's expectations. The import window remains closed currently, so the inventory in the domestic bonded zone is expected to accumulate next week.

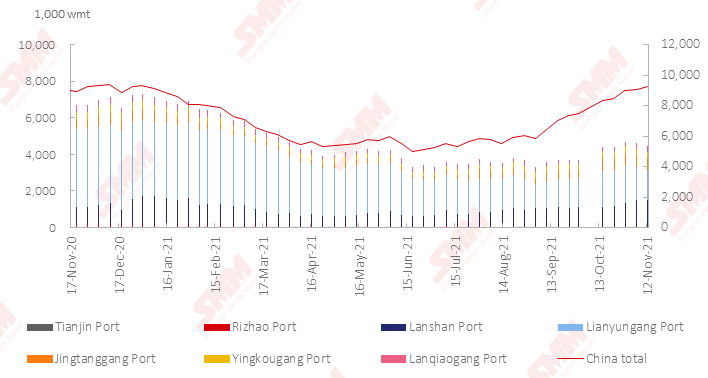

Nickel Ore Inventories at Chinese Ports Surged 190,000 wmt

The nickel ore inventory at Chinese ports grew 190,000 wmt from a week earlier to 9.24 million wmt as of November 12. Total Ni content stood at 72,500 mt. The total inventory at seven major ports stood at around 4.46 million wmt, a drop of 150,000 wmt from a week earlier.

The nickel ore inventory continued to increase.The demand for nickel ore was weaker than the normal levels as the NPI production in some regions has not fully recovered. But the import volume of nickel ore has declined sharply.

The shipments from the Philippines in October stood at around 4.6 million wmt, lower than in November. The NPI plants said that most of them restocked inventory only sufficient to production by the year-end. The port inventory is expected to decrease.