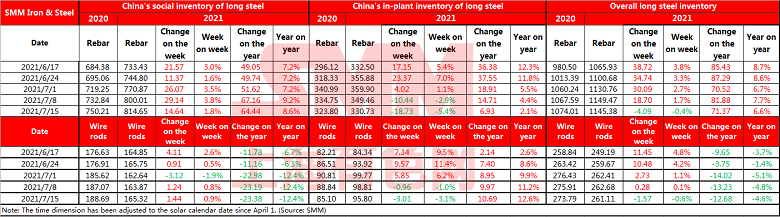

SHANGHAI, Jul 16 (SMM) — Inventories of rebar across Chinese steelmakers and social warehouses stood at 11.45 million mt as of July 15, down 0.4% from a week ago. Stocks are up 6.6% from a year earlier. The continuous growth of steel production has been initially curbed.

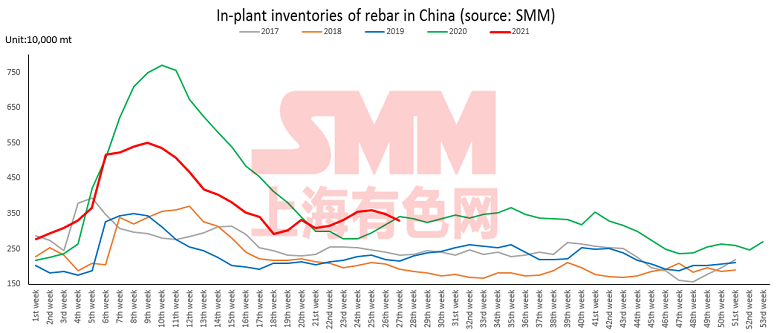

With the production restriction news brewing, prices of rebar spots and contracts resonated upwards, the market spots, contracts and speculative demand actively entered the market, and in-plant inventories were transferred smoothly.

Inventories at Chinese steelmakers fell 187,300 mt on the week and stood at 3.31 million mt. Stocks are down 5.4% from a week ago and up 2.1% from a year earlier.

The heavy rains and flood season in the south suppressed the release of end-user demand in mid-July. The performance of real estate data in June was poor. Construction area, new housing starts and land purchases were all significantly weaker from the previous month. Only the completed area showed a positive growth trend, indicating that the current demand for real estate stock was weakening and the demand potential expectations were not optimistic.

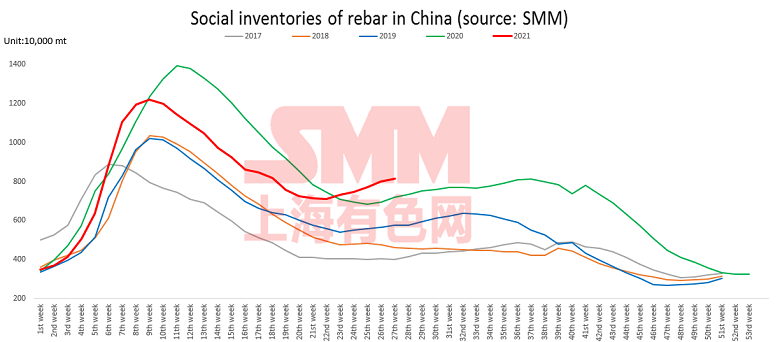

Inventories at social warehouses rose 146,400 mt on the week and stood at 8.15 million mt, up 1.8% from a week ago and 8.6% higher from a year ago.

Total inventories of long steel began to decrease, and the decline in in-plant stocks continued to expand. Social inventories continued to post slighter increase. It can be seen that amid the decrease in output and the release of speculative demand, the current active decline of in-plant stocks has been faster than the passive accumulation of social stocks.

The steel market is still in the strong expectation logic of restricting production at present, and the scope of influence is still expanding. The spot and contract market has a strong hype atmosphere around the restriction of production. There is no doubt about the supply reduction in the second half of the year, but the current risk point is the resurgence of production after the profit recovery of steel enterprises and the implementation of production restrictions without the constraints of red head documents.

On the demand side, the current demand for real estate stock is released ahead of schedule, and demand resilience will decline to a certain extent. With weak supply and demand fundamentals, the supply-side contraction will become the main driving force for the upward trend of steel prices, and the risks of policy regulation need to be guarded against.