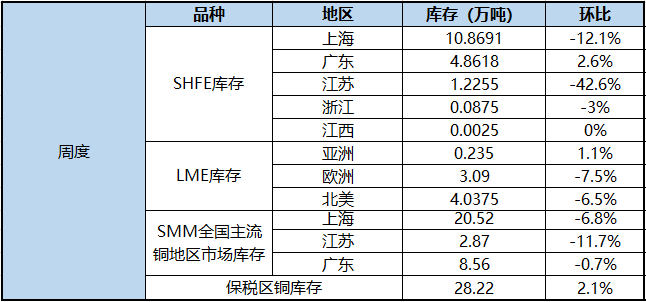

Copper:

Fundamentals, LME copper stocks fell 5275 tons to 73625 tons this week, stocks continue to be in a historical position to support copper prices, copper futures fell less than other base metals. However, domestic consumption is still not optimistic, especially there is no obvious improvement in the reserve warehouse cycle before National Day, the inventory of finished products in copper rod and cable factories is on the high side, the orders of copper processing enterprises are insufficient, the willingness of reserve warehouse before National Day is weak, and spot buying is weak. In addition, the tight supply of copper mines has eased marginally, and the supply side has gradually lost support for copper prices. Overall, the short-term macro dollar index is strong, copper prices are expected to be suppressed under a stronger dollar, while domestic consumption is lower than expected, and there is room for a correction in copper prices. It is expected that Lun Copper will operate at 6450-6650 US dollars / ton next week, while Shanghai Copper will run at 50000-51500 yuan / ton.

Aluminum:

The removal of electrolytic aluminum continued, with inventories falling by 24000 tons to 716000 tons on a weekly basis, while Guangdong and Jiangxi aluminum bars received an increase of 3900 tons to 71500 tons compared with last Thursday. Inventory in Foshan and Nanchang rose, while inventory in Wuxi, Changzhou and Huzhou declined.

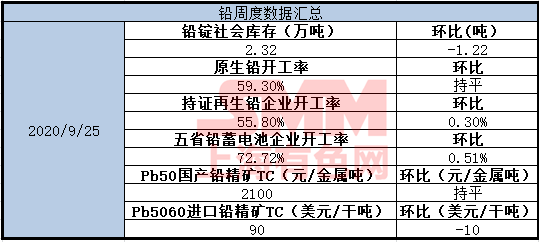

Lead:

Shanghai lead contracts continued to strengthen in recent months, market sentiment rose, Shanghai lead showed a trend of stabilizing and rebounding, but the good times did not last long, due to the depressed high-price shipments in the spot market, coupled with the rigid demand for downstream picking up goods, after the expected reduction of pre-holiday stock preparation, lead prices rose some short funds chose to short lead prices to hedge macro risks. At present, the social inventory has declined sharply, and the support for the contract in recent months is expected to be strong next week, the monthly difference may further widen, the overall lead decline is less than that of other varieties, and the technical level is focused on 14500-14700 yuan / ton.

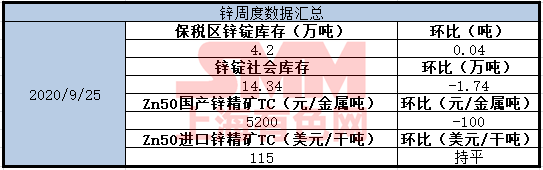

Zinc:

From a fundamental point of view, time has gradually turned to the fourth quarter, and the risk of a second outbreak of the epidemic has intensified. This week, risks have begun to emerge in Britain and the euro zone. According to the experience at the beginning of the year, the epidemic will first have a greater impact on consumption, that is, countries that have not yet achieved a complete economic restart may have their economies decline again, which directly affects overseas consumption and indirectly affects China's exports, which is worthy of vigilance. At the same time, we have also observed that the supply of overseas mines is still relatively tight, and the offer price of bulk orders is heard to be 80-100 US dollars / dry tonnage. If the supply fails to achieve volume until the fourth quarter, the profit level of smelters at home and abroad will be gradually compressed and suppress the enthusiasm of production. Gold, silver, silver and ten consumption peak season has passed, zinc price operation logic from consumption expectations to mineral supply is substantially tight switch, on the current supply and demand side, if the switching logic has not been confirmed, zinc may be overvalued. The current macro risk is greater, zinc prices are expected to fluctuate within the range. It is expected that the main zinc in the next cycle will run around 18700-19500 yuan / ton. It is expected that the spot price of zinc in Shanghai will rise by 140,280 yuan / ton in October, and that Lun zinc will run around 2350-2500 US dollars / ton next week.

Nickel:

As of Friday, SMM's total pure nickel inventory was 40492 tons, down 1821 tons from last Friday. According to investigation and statistics, the weekly output of nickel plate is about 2900 tons and that of nickel beans is about 500 tons. In terms of storage, the import of nickel plates in Shanghai is about 1500 tons, and the import of nickel beans is about 600 tons. In other areas, the inventory in Guangdong has been restocked after the supply of electroplated nickel, while the inventory in Liaoning and Tianjin in the north is in a state of net outflow. Inventories in Jiangsu and Zhejiang continue to be flat. To sum up, SMM original warehouse receipt spot inventory decreased by 1640 tons, SMM six pure nickel social inventory decreased by 1821 tons, and domestic pure nickel social inventory decreased for the third consecutive week.

Tin:

The price of Shanghai tin fluctuated from the beginning of this week to Wednesday morning, and the US dollar rose sharply on Wednesday. The metal disk was completely frustrated. Tin prices in Shanghai fell with the futures price on Wednesday afternoon, and tin prices reached a recent low on Thursday and Friday. The small card is about 140500 yuan / ton. By Thursday, the downstream delivery was more active, the market supply was less, the demand was more, and the sticking water rose somewhat. The set price of Yunxi rose 1500 yuan / ton against the Shanghai tin futures 2011 contract, Yunzi rose 500-1000 yuan / ton, and the small card rose around 500 yuan / ton.

![Sharp Decline in Copper Prices Prompted Some Downstream Enterprises to Operate at Full Capacity, and Spot Copper Turned to Premiums Across the Board [SMM South China Copper Cathode Spot Weekly Review]](https://imgqn.smm.cn/usercenter/IHqPw20251217171709.jpg)