SHANGHAI, Aug 27 (SMM) - This is a roundup of China's metals weekly inventory as of September 3.

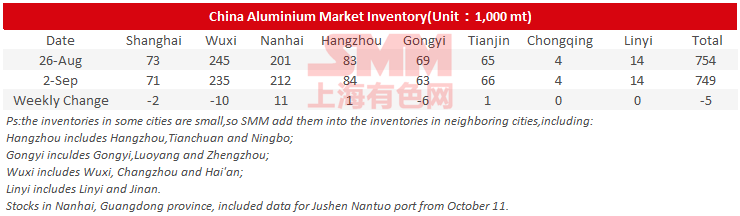

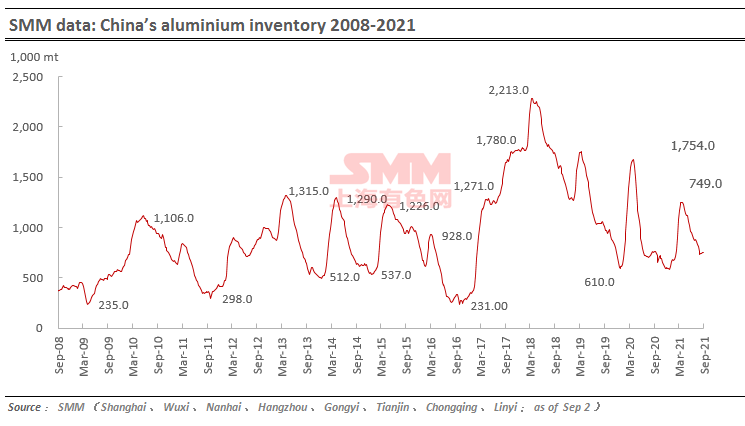

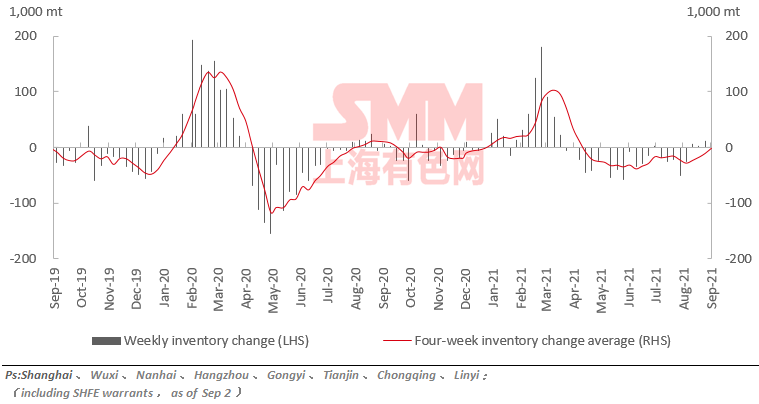

Aluminum Ingot Social Inventory Declined 5,000 mt in the Week Ended September 2

Aluminum ingot social inventory across the eight major consumption regions in China fell by 5,000 mt from a week ago to 749,000 mt on September 2. Shanghai, Wuxi and Gongyi contributed most of the decline. Inventory in Nanhai rose slightly due to poor demand. Market shall continue to pay attention to downstream consumption and arrivals in consumption hubs.

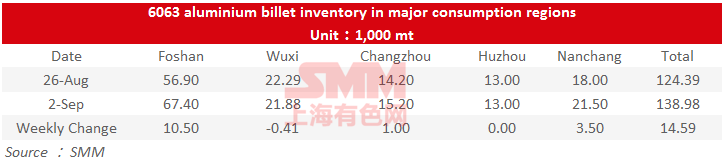

Aluminium Billet Inventory Increased by 14,600 mt in the Week Ended September 2

Domestic aluminium billet inventory stood at 139,000 mt on September 2, an increase of 14,600 nt or 11.7% from a week ago. Wuxi was the only region that saw lower inventory. Inventory in Foshan led the increase among the five regions, growing by 10,500 mt or 18.45%. Large arrivals and weaker purchases resulted in inventory accumulation. Downstream aluminium extrusion companies reduced purchases due to poor orders and high aluminium prices, which hit a 13-year high. Aluminium extrusion companies report poor orders, especially for construction extrusion. Inventory will probably rise further next week.

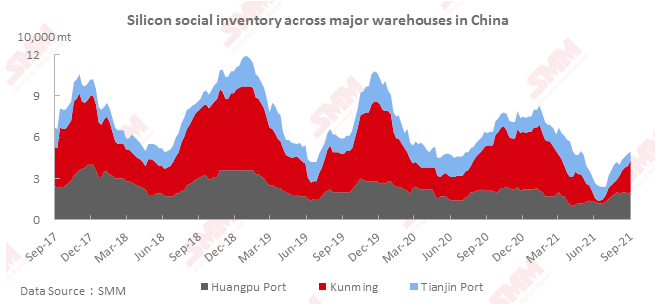

Social Inventory of Silicon Metal Diverged by Region

Social inventories of silicon metal in the three major regions totalled 50,000 mt on September 3, an increase of 2,000 mt from a week ago. Inventory at Tianjin port fell due to fewer arrivals. Inventory in south China continued to grow in the rainy season, with inventory in Kunming climbing at a faster pace. Social inventories are likely to grow further next week as a producer in the north has gradually resumed shipments.

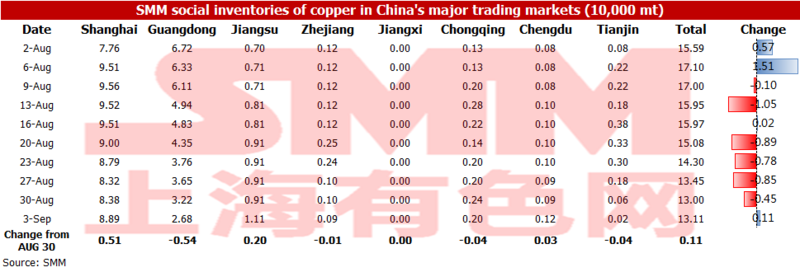

Copper Inventories across Major Chinese Markets Added 1,100 mt

Total copper inventories across major markets in China grew 1,100 mt from Monday to 131,100 mt as of Friday September 3, according to SMM data.

Copper inventories in Shanghai increased 5,100 mt from Monday to 88,900 mt; copper inventories in Guangdong decreased 5,400 mt to 26,800 mt; copper inventories in Jiangsu were up 2,000 mt to 11,100 mt; copper inventories in Tianjin dipped 400 mt to 200 mt.

SMM understood that imported copper arrived this week. Some traders transported cargoes directly to copper semis producers, so delivery taking by downstream buyers decreased. And inventories in east China increased noticeably.

Inventories in Guangdong continued to fall due to low shipments arrivals of domestic cargoes.

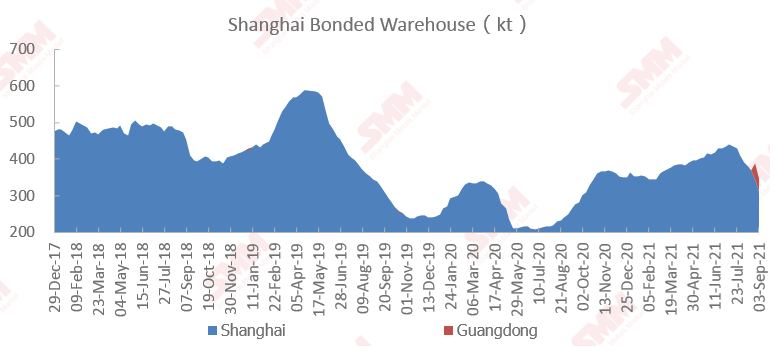

Copper Stocks in Bonded Area Decreased 40,400 mt

Copper inventories in domestic bonded zone decreased 40,400 mt from August 27 to 347,700 mt on September 3, according to SMM survey.

The import window opened previously and cargoes under warrants signed amid import profits entered after customs clearances this week, driving further declines in bonded zone inventory.

Inventory in the Shanghai bonded zone decreased 34,400 mt to 310,700 mt, and inventory in the Guangdong bonded zone fell 6,000 mt to 37,000 mt.

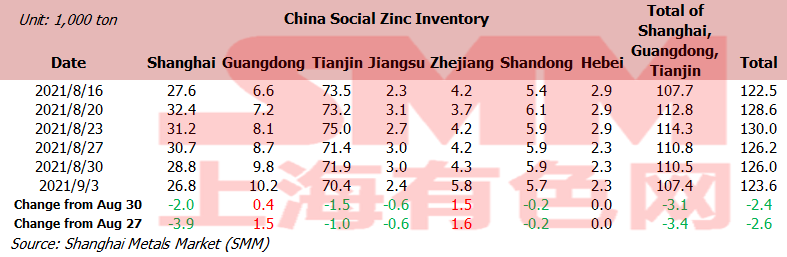

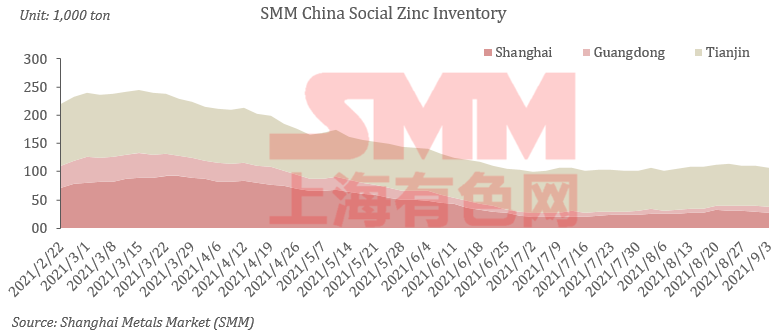

Zinc Social Inventories Down 2600 mt on Week

SHANGHAI, Sep 3 (SMM)—Total zinc inventories across seven Chinese markets stood at 123,600 mt as of September 3, down 2,400 mt from August 30 and 2,600 mt from August 27.

Inventories in Shanghai fell sharply as imported zinc inflow thinned, market mainly consumed domestic zinc and downstream plants restocked cargoes on declining prices. Guangdong saw an increase in stocks as arrivals of cargoes in the market increased and downstream demand was muted. Stocks in Tianjin declined amid the consumption of the second batch of government stockpiles and restocking demand.

Inventories in Shanghai, Guangdong and Tianjin fell 3400 mt, and inventories across seven Chinese markets decreased 2600 mt.

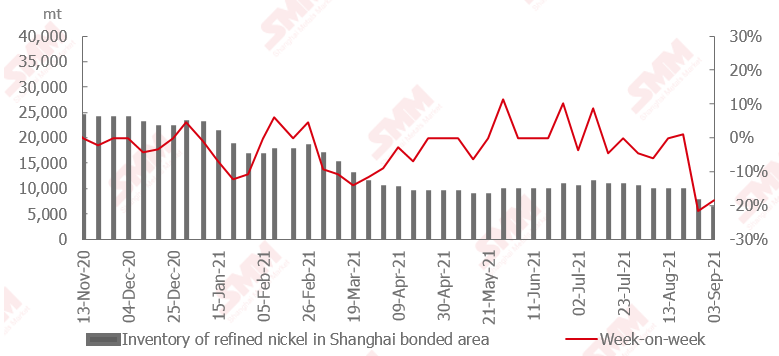

Nickel Inventory in Bonded Zone Declined amid Wider Import Profits

Pure nickel inventory in the bonded zone declined over 1,400 mt this week, according to SMM data.

Tight domestic spot supply pushed the SHFE/LME nickel price ratio higher this week. Higher import profits incentivised traders to accelerate delivery taking from bonded zone inventories. The contango structure on LME nickel has turned into a backwardation structure recently and quotes for nickel plate under B/L continued to rise. The highest traded import premiums reached $350/mt. Supply of cargoes under B/L has been tight.

More cargoes are expected to enter the domestic market from the bonded zone next week given the current SHFE/LME nickel price ratio. This will drive further declines in bonded zone inventory.

Nickel Ore Inventories at Chinese Ports fell 199,000 wmt

As of September 3, nickel ore inventory at Chinese ports fell 199,000 wmt from a week earlier to 5.88 million wmt. Total Ni content stood at 46,200 wmt, according to SMM data. Total inventory at seven major ports stood at around 3.3 million wmt, a decline of 379,000 wmt from a week earlier.

Affected by the pandemic, cargoes were stranded at ports for a longer period. And this slowed growth in port inventory. The current port inventory level remains low, which is basically the same as that of March.

Domestic demand remains strong. Output did not slide. Nickel ore inventory is expected to decrease further in October.

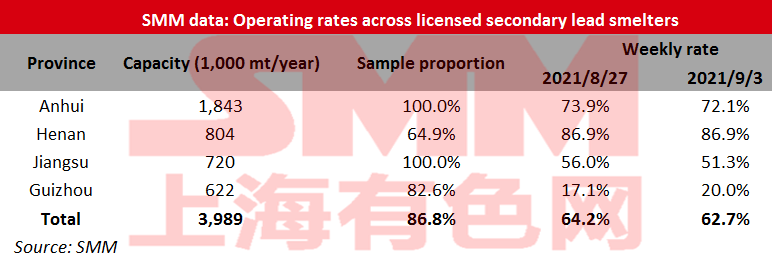

Operating Rates of Secondary Lead Smelters Down 1.45% on Week

Operating rates across licensed smelters of secondary lead in Jiangsu, Anhui, Henan and Guizhou averaged 62.72% in the week ended September 3, down 1.45 percentage points from the previous week, showed an SMM survey.

Operating rates of secondary lead smelters continued to decline mainly because the losses of secondary refined lead smelters expanded, and some smelters had losses aournd 300-500 yuan/mt. Some smelters in Anhui cut production sharply due to environmental protection control and losses. The output of large smelters in Jiangsu also fell slightly due to market fluctuations. Anhui Xinda resumed production from maintenance, and Guizhou Cenxiang increased production as planned, but the output increment was limited, and the overall operating rate declined.

Among the non-sample companies, Jiujiang Huijin, zhenyu and other small smelters in Jiangxi reduced or suspended production after secondary lead prices fell below the break-even point. smelters in Hubei increased production reduction or suspension. Some smelters in Hebei also reduced production due to the factory relocation. Anhui Huabo Phase I will be put into production in mid-September.

The operating rate may increase slightly this week if profits recover and the emission restrictions loosen.

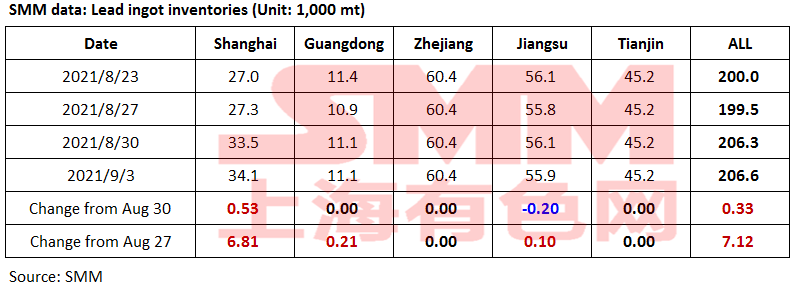

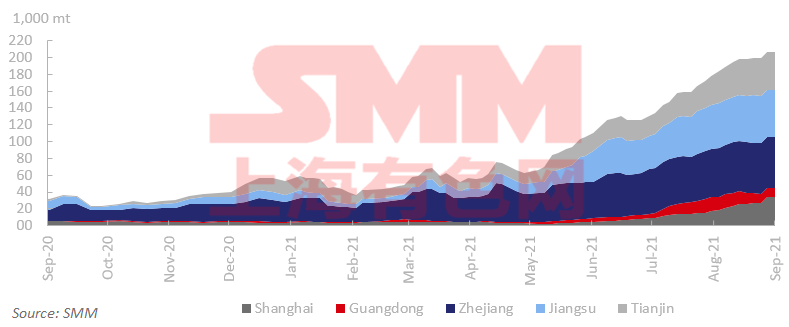

Lead Ingot Social Inventories Expanded 7,100 mt On Week

SHANGHAI, Sep 3 (SMM) – Social inventories of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin increased 7,100 mt from August 27 and rose 300 mt from August 30 to 206,600 mt as of September 3.

Lead prices fell below 15,000 yuan/mt, secondary lead declined below the cost line and losses at smelters increased. Primary and secondary lead smelters held a wait-and-see outlook. Shipments at traders were normal. Secondary lead smelters reduced output in the second half of the week. Thus, social inventories of lead ingots rose sharply on the week, but the increment slowed from early week. Cargoes at some smelters will be transferred to warehouses in approaching the deliveries. Secondary lead smelters still suffer losses at the moment and some smelters reduced their output. The increase for social inventories of lead ingots is expected to slow.

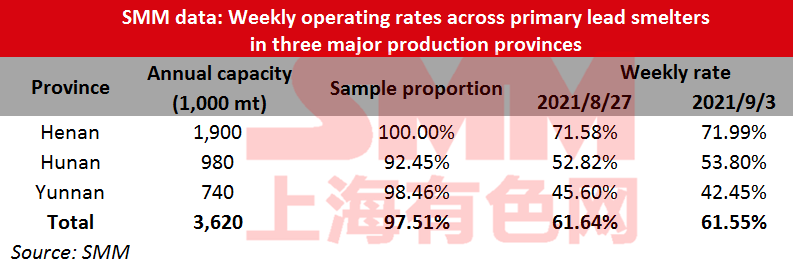

Operating Rates of Primary Lead Smelters Down 0.08% on Week

Operating rates across primary lead smelters in Henan, Hunan and Yunnan provinces dipped 0.08 percentage point from the previous week to 61.55% in the week ended September 3, showed an SMM survey.

Henan Shibin plans to slightly increase production in September to make up for the reduced output in the power curtailment. Shuikoushan Jinxin slightly raised production as planned. A smelter in Gejiu, Yunnan suspended production due to the tight supply of crude lead. Xing'an Silver and Lead in Inner Mongolia started maintenance and basically had no output this week.

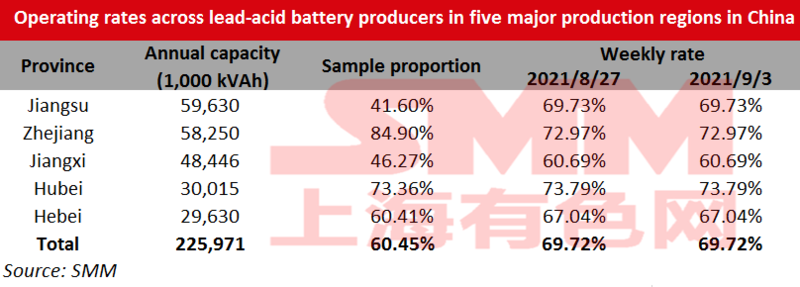

Operating Rates of Lead-Acid Battery Plants Flat on Week

Operating rates across lead-acid battery producers in Jiangsu, Zhejiang, Jiangxi, Hubei and Hebei provinces stood largely flat at 69.72% on the week as of Friday September 3.

Lead-acid battery market was largely unchanged, but some dealers tended to be cautious in purchasing due to the lower lead prices. The replacement demand in the car battery market was weak, and some battery plants had the product inventories of two months.

Although the export orders of car batteries increased, the shipping cycle was longer due to the adverse shipping conditions, and corporate funds were stagnant. Most companies scheduled production on the sales, and the production did not improve significantly.

The orders for electric bicycle battery were relatively more abundant in some companies in Jiangxi and Jiangsu, where the operating rates stood above 90%. However, some lead-acid battery companies in the key areas in Jiangsu were still under strict production restrictions due to the pandemic.

Most battery companies will continue to schedule production based on sales in September, and the operating rate will be stable.