SHANGHAI, Sep 30 (SMM) - This is a roundup of China's metals weekly inventory as of September 30.

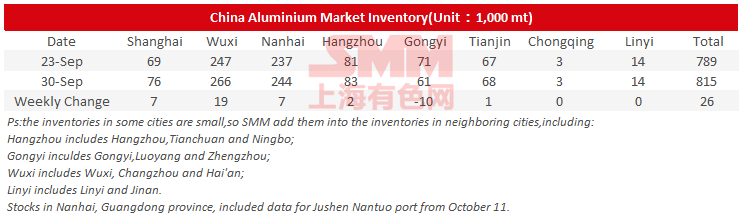

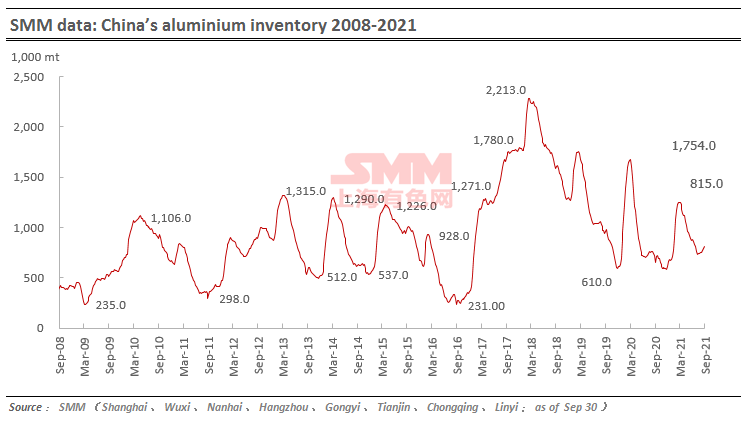

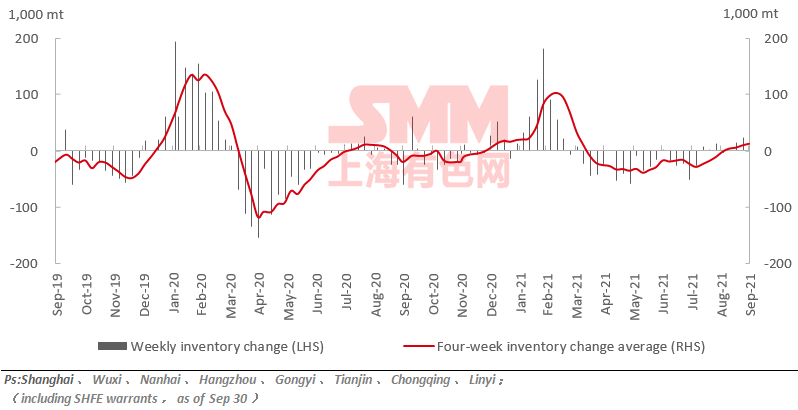

Aluminium Social Inventories Rose 26,000 mt on Week

SMM data showed that China's social inventories of aluminium across eight consumption areas rose 26,000 mt on the week to 815,000 mt as of September 30. The inventories in Wuxi and Nanhai rose slightly, while that in Gongyi dropped.

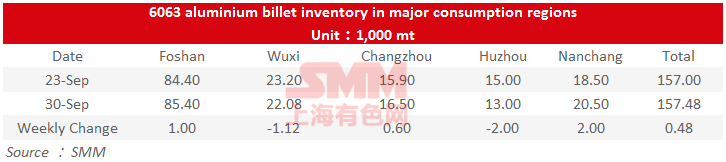

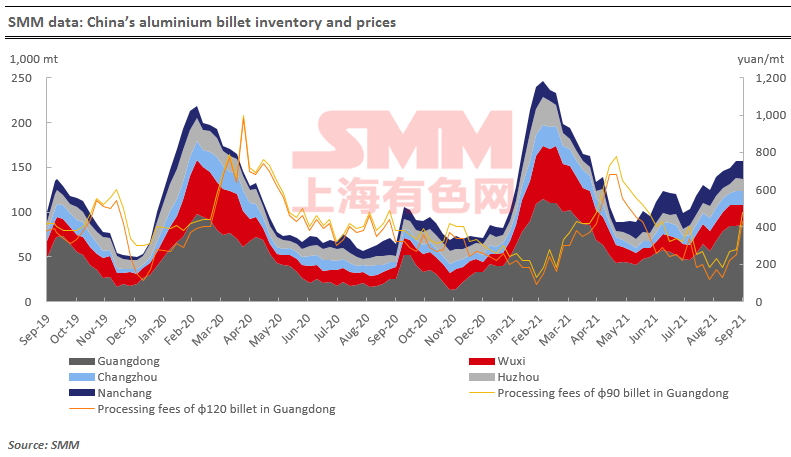

Post-holiday aluminium billet inventory is expected to increase amid sluggish pre-holiday restocking of extruders

The stocks of aluminium billet in five major consumption areas rose 500 mt to 157,500 mt on Thursday September 30 from the previous week, an increase of 0.32%. Among them, Nanchang contributed most of the increases by 2000 mt, up 10.81% from the last week. The inventories in Changzhou and Foshan added 600 mt (3.77%) and 1,000 mt (1.18%), respectively. While the inventories in Wuxi and Wuzhou dropped 1,100 mt (4.47%) and 2,000 mt (13.33%), respectively.

The downstream restocking was sluggish amid high aluminium prices and power rationing though it has been close to National Day holiday. Thus, the inventory of aluminium billets rose slightly.

Looking forward, the new orders were still less satisfactory as the demand of downstream extruders were sluggish, according to SMM. And some extruders have reduced their production due to power rationing and off-peak power consumption scheme in Guangdong and Jiangsu. The recovery after the holiday is worthy of attention. Meanwhile, the warehouses reported poor arrivals of goods, and the post-holiday inventory of aluminium billet may trend down amid purchase demand after the holiday. However, the demand side is likely to remain quiet as the power rationing intensified in Guangdong, which required local companies to close for 5 – 6 days or even 7 days in a week. So generally speaking, the inventory of aluminium billet next week will see higher possibility of increase.

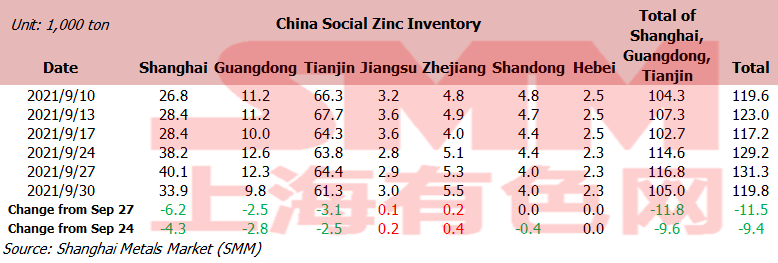

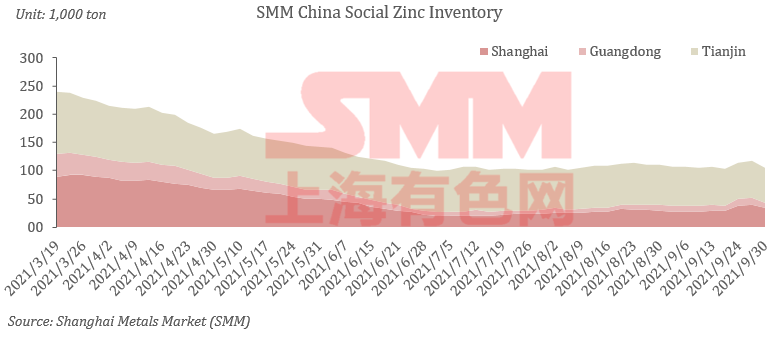

Zinc Social Inventories Down 9,400 mt on Week

SHANGHAI, Sep 30 (SMM)—Total zinc inventories across seven Chinese markets stood at 119,800 mt as of September 30, down 11,500 mt from September 27 and 9,400 mt from September 24.

The inventory in Shanghai declined sharply amid increasing pre-holiday restocking by downstream plants. Guangdong saw a decrease in stocks as maintenance at smelters affected the shipments and downstream producers still have pre-holiday restocking demand. The inventory in Tianjin trended lower due to limited arrivals of cargoes and pre-holiday stockpiling.

Inventories in Shanghai, Guangdong and Tianjin fell 9,600 mt, and inventories across seven Chinese markets decreased 9,400 mt.

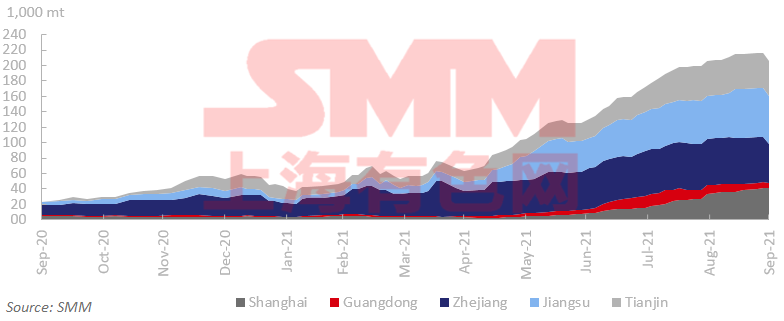

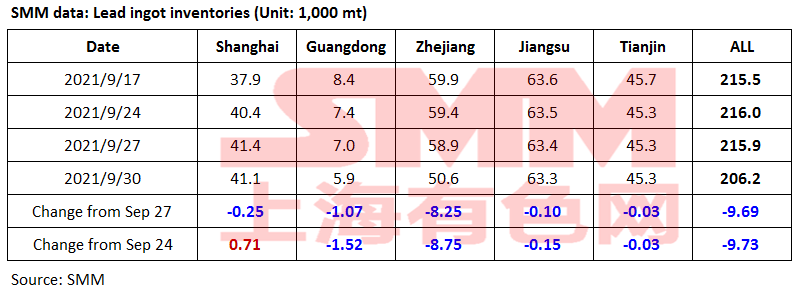

Lead Ingot Social Inventory Down 9,700 mt from Sep 24

Social inventories of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin decreased 9,700 mt from September 24 and fell 9,700 mt from September 27 to 206,200 mt as of September 30.

According to SMM survey, the primary and secondary lead smelters generally reduced production due to the losses or power rationing, and the tighter supply prompted the smelters to hold prices high. The quotations for the small orders of the primary lead stood at premiums of 0-200 yuan/mt (ex-factory) over the average SMM #1 lead price. The quotations for the secondary refined lead were mostly at discounts of 0-50 yuan/mt over SMM #1 lead price. The traders’ quotations for the domestic lead stood at discounts of 50-0 yuan/mt over the SHFE 2110 lead contract. The quotations in the trading market were generally lower than the smelters’ quotations, and downstream users turned to purchase from the traders, leading to a sharp decline in the social inventory, especially in Zhejiang, Guangdong, and other major consumption areas.

Compared with the smelters, more downstream companies will take the National Day holiday. There’s only one working day in the first week after the holiday, and the inventory may increase more in the plants. The stocks are likely to be transferred to the social warehouses for the delivery of the SHFE 2110 lead contract in the second week after the holiday.

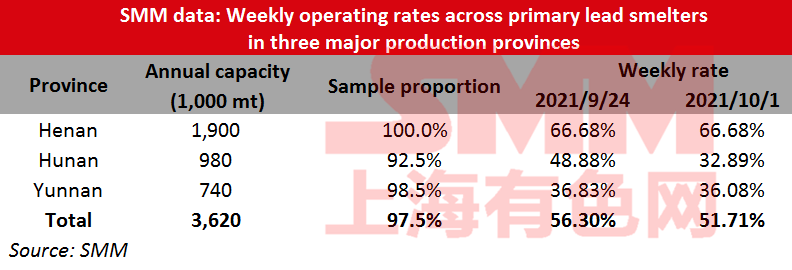

Operating Rate of Primary Lead Smelters Down 4.59% from Sep 24

The average operating rate across primary lead smelters in Henan, Hunan and Yunnan provinces lost 4.59 percentage points from the previous Friday to 51.71% in the week ended September 30, an SMM survey showed.

The smelters in Henan and Yunnan maintained normal production as they did not receive the notice of power rationing. The production restrictions expanded in Hunan. Yunteng and Yinxing slightly lowered their operating rates. Shuikoushan and Huaxin suspended production earlier for the autumn maintenance. The overall operating rate in Hunan fell significantly.

The lead concentrate supply remained tight in Yunnan. Hongqian, Gejiu Chuangyuan and other smelters are still in suspension.

In addition, Xing’an Silver and Lead have completed the maintenance in September. Its output will be partly resumed during the National Day holiday and fully recovered after the holiday. Jinde in Jiangxi plans to conduct maintenance in October.

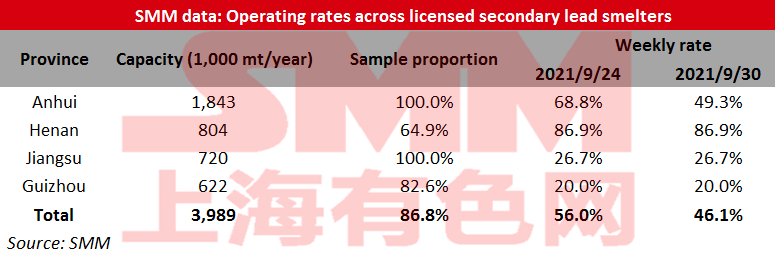

Operating Rate of Secondary Lead Smelters Down 9.91% from Sep 24

Operating rates across licensed smelters of secondary lead in Jiangsu, Anhui, Henan and Guizhou averaged 46.11% in the week ended September 30, down 9.91 percentage points from the previous week, showed an SMM survey.

The operating rate fell sharply mainly due to the further production reduction and suspension amid the losses, power rationing, and environmental protection. The extended power rationing and the inspections on the power consumption in some regions also affected the production of secondary lead.

Large-scale companies in Anhui started to reduce production by 15-30% this week, dragging down the overall operating rates.

The impact of the power rationing is expected to weaken after the National Day holiday, and some smelters in maintenance will resume production in Jiangxi and Henan. The overall operating rate is expected to rebound.

Nickel Ore Inventories at Chinese Ports Surged 143,000 wmt

Nickel ore inventory at Chinese ports grew 143,000 wmt from a week earlier to 7.49 million wmt as of September 30. Total Ni content stood at 58,800 mt. Total inventory at seven major ports stood at around 3.68 million wmt, a decline of 37,000 wmt from Friday September 24.

The impact of power rationing and production restriction has not yet fully subsided. And the suspension of production in Guangdong and Guangxi is still relatively severe. The stainless steel mills integrated with NPI facility and the neighbouring NPI plants that directly supply liquid NPI to mills were kept from resuming production.

Nickel ore inventories will maintain a slight accumulation in the short term.

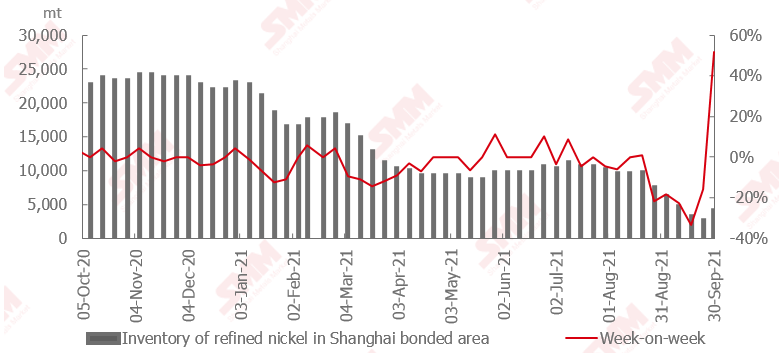

Chinese Bonded Zone Saw Concentrated Shipments Arrivals of Nickel Plates

Companies have cut output this week due to the impact of the domestic power rationing, leading to weak downstream stockpiling before the holidays.

The SHFE/LME nickel price ratio inched lower from highs early last week, but rallied amid low inventory and market concerns over further inventory declines amid low prices.

Attention shall be paid to the domestic consumption and production restrictions post holidays. If there is a recovery of production, the nickel price ratio is expected to continue to improve, which will stimulate the inflow of pure nickel.

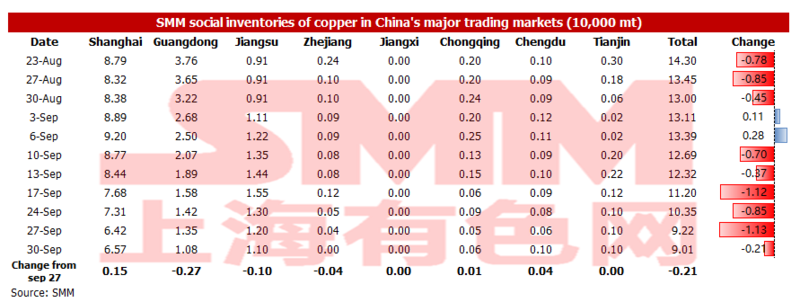

Copper Inventory in Major Chinese Markets Dipped 2,100 mt on Week

As of Thursday September 30, the copper inventory in the mainstream Chinese market dipped by 21,000 mt from Monday to 90,100 mt, continuing to set a new low for the year.

The main contributors of the inventory decline are Guangdong and Jiangsu, in which places the inventory fell 2,700 mt and 1,000 mt, respectively.

As the power rationing in Guangdong this week has weakened compared to last week, large downstream copper processing companies have generally resumed normal production. And the operating rate has risen significantly this week. In addition, some processing plants have refrained from halting production during the National Day holidays to catch up with the output, and restocked before the holiday. On the contrary, the inventory in Shanghai has increased by 1,500 mt.

Affected by the power rationing, many downstream companies that will close during the National Day holidays showed little buying interest ahead of the holiday. This combined with the inflow of imported copper has led to an increase in inventories. Some smelters will gradually recover after the overhaul post holiday. But output at many smelters will decline due to the power rationing and production restrictions. According to the experience of the past few years, the inventory will increase on the first day after the holidays.

SMM expects that the increase on the first day post-holiday will be less than the 23,000 mt in the same period of previous years.

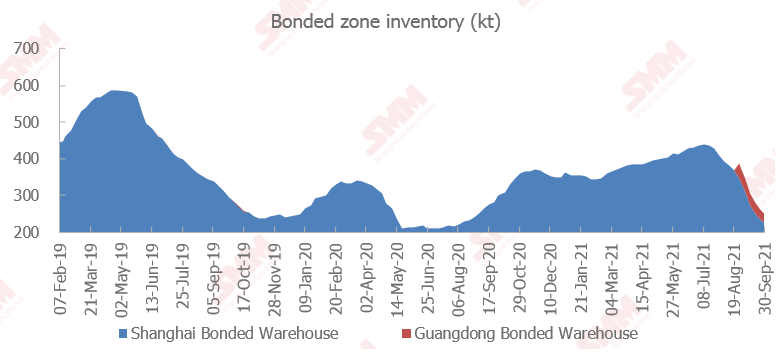

Copper Inventory in China Bonded Zone Dipped 11,200 mt on Week

Copper inventories in the domestic bonded zones dipped 11,200 mt from September 24 to 251,100 mt as of Friday September 30, according to the most recent SMM survey. Inventory in the Shanghai bonded zone decreased 9,700 mt to 225,600 mt, and inventory in the Guangdong bonded zone fell 1,500 mt to 25,500 mt.

In the past month, the import window has opened from time to time. This, combined with the high premiums in the domestic spot market, improved the import profit. This incentivised customs clearance, driving the bonded zone inventory to continue to fall.

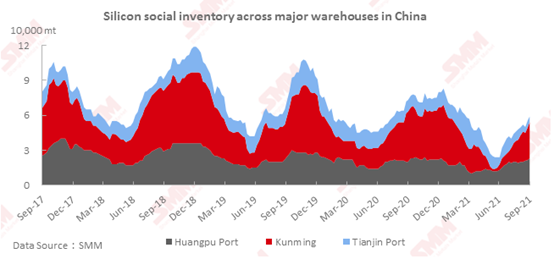

Social Inventory of Silicon Up 3,000 mt on Week

Social inventories of silicon in Huangpu port, Kunming, and Tianjin port totalled 59,000 mt as of September 30, up 3,000 mt from the previous week.

Pre-holiday transactions were muted amid high silicon prices and the power rationing at downstream producers. The inventory in Kunming and Huangpu Port increased. The stocks in Tianjin port fell slightly amid thin arrivals of cargoes and normal shipments. The social inventory is expected to stabilise as post-holiday market activities are likely to increase.

![[SMM Analysis] Magnesium Exports Surge in Early 2026, Geopolitical Turmoil Threatens Q2 Outlook](https://imgqn.smm.cn/usercenter/LYGyd20251217171725.jpg)

![Scrap Tungsten Market Saw a Slight Price Collapse, While Ore and Upstream Smelting Products Consolidated Sideways [SMM Tungsten Daily Review]](https://imgqn.smm.cn/usercenter/CIcRv20251217171725.jpg)