SMM7 March 16:

As of July 16, the country's total inventory of building materials was 10.7401 million tons, with a month-on-month ratio of + 0.6%, compared with the same period last year. Seasonal interference has not faded, central China, East China, southwest and other areas are still shrouded in overcast and rainy weather, terminal demand continues to be suppressed, so the thread inventory is still in a state of accumulation. However, after South China took the lead in "getting rid of difficulties", the strong replenishment of local demand is an important argument to prove the objective existence of the demand for quick work. The urgent demand for work is more urgent than in previous years, and the terminal just needs a good year-on-year performance, which is an important reason why the current inventory growth continues to narrow year-on-year (this week, the thread pool growth rate narrowed by 3 percentage points year-on-year).

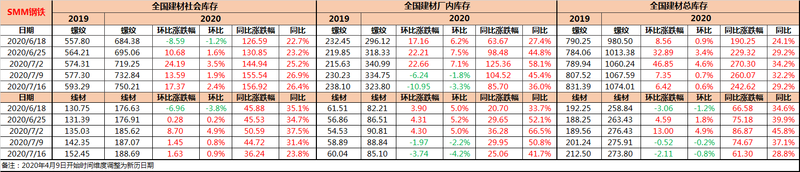

Table 1: Overview of thread inventory

Source: SMM

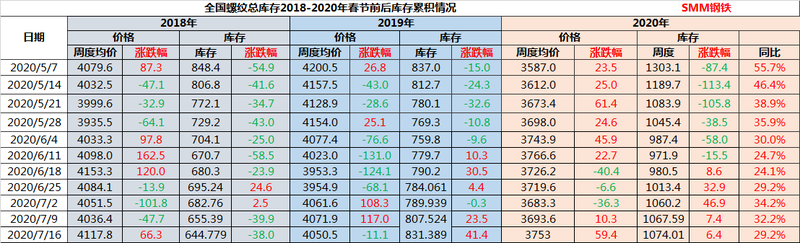

Table 2: comparison of Thread inventory prices from 2018 to 2020

Note: due to the epidemic factors since 2020, due to the different opening times in different places, there is a certain error in the actual spot average price; the time dimension is the Gregorian calendar date.

Source: SMM

Specifically:

Social inventory of 7.5021 million tons, an increase of 173700 tons this week, + 2.4% month-on-month, + 26.9% year-on-year.

Under the background of a positive situation in the A-share bull market, the raw material side was led by the news side to rise first, driving the period snail to continue the strong situation in the past two weeks. The expectation of the spot market for the future is also improving, and the enthusiasm of traders to take goods has been significantly improved, accelerating the transfer of the factory warehouse to the social warehouse. While the terminal "steel needs" is "serious illness has not been cured", so the speed of accumulation has been accelerated.

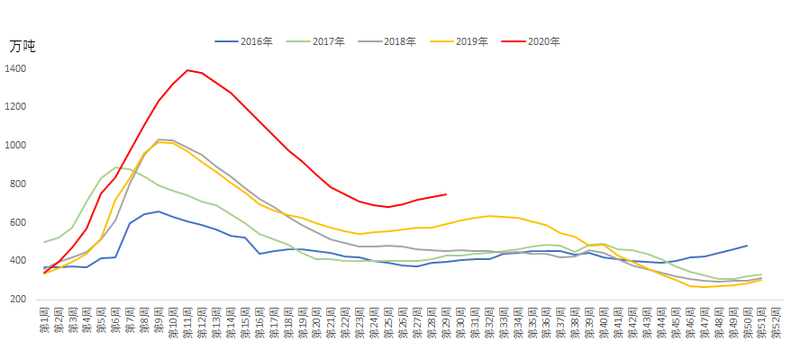

Figure 1: an overview of the trend of threaded community library since 2016

Source: SMM

The inventory in the plant is 3.238 million tons, down 109500 tons this week,-3.3% month-on-month, + 36.0% year-on-year.

In addition to the market merchants' enthusiasm for taking goods driven by strong expectations, the decline in the output of steel mills is also an important reason for the decline in the factory warehouse. Under the dual pressure of high plant pressure and poor profitability, the overhaul and production reduction plans of steel mills have increased-according to SMM research, the planned rebar output of blast furnace steel mills in July decreased by 2% compared with the actual output in June, and the operating rate of electric furnace plants also dropped by about 11.52% compared with the same period in June.

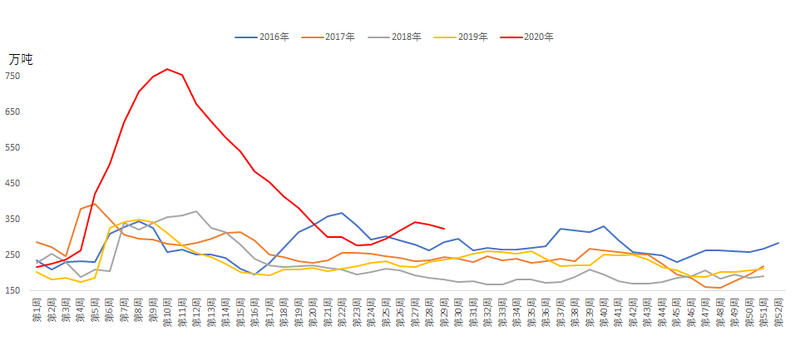

Figure 2: an overview of the trend of thread factory warehouse from 2016 to now

Source: SMM

In the short term, the fundamentals of rebar are not unusual-the supply side is likely to maintain a small fluctuation at the current level, the demand side continues to be hit by precipitation, the road to rebar accumulation is not over, and steel prices are still in an awkward position of "neither up nor down". However, as more and more regions out of the "rainy season" haze, rush demand released as scheduled, thread fundamentals regained strong support, steel prices are expected to consolidate and continue to start.

![[SMM Hot-Rolled Coil Daily Transactions] Spot Transactions Weakened Somewhat](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)