SHANGHAI, Sep 10 (SMM) - This is a roundup of China's metals weekly inventory as of September 10.

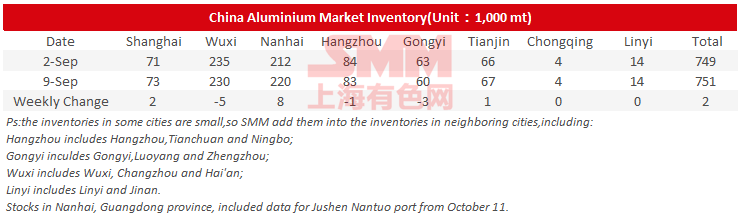

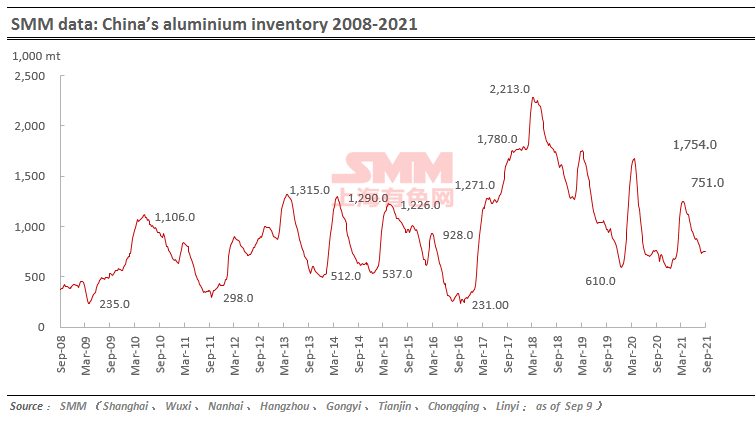

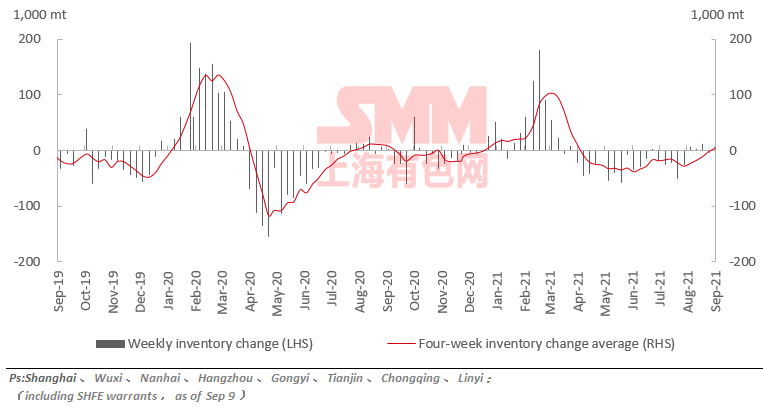

Aluminium Social Inventories Rose 2,000 mt on Week

SMM data showed that China's social inventories of aluminium across eight consumption areas rose 2,000 mt on the week to 751,000 mt as of September 9. Increases were mostly contributed by Nanhai due to added arrivals of imported aluminium and ingots from north-west China. Inventories in Wuxi and Gongyi continued to fall.

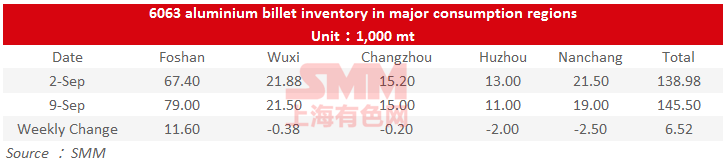

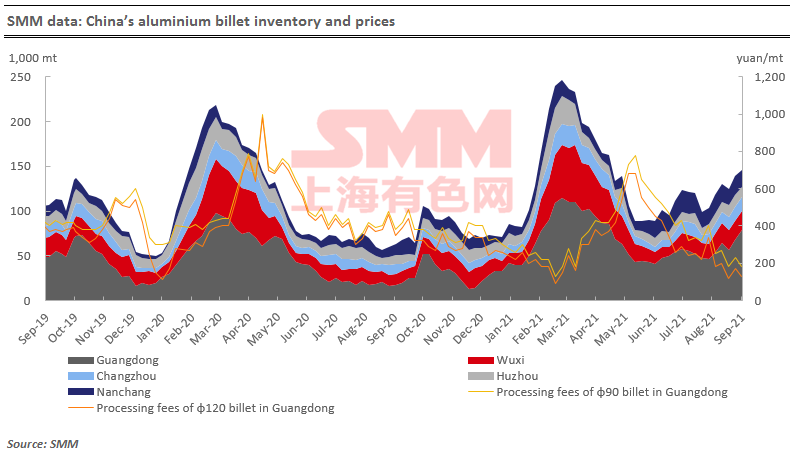

Aluminium Billet Inventories Up to 145,500 mt on Week

The stocks of aluminium billet in five major consumption areas rose by 6,500 mt to 145,500 mt on Thursday September 9 from the previous week, an increase of 4.7%.

The increase was solely contributed by Foshan, with an added amount of 11,600 mt or 17.2% on the week. Other fours markets all recorded decline in inventories. According to SMM, downstream sector was not interest in taking in goods on the back of soaring aluminium prices. Arrivals of aluminium billets in south China exceeded deliveries, and orders at downstream aluminium extrusion companies were also sluggish.

Going forward, the market is likely to be dominated by wait-and-see stance according to downstream aluminium extrusion companies in light of high prices. Some were even more cautious in taking orders, suppressing demand for aluminium billets due to shrinking orders at aluminium extrusion companies. Aluminium billets inventory is likely to rise further in the following week.

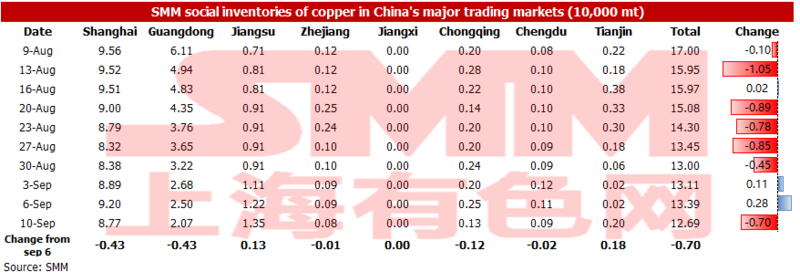

Copper Inventory in Major Chinese Markets Dipped 700 mt on Week

As of Monday September 10, copper inventory across major Chinese markets dipped 700 mt from Monday to 126,900 mt, according to SMM data.

Copper inventories in Shanghai decreased 4,300 mt from Monday to 8.7787,700 mt; copper inventories in Guangdong were down 4,300 mt from Monday to 20,700 mt; inventories fell slightly across Zhejiang, Chongqing and Chengdu. Copper stocks in Jiangsu and Tianjin increased by 1,300 mt and 1,800 mt, respectively, from Monday.

Domestic inventories rose slightly last week by 1,100 mt before returning to a downward track this week. The declines were mainly seen in Shanghai and Guangdong. Imports of copper in both places increased this week, but most of them were shipped directly to downstream plants, hardly contributing to inventories in social warehouses.

In addition, shipments arrivals in Guangdong were still low due to maintenance at smelters in neighbouring regions. We expect that inventory in Guangdong will not increase until after the National Day holiday. Inventory in Shanghai will depend on arrivals of imported copper.

Next week, we expect inventory decline to continue amid downstream stockpiling for Mid-Autumn Festival holidays.

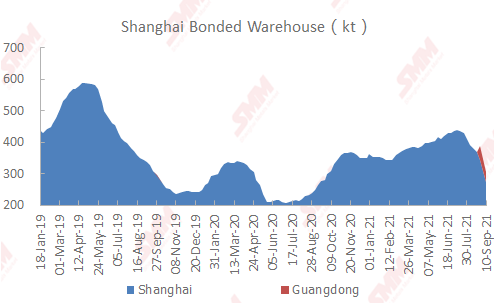

Copper Stocks in Bonded Area Decreased 42,400 mt on Week

Copper inventories in domestic bonded zones decreased 42,400 mt from September 3 to 305,300 mt on September 10, according to SMM survey.

Inventory in the Shanghai bonded zone decreased 37,900 mt to 272,800 mt, and inventory in the Guangdong bonded zone fell 4,500 mt to 32,500 mt.

In the past month, import profits have driven customs clearance by traders for large volumes of imported copper amid the favourable SHFE/LME copper price ratio. Therefore, bonded zone inventories have continued to decline rapidly.

Market participants have awaited delivery taking in queues in the Shanghai bonded zone. Bonded zone inventories will have room to fall.

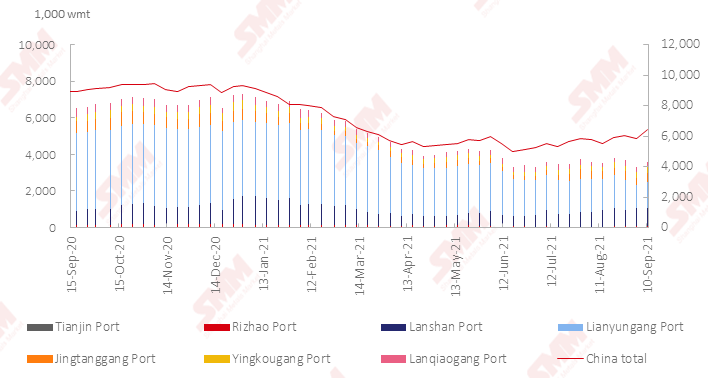

Nickel Ore Inventories at Chinese Ports Rose 586,000 wmt on Week

Nickel ore inventory at Chinese ports grew 586,000 wmt from a week earlier as of Friday September 10. Total inventory at seven major ports stood at 3.3 million wmt, an increase of 266,000 wmt from a week earlier. Total Ni content stood at 50,800 mt, an increase of 4,600 mt from last Friday.

Southern ports saw concentrated shipments arrivals this week. Offloading which was restricted previously due to the impact of the pandemic has recovered.

Two typhoons made landfall in the Philippines, which moved from the Philippines to the sea areas of south China. This is likely to affect the subsequent delivery and unloading process. The short-term accumulation of nickel ore inventory will be limited.

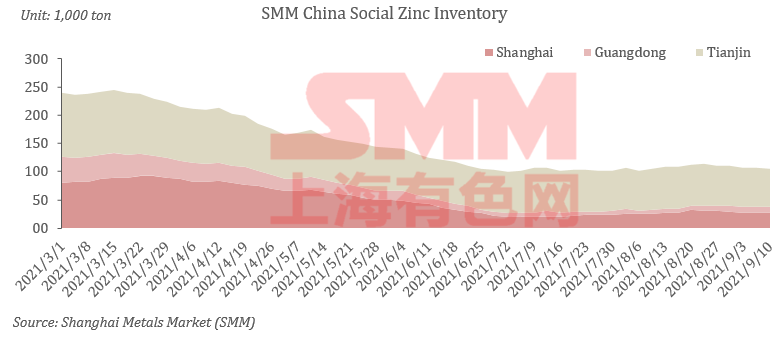

Zinc Inventory Fell 4,000 mt on Week

Total zinc inventories across seven Chinese markets stood at 119,600 mt as of September 10, down 2,500 mt from September 6 and 4,000 mt from September 3. Shanghai saw a balance between supply and demand as arrivals of cargoes increased and downstream plants properly restocked goods. Inventories in Guangdong increased further as higher zinc prices suppressed downstream demand and arrivals of goods stabilised in the spot market. Shipments from Tianjin rose sharply due to high discounts of spot quotes against east China market, less shipments by smelters and transfer of inventories to east China. Inventories in Shanghai, Guangdong and Tianjin fell 3100 mt, and inventories across seven Chinese markets decreased 4000 mt.

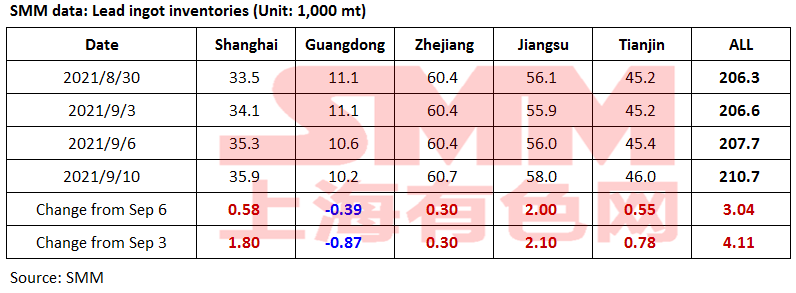

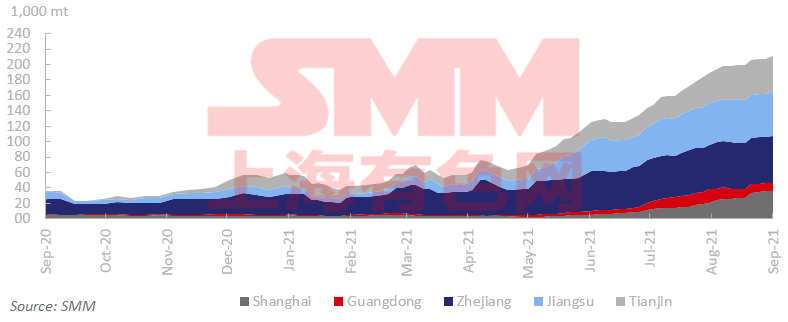

Social Inventories of Lead Ingots Up 4,100 mt on Week

Social inventories of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin increased 4,100 mt from September 3 and rose 3,000 mt from September 6 to 210,700 mt as of September 10.

Lead prices showed V-shaped trend and broke the breakeven point of secondary lead. Smelters generally lowered shipments while downstream producers held a cautious outlook. Some holders began to deliver goods and in-plant stocks of lead ingots transferred to social inventories. Secondary lead smelters in Guangdong suspended production amid environmental protection inspections and downstream plants turned to restock primary lead. Thus, stocks in Guangdong declined again. Lead ingot stocks are likely to continue to transfer to warehouses as next week is for delivery. Losses of secondary lead partly recovered as lead prices increased. Social inventories of lead ingots are expected to increase next week amid the commission of newly expanded smelters.

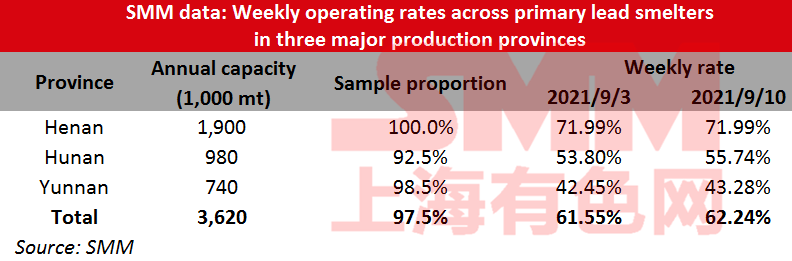

Operating Rates of Primary Lead Smelters Up 0.69% on Week

Operating rates across primary lead smelters in Henan, Hunan and Yunnan provinces gained 0.69 percentage point from the previous week to 62.24% in the week ended September 10, showed an SMM survey.

Production in Henan was largely unchanged. In Hunan, Shuikoushan Jinxin slightly increased production this week, restocking the finished products for the maintenance in October. Shuikoushan Zhihui also increased production in September after the power curtailment was lifted. In Yunnan, Mengzi Mining and Metallurgy is expected to resume production in mid-September, and the production is likely to be expanded next week. Gejiu Tongfu raised production after the raw material restocking. Chifeng Shanjin Silver and Lead slightly reduced in end-August due to the equipment failure, and is expected to resume normal production next week.

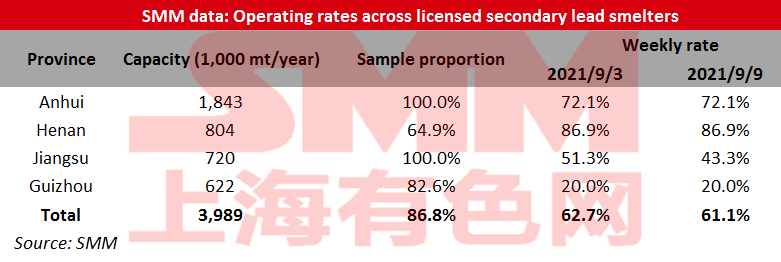

Operating Rates Across Licensed Smelters of Secondary Lead Down 1.62% on Week

Operating rates across licensed smelters of secondary lead in Jiangsu, Anhui, Henan and Guizhou stood at 61.11% this week, down 1.62% from the previous week, an SMM survey showed.

The secondary smelters tightened their production plans as most of them continued to suffer losses and demand failed to increase sharply. Output at some small smelters declined amid market fluctuations. Although most companies were at a loss this week, costs across companies varied. The losses at individual small smelters in Jiangxi and Henan were eased, which resumed production from maintenance this week. But this part of increment failed to change the trend of declining production across four markets. Operating rates at secondary smelters are expected to increase amid the end of maintenance at individual smelters in Anhui and Guangdong.

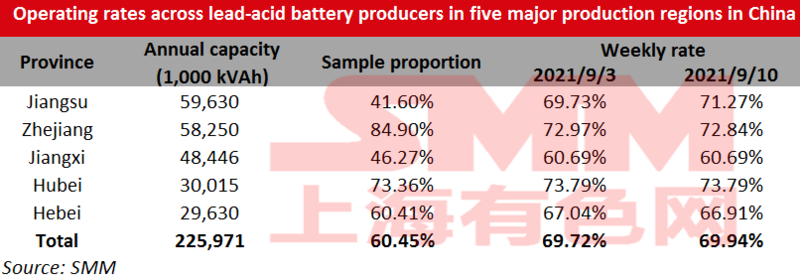

Operating Rates of Lead-Acid Battery Plants Up 0.22% on Week

Operating rates across lead-acid battery producers in Jiangsu, Zhejiang, Jiangxi, Hubei and Hebei provinces increased 0.22 percentage point from September 3 to 69.94% as of Friday September 10.

The pandemic in Jiangsu has been effectively controlled in September, and some lead-acid battery producers have resumed production amid loosened pandemic prevention policy, leading to the increase in the overall operating rate.

The car production and sales weakened in other regions, dragging down the orders for car batteries. At the same time, some car battery companies received few orders due to the impeded export shipping, and the companies plan to reduce production in September.