SMM7 March 17: the epidemic that occurred at the beginning of this year has had a tremendous impact on the global economy and industrial development. For the cobalt lithium new energy industry, the market supply and demand structure has also undergone significant changes. However, since March, China and Europe have issued optimistic policies for the new energy vehicle industry, which undoubtedly releases a positive signal for the future development of "electrification". In this way, the SMM new energy analysis team investigates and integrates the production data of China's core battery materials, summarizes the trend characteristics combined with the price trend, and makes a judgment and forecast of the price trend in the second half of 2020.

This is the third of a series of analysis reports, which describes the conclusions and forecasts of the core data of the positive industry:

From January to June 2020, China's total output of ternary materials was 70, 000 tons, down 36.3% from the same period last year, and 15.8% lower than in the second half of 2019. SMM expects the output of ternary materials in the second half of 2020 to be 114000 tons, down 5% from the same period last year.

From January to June 2020, China's total output of lithium iron phosphate was 48000 tons, up 16.6 per cent from the same period last year and 5.6 per cent lower than in the second half of 2019. SMM expects lithium iron phosphate production in the second half of 2020 to be 71000 tons, up 30.3% from the same period last year.

From January to June 2020, China's total output of lithium manganate was 20,000 tons, down 26.1 percent from the same period last year and 21.5 percent lower than in the second half of 2019. SMM expects lithium manganate production to be 30, 000 tonnes in the second half of 2020, down 3.1 per cent year-on-year.

From January to June 2020, China's total output of lithium cobalt was 27000 tons, up 4 per cent from the same period last year and 0.6 per cent lower than the second half of 2018. SMM expects lithium cobalt production to be 29000 tons in the second half of 2020, down 7.1 per cent from the same period last year.

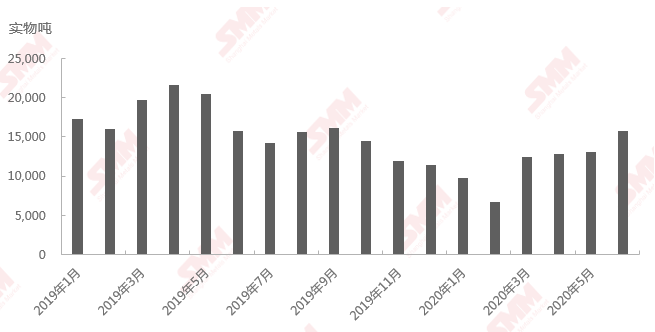

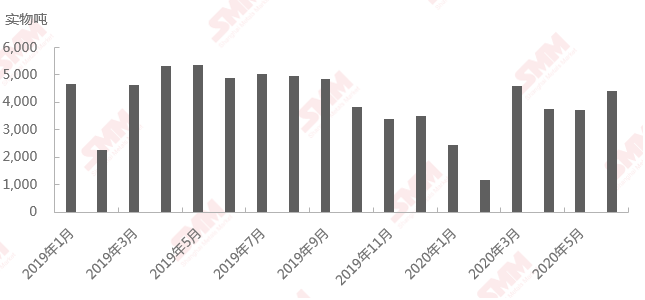

Output of ternary materials in China since January 2019

From January to June 2020, China's total output of ternary materials was 70,000 tons, down 36.3 percent from the same period last year and 15.8 percent lower than in the second half of 2019. Among them, the output in June was more than 15000 tons. In the first half of the year, no enterprise produced more than 10,000 tons, with a CR10 of 71.1% and a CR5 of 45.4%. In June 2020, China's total output of ternary materials was 15730 tons, an increase of 0.03 percent over the same period last year and 20.4 percent month-on-month, the highest output in the first half of 2020.

According to SMM research, the output of ternary materials decreased significantly in February compared with the same period last year, mainly for the following reasons:

1. At the beginning of this year, the domestic epidemic began to break out. In February, Sanyuan material factories generally started relatively late. Due to the difficulties of logistics and workers' rework, the operating rate of material factories was only 30%.

2. The number of workers in the downstream battery factory is relatively large, the proportion of non-local workers is relatively high, and its operating rate is even lower. Sanyuan material enterprises are greatly affected by the terminal market, the trading in the power market is weak in February, car enterprises and battery factories basically use pre-year inventory, and the purchase volume has dropped sharply.

According to this, although part of the production line of the domestic head battery factory has not stopped during the Spring Festival, the demand of the downstream car market is weak, the inventory of batteries and materials is high and the consumption rate is slow in the first quarter of 2020.

In the second quarter of 2020, the overseas epidemic began to aggravate, the export of ternary batteries was blocked, and the purchase of high-nickel ternary products by domestic head battery enterprises decreased sharply, affecting the proportion of high-nickel products. In addition, overseas markets radiated to ternary material factories, and the exports of some enterprises decreased by 10% and 20%.

In addition, the small power market is becoming more and more popular in the first half of this year, especially since May, the demand for bicycles in overseas European markets has increased, domestic electric bicycle exports have begun to increase, and domestic shared electric bicycles have continued to increase in various cities. Therefore, the ternary order of 5 series continues to increase every month, and the proportion also increases.

According to SMM understanding, the current domestic power market increment is not obvious, battery factories still have part of the inventory, procurement is not active enough. Downstream digital and small power market demand continues to increase, SMM expects the output of Sanyuan materials plant in July may be slightly higher than in June. As the current high-nickel ternary orders of battery enterprises represented by C are gradually stable, the regular order quantity of 8-series ternary materials is expected to return to normal in August. In addition, car companies will mainly reduce costs this year, and some new models will use partial proportions of 5 and 6 series ternary batteries.

SMM predicts that in the second half of the year, many car companies will release new models, such as Lai EC6, Xiaopeng P7, Changan CS55 E-ROCK, brilliance BMW iX3, Volkswagen ID.3, etc., the operating rate of battery factories will continue to increase, coupled with national and local policy support and the gradual recovery of domestic consumer demand, the power market will pick up in the second half of the year, and SMM forecasts that the output of ternary materials in the second half of the year is expected to be 11.4 tons.

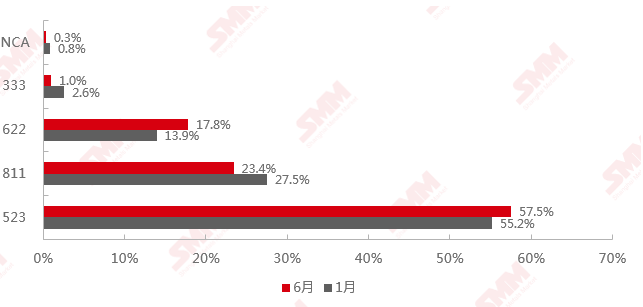

2020年1月、6月中国三元材料产品结构对比

From the point of view of the yield structure, the proportion of high nickel in June decreased slightly compared with that in January, mainly because the ternary demand for high nickel was still gradually recovered by the epidemic in June, and high nickel is still a trend in the long run. In June, the ternary material 523 accounted for 57.5%, compared with January this year, the proportion increased by 2.3%, the proportion increased by 17.8%, and compared with January, the proportion increased by 3.9%. The proportion of high nickel 811 and NCA accounted for 23.4% and 0.3%, respectively, which decreased slightly compared with January.

At present, domestic foreign battery factories are still dominated by high nickel ternary, and the high nickel ternary demand of head battery enterprises is also gradually recovering. This year, domestic car companies still take cost reduction as the main goal, and the new models are installed with 5-and 6-series ternary batteries in a partial proportion. SMM predicts that the output of high-nickel ternary materials will continue to increase in the second half of the year, but the growth space is limited, and the product structure of ternary materials will still be dominated by 5-series and 6-series.

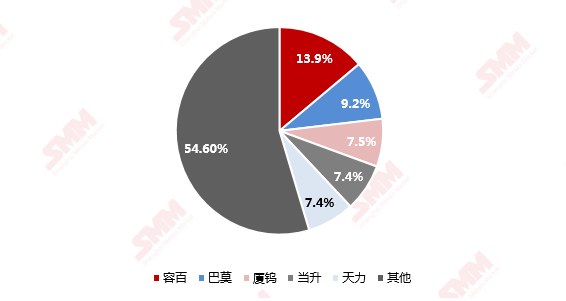

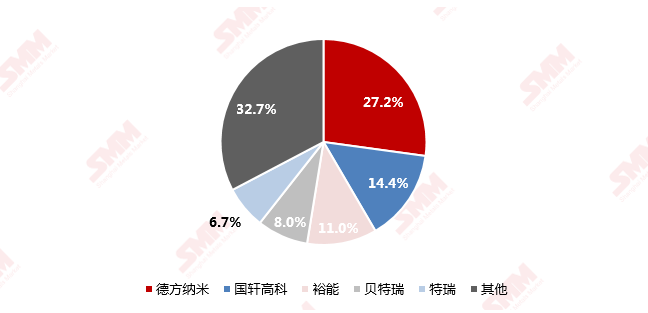

2020年H1三元材料生产商前五名市占率

Source: SMM

The market share of ternary material Top 5 has reached 45.4%, and now the industrial concentration is stronger than in 2019. Large factories are actively expanding production after stable cooperation with downstream power battery factories, while small and medium-sized factories are facing the problem of overcapacity. According to SMM, there are many new production capacity planning enterprises from 2020 to 2022, such as Xiamen tungsten industry will put into production of 10000 tons of medium and high nickel ternary materials by the end of 2020, Hunan fir design and construction of high nickel cathode material plant with an annual output of 28800 tons, Dangsheng science and technology will build a cathode material plant with the first phase of 50, 000 tons and a total capacity of 100000 tons, and long-term lithium will begin construction in April to expand the production line of 80, 000 tons of high nickel. Rongbai Science and Technology will be built in three phases and will expand its high nickel production capacity of 100000 tons by the end of 2025. As the current capacity utilization rate of the ternary material industry is less than half, the trend of product customization is significant, and the gross profit level varies greatly, SMM expects that only a few enterprises that have good cooperation with the downstream or have the advantage of upstream raw materials have certain practical significance in their production expansion plans. It is estimated that the production capacity of ternary materials in China will reach 800000 tons in 2022.

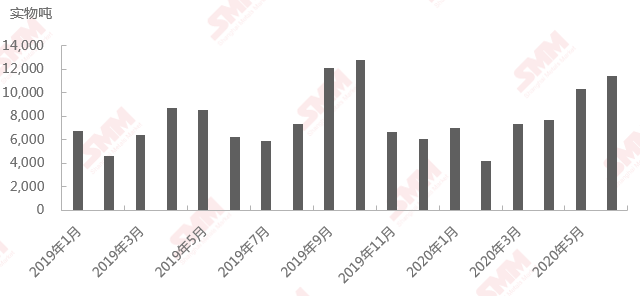

2019年1月至今中国磷酸铁锂产量

From January to June 2020, China's total output of lithium iron phosphate was 48000 tons, up 16.6 per cent from the same period last year and 5.6 per cent lower than in the second half of 2019. In the first half of the year, a total of two enterprises produced more than 6000 tons of lithium iron phosphate, with a CR10 of 89.2% and a score of 63.9%. In June 2020, China's total output of lithium iron phosphate was 6180 tons, an increase of 84.6 percent over the same period last year and 10.9 percent month-on-month, the highest monthly output in the first half of the year.

The number of 5G base stations increased greatly in the first half of this year, and the demand for iron-lithium batteries increased significantly, and most small and medium-sized enterprises competed for energy storage orders. This year, the price of energy storage iron lithium battery has been greatly reduced, the cost of the battery system has been reduced to about 0.6 yuan / Wh, the performance-to-price ratio has been improved, and lead-acid batteries have been gradually replaced. In addition, electric bicycles began to increase this year, taking into account the safety and cost, the advantages of iron-lithium batteries are outstanding, and the demand is also gradually increasing.

In terms of the power market, the performance of the car market in the first half of 2020 was poor, with a serious decline in overall production and sales compared with the same period last year, and the demand for iron-lithium batteries also However, with the release of the Tesla iron lithium version of the model 3 model in the second half of the year, BYD "Han" began to deliver, and orders for iron-lithium batteries increased significantly. In addition, in the policy of "New Energy vehicles going to the Countryside" issued on July 15, the demand for iron and lithium will also rise for many A00-class models, such as the miniEV of SAIC GM Wuling.

With the increasing proportion of lithium iron in passenger vehicles and more obvious advantages in new energy commercial vehicles, coupled with the increment of energy storage and small power market, SMM expects that lithium iron phosphate production will continue to increase in the second half of the year, and production is expected to be 71000 tons in the second half of the year.

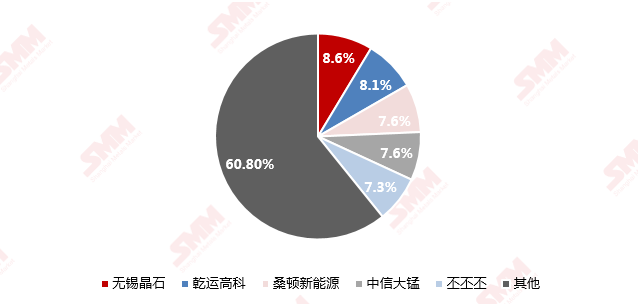

Top five market share of H1 lithium iron phosphate manufacturers in 2020

The concentration of lithium iron phosphate market in the first half of 2020 is still very high, with the top five accounting for 63.9%. At present, the polarization of lithium iron phosphate market is still serious, only a few head iron lithium enterprises have close cooperation with downstream power battery factories, enterprises continue to expand production, capacity utilization is also gradually improving. At present, the downstream orders of other small and medium-sized iron and lithium enterprises are mainly energy storage and small power market, with serious overcapacity, fierce market competition and declining prices. SMM expects competition in the iron-lithium market to continue in the second half of the year, and the top five may change.

Output of lithium manganate in China since January 2019

From January to June 2019, China's total output of lithium manganate was 20,000 tons, down 26.1 percent from the same period last year and 21.5 percent lower than in the second half of 2019. In the first half of the year, no enterprise produced more than 2000 tons, with a CR10 of 71.3% and a CR5 of 31.9%. In June 2020, downstream demand increased slightly. China's total output of lithium manganate was 4410 tons, down 10 per cent from the same period last year and 18.9 per cent higher than the previous month.

Affected by the domestic epidemic situation from January to February this year, lithium manganate enterprises resumed production relatively late, the operating rate was low, and the output of lithium manganate declined seriously compared with the same period last year. In March 2020, most lithium manganate manufacturers resumed production, overseas orders were normal, and the output in March was the highest in the first half of the month. Affected by the overseas epidemic in the second quarter, orders for downstream consumer batteries and consumer products were delayed or cancelled, affecting the demand for lithium manganate materials. Production increased slightly in June due to domestic demand for hand-held electric fans, but the overseas market has not yet recovered and the increase is not obvious.

SMM believes that with the improvement of the overseas epidemic in the future, especially the resumption of orders in Southeast Asia, the production of lithium manganate will return to normal. In addition, the domestic market for electric bicycles and power tools will also drive part of the output of lithium manganate. During the peak consumer market season in the second half of September, SMM expects demand for lithium manganate to increase in the second half of the year, with production expected to be 30, 000 tons.

Top five market share of H1 lithium manganate manufacturers in 2020

Due to the low industry threshold and scattered downstream demand, lithium manganate is involved in consumer, power and small power categories. There are more lithium manganate producers, the industrial concentration is lower than other cathode materials, the market share of Top 5 is 31.9%, and the market competition is fierce.

![[SMM Analysis] The arrival volume of spodumene in January 2026 reached a record high then declined in February.](https://imgqn.smm.cn/usercenter/zWZVI20251217171730.jpg)