CHANGSHA, Jul 23 (SMM) – China’s zinc concentrate supply will be sufficient in Q3 and Q4 this year, while TCs for domestic and imported concentrate are likely to rise further, according to senior zinc analyst Darius Li.

Li was presenting his outlook on the China domestic zinc market at the 2020 (15th) Lead and Zinc Summit held by SMM at Changsha, China.

Zinc concentrate stocks stood at 15,000 mt in Fangchenggang and 130,000 mt in Lianyungang as of July 17. Domestic zinc smelters kept raw material inventories that could guarantee production for 28 days on average as of July 10, an SMM survey showed. Treatment charges (TCs) for zinc concentrate fell as raw material stocks at smelters returned to normal levels.

Zinc concentrate mines have slashed output in 2008 and 2015 when zinc prices slumped. Prices in 2008 were highly correlated with TCs for domestic zinc concentrate, while prices in 2015 declined six months earlier than TCs fell. Domestic mines should consider initial investment costs (such as prices of exploration and mining rights) before cutting output, and some state-owned mines will not reduce production easily despite large losses as they need to ensure employment and production.

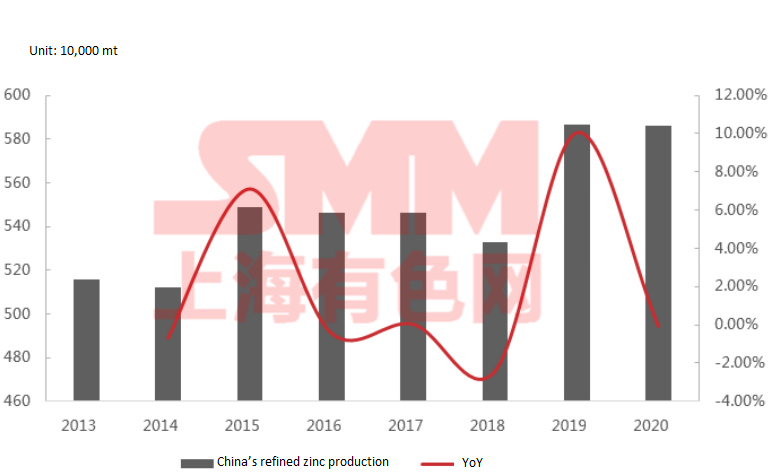

“China’s zinc concentrate supply will be sufficient in Q3 and Q4, and TCs for domestic and imported concentrate are likely to rise further, as overseas mines have gradually resumed production and shipments. China’s refined zinc output is likely to increase in the second half of this year amid a prospect of higher profits,” Li said.

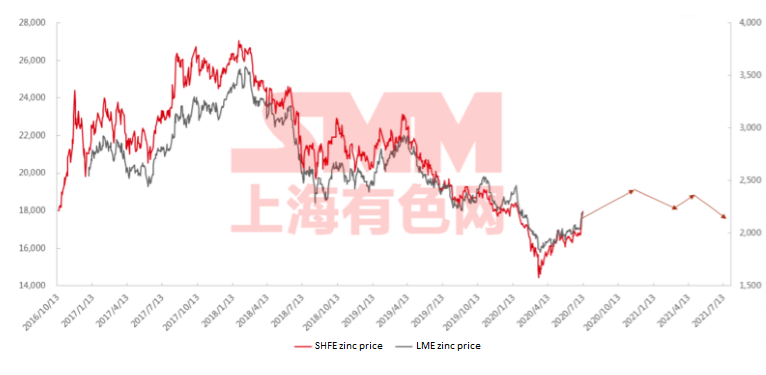

Zinc prices positively correlated with inventories

Zinc prices has fallen to a new low in end-March since mid-April 2016 of 14,265 yuan/mt amid the widespread of COVID-19 in China, and has since rebounded, generating a V-shaped curve.

SHFE and LME zinc prices (Unit: yuan/mt, $/mt)

Li said that compared with lead, zinc prices are positively correlated with inventories. “For instance, inventories shrank continuously in 2019, but zinc prices fell rapidly. Refined zinc saw a large supply surplus since April 2019 as its output soared.”

China’s refined zinc production (Source: SMM)

Li also noted that although the COVID-19 crisis has caused huge dent on overseas zinc consumption, but a global zinc supply glut remained in place. Zinc prices are expected to increase as consumption recovers.

Li also pointed out the reasons for mines to reduce or suspend production. Mines in high-altitude areas, such as Tibet, Xinjiang and Inner Mongolia have suspended operations seasonally and postponed resumption amid COVID-19. On the other hand. some mines halted production due to environmental protection restrictions or cash flow issues, while some mines cut output due to production losses.

Shortage of storage space for sulphuric acid, tight supplies of zinc concentrate and zinc slag and routine maintenance were major reasons for domestic zinc smelters to trim output in Q1. For instance, shortage of storage space for sulphuric acid, tight feedstock supply and equipment breakdown affected nearly 340,000 mt of operating capacity in Inner Mongolia, accounting for 50% of total local capacity. The tightness in raw material supplies and routine maintenance disrupted 520,000 mt of operating capacity in Sichuan, accounting for 75% of the total.

As for galvanising producers, COVID-19 has caused a dent on domestic consumption, but galvanising consumption was strong. This is mainly due to support from infrastructure projects. Floor space under construction and excavator sales were sluggish in H1 2020, but indicators rallied in late Q2 as COVID-19 has been successfully contained in China. Output and sales of automobiles rose slightly, demand for home appliances was strong, but operating rates at semi-steel tire producers remained low.

Meanwhile, orders of die-cast zinc alloy and end products were sluggish, weighing on zinc consumption in Guangdong. Weak automobile output and sales has also cast a shadow on the zinc oxide industry.