Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

Language:

Language:

SMM6 March 23: in today's online market live conference hosted by SMM, SMM analyst Yu Shaoxue conducted a live broadcast of the development status and future prospects of lithium copper foil in China. In the live broadcast, the analyst introduced the development status of lithium copper foil industry, from the point of view of lithium industry and combined with the survey data of lithium copper foil enterprises, and then introduced the development trend of lithium battery in the downstream application field. finally, according to the downstream demand, the supply and demand of lithium copper foil in the future is predicted.

Analysis on the present situation of Lithium Copper foil Industry in China

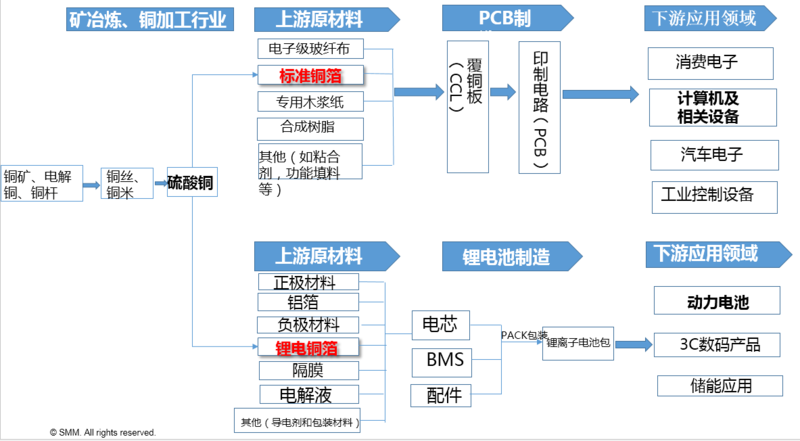

The lithium copper foil is located in the upstream of the lithium ion battery industry chain. As a negative collector, it forms the cell of the lithium ion battery together with positive electrode materials, negative electrode materials, diaphragms, electrolytes and other materials (such as conductive agents, packaging materials, etc.). The battery core, BMS (that is, our battery management system) and accessories are packaged by Pack (battery package) to form a complete lithium ion battery package. It is used in downstream fields such as new energy vehicles.

Standard copper foil is the upstream material for making copper clad laminate and printed circuit board, and its main function is to act as a wire for the interconnection of electronic components. Used in consumer electronics, computers and related equipment.

In 2020, the output of lithium electricity in China is about 150000 tons, accounting for 31% of the total output of electronic copper foil. China's output of lithium copper foil increased by more than 100000 tons from 50, 000 tons in 2015 to 153000 tons in 2020, with a compound annual growth rate of 25.06 percent. From the perspective of product structure, the proportion of standard foil is still as high as 69%, showing a downward trend year by year, while the proportion of lithium copper foil is increasing year by year.

Among the major domestic lithium battery copper foil manufacturers in 2020, the annual output of lithium battery copper foil in 2020 is more than 2000 tons, with a growth rate of more than 2 digits. Longdian Huaxin, Nuode shares, Guangdong Jiayuan three enterprises total output of lithium copper foil is about 77000 tons, accounting for about 50% of the total domestic output.

Since the introduction of 6 μ m copper foil in the Ningde era in 2018, the proportion of 6 μ m has continued to rise, from about 14% in 2017 to 45% in 2021, and has become the mainstream specification in the industry. 4.5 mu m has been available for mass use since last year, with an average monthly consumption of more than 300 tons in the industry. Jiayuan Technology, Nord shares, Copper Crown Copper foil and other enterprises have achieved mass production of 4.5 μ m copper foil. According to SMM, Jiayuan 4.5 micron annual production of about 2000 tons, Nord has more than 1000 tons, including downstream Ningde era, BYD and other companies are now starting to use 4.5 micron products in bulk.

The finished product price of copper foil is mainly composed of copper price + processing fee. the price of copper wire purchased by copper foil enterprises is generally in accordance with the model of average price + processing fee of electrolytic copper in SMM No.1, while the price of selling copper foil is mainly in accordance with the monthly average price + processing fee of last month's spot. The decisive factor of the enterprise's operating margin is the processing fee difference between the enterprise and the supplier, that is, "sales processing fee-supplier processing fee". In essence, the change of copper price has little influence on the enterprise's operating margin, so it has little influence on the net profit of copper foil enterprises. Based on this background, the profitability of the processing fee level of the company's overall products is the core key variable.

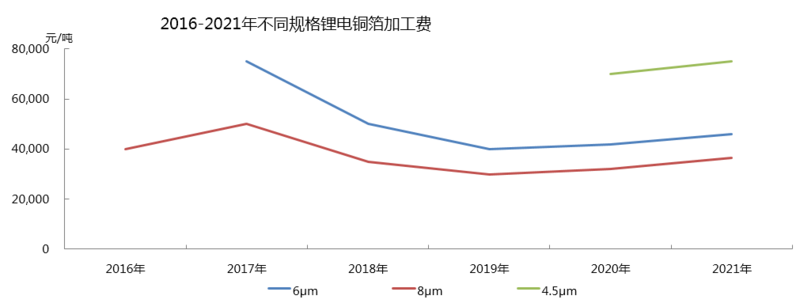

First of all, lithium copper foil, as the carrier and conductor of the anode material of lithium battery, was promoted by the first round of rapid development of new energy vehicles around the world from 2016 to 2017, and the processing fee began to rise. By 2017, the average processing fee of 8um lithium copper foil reached 50,000 yuan / ton, but with the slowdown of the downstream growth rate of lithium battery and the expansion of lithium copper foil production capacity in 2019, the processing fee of 8 μ m lithium copper foil fell again to the level of 30,000 yuan / ton. Since the second half of 2020, the growth of downstream demand has led to the shortage of lithium copper foil, and the processing cost of copper foil has rebounded significantly. Up to now, the processing fee of 8 μ m copper foil is about 36000 yuan / ton, the additional fee of 6 μ m copper foil is 46000 yuan / ton, and the processing fee of 4.5 μ m copper foil is about 75000 yuan / ton.

Development status of downstream Lithium electricity Industry

The road to the rapid development of new energy vehicles

2020 there are more than 80 million vehicles sold in the world, while there are only more than 3 million new energy vehicles in the world, and about 1.22 million in China. It is estimated that the output of new energy vehicles will be 6.1 million by 2025. From a further point, it is conservatively estimated that the sales in 2030 will reach 13.6 million. Read that the proportion of electrification in other countries is growing rapidly. In fact, it is very difficult to predict this emerging industry. Once the critical point is reached, it will grow at a base rate.

The installed capacity of carbon peak and carbon neutralization will exceed 30GW at the end of the 14th five-year Plan.

By the end of 2020, the cumulative installed scale of electrochemical energy storage in China ranked second, with 3.2GW, an increase of 83.3% over the same period last year. Among all kinds of electrochemical energy storage technologies, the largest cumulative installed scale of lithium-ion batteries is 3GW. The state has issued the guidance on accelerating the Development of New Energy Storage (draft for soliciting opinions), and it is planned that the installed scale of energy storage will reach 30GW by 2025. If the lithium battery is equipped with energy storage according to 2 hours, it takes 60 gigawatts of battery. Suppose 900t copper foil is used for optical energy storage. In addition to electric energy storage, there are household energy storage, communication base stations, USB backup power and so on. It is estimated that by 2025, Chinese market shipments will reach 60 GWH, with a five-year compound growth rate of more than 33%. The rapid growth of lithium-ion battery shipments for energy storage is mainly due to the rapid decline in the cost of lithium-ion batteries driven by the large-scale production of power batteries for new energy vehicles.

China Battery Market-Global announced Investment Plan

In 2020, the installed capacity of lithium-ion batteries for new energy vehicles in China totaled 63.3 GWH, an increase of 1.8% over the same period last year. From the overall performance, affected by the epidemic, the monthly installed capacity of power batteries has been in negative growth in the first half of the year, until the rapid growth can be resumed in the second half of the year. From the point of view of the installed capacity, Ningde era is the largest, head power battery system provider, BYD's battery supply is mainly, so in terms of expansion scale, it is weaker than Ningde era. According to the future planned new capacity of several major companies this year, SMM estimates that the demand for lithium-ion batteries is about 390 gigawatts for power batteries, 150 gigawatts for 3C batteries, and 60 gigawatts for energy storage.

Analysis on the Development trend of Lithium Copper foil Industry

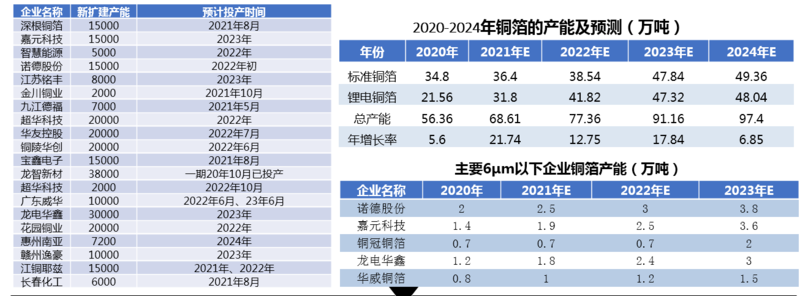

In 2022, the total annual production capacity of the newly built copper foil factory (or production line) in China is estimated to reach about 100000 tons. Among them, 85% is the new production capacity of copper foil for lithium battery.

It is estimated that from 21 to 23 years, the production capacity of electrolytic copper foil in China will continuously increase at a double-digit annual growth rate, among which in 2022, the production capacity of copper foil for electronic circuits and copper foil for lithium battery will be reversed in the first year above, that is, the production capacity of copper foil for lithium battery is higher than that for electronic circuits.

At present, the excess capacity is mainly concentrated in 6 μ m and above lithium copper foil, but the demand side is in the transition to 6 μ m and below. The reduction of market orders for lithium copper foil above 6 μ m has triggered fierce market competition, and it is difficult for some enterprises to effectively release new production capacity. (3) the switching from 8 μ m to 6 μ m of lithium copper foil has a technical threshold and needs to go through a long period of time. It is expected that the production capacity utilization rate of manufacturers with extremely thin lithium copper foil at the head will be high. Due to technical reasons, it is difficult for small manufacturers to meet the production requirements of extremely thin lithium copper foil, but the demand space above 8 μ m will be further reduced. In this case, it is expected that the overall capacity utilization rate of lithium copper foil manufacturers will remain low, while the head manufacturers will run at full production.

At present, the copper foil of lithium-ion battery is mainly 8 μ m and 6 μ m, and the future development trend is to develop products with thinner and higher energy density. 70 KG/Kwh is calculated by decreasing. However, taking into account the climbing of the overall new capacity of lithium copper foil and the overall industry utilization rate of about 65%, as well as the factor of quality rate, the relationship between supply and demand of global lithium copper foil will be relatively healthy, according to the law of market economy, the future expansion plan of lithium copper foil production capacity will still be based on the overall market demand. However, in the short term, the production capacity of high-end lithium copper foil of 6 μ m or less is relatively scarce.

SMM estimates that the demand for lithium copper foil will reach 540900 tons by 2025. In 20, 21 and 23 years, the nominal production capacity was higher than the demand for lithium copper foil in these three years, and there was excess capacity in all three years. It is expected that the overcapacity rate will begin to narrow from 2023, and the whole market will tend to be in a tight balance by 25 years.

From the point of view of the relationship between supply and demand of lithium copper foil and electronic circuit copper foil, due to the influence of the epidemic situation, the supply and demand mismatch in 2020, copper foil processing fees into the rising channel, in the short term, due to the untimely realization of production capacity and difficulties in converting the production capacity of very thin copper foil below 6 μ m, copper foil processing fees still maintain an upward trend.

On the whole, the nominal capacity of domestic copper foil is in a state of excess, and with the commissioning of new capacity and the improvement of capacity utilization, processing fees are expected to be adjusted in the future. it is estimated that by 25 years, the processing fee for 6 microns is 40,000 / ton, and that for 8 microns is 30,000 / ton.

For queries, please contact Lemon Zhao at lemonzhao@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn