SHANGHAI, May 28 (SMM) — The national high-level meeting kept vocalizing this week, and administrative intervention frequently reflected the determination of the policy to face the suppression of commodity prices. However, there is also rare good news among the many bad news: "Li Keqiang presided over the National Standing Committee on May 26. During the meeting, it was proposed to further promote anti-monopoly and anti-unfair competition law enforcement, and investigate and deal with malicious subsidies and low-price dumping for market share according to law." This news seems to have nothing to do with the steel market, but the China Iron and Steel Association issued a self-discipline proposal for the steel industry that it is proposed to oppose the behavior of driving up prices higher than costs, and dumping of prices below cost.

The futures market stopped falling and rebounded yesterday, and the spot market finally ushered in a short-term stabilization. If administrative intervention comes to an end, will the market usher in a turning point for bargaining?

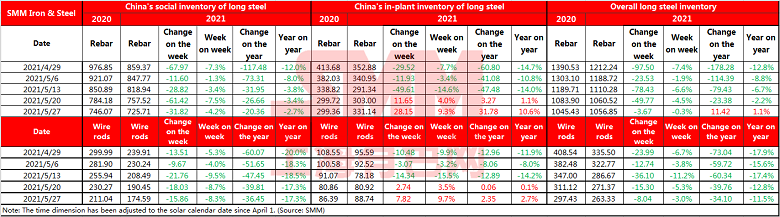

China steel rebar inventory posted slower decrease this week, and the turning point was gradually approaching. Inventories of rebar across Chinese steelmakers and social warehouses stood at 10.57 million mt as of May 27, down 0.3% from a week ago. Stocks are down 1.1% from a year earlier.

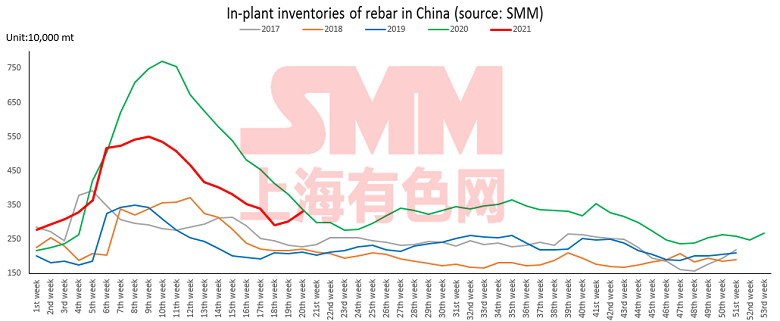

Due to the wide decline in prices, steel companies' sales were blocked, and in-plant stocks posted faster increase for the second consecutive week, and the year-on-year growth rate further expanded. Inventories at Chinese steelmakers rose 281,500 mt on the week and stood at 3.31 million mt. Stocks are up 9.3% from a week ago and up 10.6% from a year earlier.

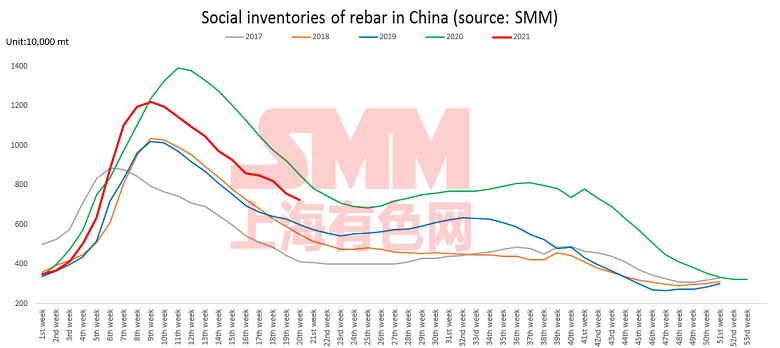

Due to the rapid price decline, spot traders were unable to ship goods in time, and speculators sold at low prices, which intensified the selling pressure on the spot market. Although the pace of end-user purchases has recovered, there is little speculative demand, and with the advent of the hot and rainy seasonal off-season, the daily transaction data has been less than 180,000 mt for several days. Inventories at social warehouses fell 318,200 mt on the week and stood at 7.26 million mt, down 4.2% from a week ago and 2.7% lower from a year ago. The year-on-year decrease fell 0.7 percentage point from the previous week. Considering that the current in-plant stocks are rising too fast, it is expected that the pressure on the increase of social stocks will gradually increase.

Judging from the spirit of the recent high-level meetings and the speeches made by the leaders, in order to ensure the development of downstream processing and manufacturing, the policy focus on upstream raw materials will still focus on "stabilizing prices" and ensuring supply.

After the prices plummeted, not only the profit margins of steel companies were greatly reduced, but the market was also greatly hurt. It is expected that news of production cuts and maintenance on the supply side in June will increase. It is expected that the pressure on the supply side will be eased, and the possibility of further increase in output is unlikely.

On the demand side, May and June are historically the off-season for seasonal consumption, and it is normal for the marginal weakening of demand. The resilience of rigid demand is still strong. The "two concentration" land market transactions were hot in May, and the start of real estate in the second half of the year may be worth looking forward to.

The shift of the policy focus is to gain time and price space for the "carbon peak" effort. Policy suppression and environmental protection and production restrictions will be the normalized long positions and short positions game concept in the second half of the year. In the short term, under the premise of policy suppression, the marginal weakening of fundamentals and the inflection point of inventories are approaching. It is expected that steel prices will continue to fluctuate downward after a brief stabilization.