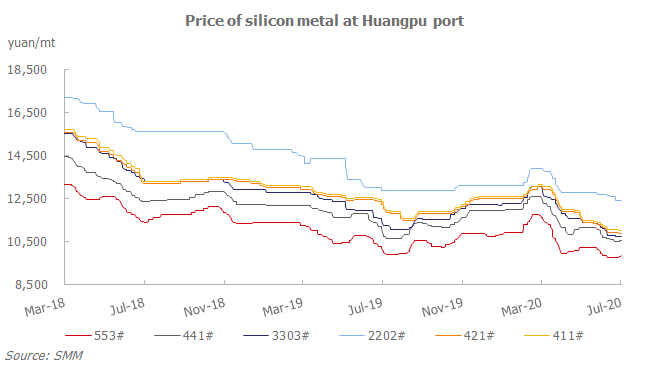

SHANGHAI, Jul 15 (SMM) – Silicon prices returned to a downward trend in June after stabilising in May, as supply increased with ramped-up production in Yunnan and Sichuan, while demand in the domestic and overseas markets failed to post same growth. Trades were thin amid pessimistic sentiment.

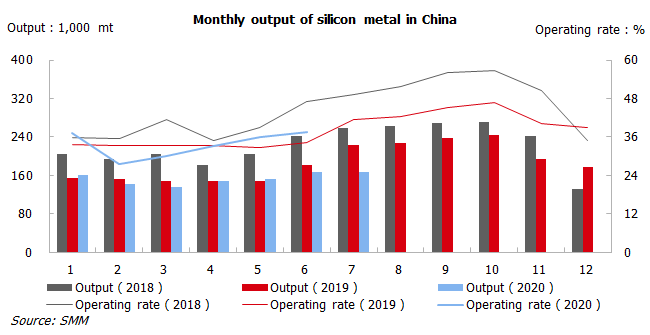

By mid-June, prices of some low-grade specifications declined to the lowest levels in three years, below the costs of some production capacity, and this led to increased suspension at producers. But the capacity additions in south-west China will continue to contribute to output growth. This, coupled with the resumption of work in north China, will likely see the national operating rates of silicon mills in August reaching peak level of the year.

Resumption of the export market will be the major driver for consumption during the June-September period. Downstream producers in major export destinations of Asia, such as Japan, South Korea and Thailand started to make enquiries and restock after they restarted operation. This improved China’s export trades in June, as compared with May, and new orders will be mostly delivered in July-August.

However, the resumption of downstream production in Europe and the Middle East remained at a slow pace, as some major producers have cancelled purchase tenders for Q3 or the second half of the year. The shipments for Q2 orders have been delayed to H2 2020.

SMM expects China’s monthly average exports of silicon in June-September at 50,000 mt, still lower from a year ago, and the loss in exports in H1 may not be offsetted in H2 2020.

Operations at Chinese silicon mills edge higher in July. On the downstream front, operations at aluminium alloy and polysilicon producers are slightly weaker than June while higher production of organosilicon monomer and a rise in exports result in overall higher demand.

Purchases have increased after silicon prices rebounded from the bottom levels in June, but restocking demand was limited as most of the procurement was for the fulfilment of backlogged orders. Some buyers raised the quantity for each purchase while lowered the purchase frequency.

SMM expects silicon prices to remain stable in July. Zero price spread between high and low-grade silicon products at the start of the month will be unable to sustain, as supply resumption from major mills in Xinjiang in late-July will weigh on prices of low-grade silicon. Average prices of chemical-grade 421# silicon will slightly recover in August, and the price spread between different specifications will return to normal levels.

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)