SMM7 March 30: recently, a number of iron ore miners released performance reports, according to SMM statistics, the major mining enterprises were less affected by the epidemic in the second quarter. Among the big four miners, Rio Tinto and BHP Billiton completed about 50 per cent of their production in the first half of 2020, while FMG production reached about 48 per cent in the first half of the year. However, the production completion of Brazil Vale in the first half of 2020 accounts for only 42% of the lowest target for the whole year, and the second half of the year is expected to increase by about 50 million tons over the first half of the year in order to achieve the minimum guidance target. In the later stage, we need to continue to pay attention to its production and transportation changes.

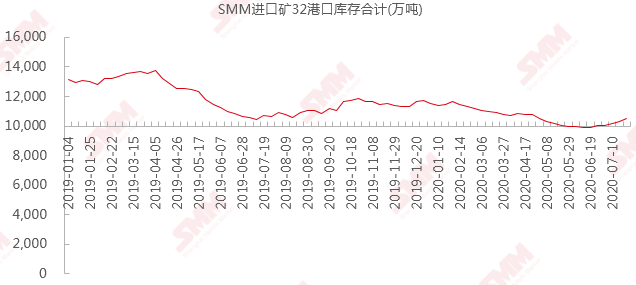

In the first half of the year, due to the strong domestic iron ore demand and foreign mineral supply due to the impact of the epidemic, mineral prices fluctuated sharply, and the overall trend fluctuated. The tight supply situation is clearly reflected in inventories. In the first half of the year, SMM tracked inventories of 35 ports below 100m tons for several consecutive periods, while iron ore stocks hovered at nearly three-year lows. Although the supply of iron ore has eased recently, it is still difficult for ore prices to fall:

On the supply side, SMM tracking data show that a total of 93 ships have arrived at eight major ports in China, and the incoming cargo volume is expected to be 15.22 million tons, a decrease of 1.67 million tons compared with the previous period and an increase of 810000 tons over the same period last year. During the period, Australian port departures fell 160000 tons from the previous month to 16.56 million tons, but increased significantly by 2.49 million tons compared with the same period last year. Brazil's port departures increased by 910000 tons to 6.73 million tons, but decreased by 1.37 million tons compared with the same period last year. Recently, the impact of port maintenance in Australia and Pakistan has weakened, the supply side of iron ore continues to be loose, and the inventory of imported ore ports is expected to continue to accumulate.

On the demand side, according to a survey by SMM, the operating rate of blast furnace in the last week of July was 90.3%, up 0.23% from last week. The increase mainly comes from the completion of overhaul of some steel mills affected by floods this week, and it is expected that the operating rate of blast furnace will be high and stable next week.

In terms of port inventory, SMM tracked inventory totaling 105.21 million tons, an increase of 2.31 million tons over the previous month and a decrease of 1.09 million tons over the same period last year. Port inventory has accumulated for the sixth week in a row, and the growth rate continues to expand. Due to the recent floods in the areas along the Yangtze River, some steel mills have increased their overhaul and furnace maintenance, resulting in a drop in port inventory compared with the previous month, and an increase in the inventory of some ports along the Yangtze River. With the weakening of the impact of rainstorm and flood in the later period, and the opening of port dredging in Tangshan area, the daily dredging of imported mines is expected to rise month-on-month.

SMM believes that the probability of iron ore entering August is still high, and there is even a chance to hit a new high if there is an abnormal supply in Brazil. Although it has reached the traditional off-season, the demand suppressed by Rain Water in the early stage continues to be released, the demand is good, and the overall hot metal output is stable. And recently, there are more iron ore coming to Hong Kong, and the port inventory has been accumulated for the sixth consecutive week, but the structural shortage has a strong support for the spot. On the other hand, the current long-process steel mill thread and hot coil profits are between 202 and 357 yuan / ton, some steel mill profits are expanding, the demand for mainstream fine ore is only increasing, and the mainstream fine ore price is expected to continue to be strong.

In the second half of the year, iron ore as a whole is not likely to be stronger than in the first half, but it is also hard to plummet. As it may be difficult for domestic demand to increase significantly in the second half of the year, but it will not be much worse than in the first half of the year, and the epidemic in Brazil and India is still severe, there are uncertainties in supply. From the semi-annual data, the late iron ore supply turned to marginal easing, but low inventory support, mainly driven by steel demand, iron ore or from leading the rise to the market to follow the trend.

Iron ore main connection trend

"Click to view SMM iron ore port inventory

Quarterly report of major mines

Vale

In the second quarter of 2020, Vale iron ore powder production was 67.6 million tons, of which monthly production in June exceeded 25 million tons, showing a strong increase from April and May levels, due to the arrival of seasonal high production periods as rainfall decreased. The production and operation rate of S11D reached the level of 91 million tons / year in June and is likely to increase in the second half of the year, and the annual output is expected to be slightly more than 85 million tons. "check the details.

BHP Billiton

BHP Billiton released its second-quarter production report, which showed that BHP produced 67 million tons in the second quarter, an increase of 11% over the previous quarter. Production in the current fiscal year reached 248 million tonnes, 4 per cent higher than in fiscal 2019. In terms of sales, BHP Billiton sold 77.05 million tons of iron ore in the second quarter, up 13% from the previous quarter and 7% from the same period last year, including 50.9 million tons of fines and 17.25 million tons of lump ore. The total sales volume in the first half of 2020 was 145 million tons, an increase of 8% over the same period last year.

Rio Tinto

According to Rio Tinto's second-quarter production and sales report, iron ore shipments in the Pilbara business were 86.7 million tons in the second quarter, up 19 per cent from a month earlier and 1 per cent year-on-year. Iron ore production in the Pilbara business was 83.2 million tonnes in the second quarter, up 7 per cent from a month earlier and 4 per cent year-on-year. The total output in the first half of the year reached 161 million tons, an increase of 3 percent over the same period Although the epidemic has a certain impact on operations, the volume of shipments is still on the rise compared with the same period last year. Spot sales at the port developed steadily in the second quarter, with a total sales volume of 1.7 million tons. Although Hurricane Damien had a serious impact on infrastructure and ports in February, it performed well in the second quarter, with iron ore shipments of about 160 million tons in the first half of the year, an increase of 3 percent over the same period last year.

FMG

Australian miner FMG released a quarterly report showing that iron ore processing reached 42.7 million tons in the second quarter, up 1% from a month earlier and down 12% from a year earlier. FMG iron ore shipments reached 47.3 million tons in the second quarter, up 12 per cent from the previous quarter and 2 per cent year-on-year. FMG2020's total shipments for the fiscal year reached 178 million tons, up 6% from a year earlier, higher than the company's previous fiscal year upper limit (1.75-177 million tons), mainly due to record shipments in the fourth quarter of the fiscal year. The company said the rebound in demand from China, the largest importer of iron ore, provided support for iron ore prices, although the epidemic situation in other countries and regions of the world is still not optimistic. "check the details."

"SMM online Q & A" has come to the market, price, information if you have any questions, feel free to ask!

Scan the QR code and join the SMM metal communication group.

![[SMM Hot-Rolled Coil Daily Transactions] Spot Transactions Weakened Somewhat](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)