SMM7 March 15: today, at the "China Tungsten Industry Market and Application Summit Forum and China cemented Carbide Market Application Symposium", Hu Yan, a senior analyst from SMM tungsten industry, brought a speech on the theme "Review and price prospect of China's tungsten industry market in 2019-2020". The content covers the distribution of global tungsten reserves to tungsten concentrate output, tungsten concentrate import and export to industrial policy, major events review, tungsten concentrate and ammonium paratungstate price trend are reviewed and prospected.

Global tungsten reserves

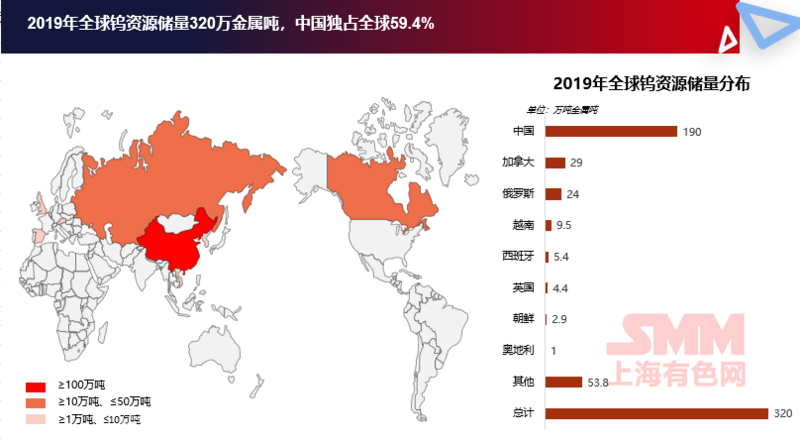

The global tungsten resources are mainly concentrated in China, Canada, Russia and other countries. According to the data of the US Geological Survey, in 2019, the global tungsten reserves were 3.2 million tons, while China's tungsten reserves were 1.9 million tons, accounting for 59.4 percent of the global total. In addition, countries with more than 100000 tons of metal are Canada and Russia.

The most typical tungsten mines in Canada are Cantung and Mactung, but due to environmental and traffic reasons, the operating cost of Cantung tungsten mine is too high and there is basically no profit, so production has been suspended since 2016. Mactung tungsten mine also shelved development again in 2016.

Russia's tungsten resources are mainly concentrated in the North Caucasus, East Siberia and the far East. In the past, most of Russia's tungsten mines were exported to Japan and China. However, in recent years, Russia has strengthened the integration, development and utilization of domestic tungsten resources, so the number of exports has declined.

Excluding the three countries mentioned above, China, Canada and Russia, the remaining 20% of the world's tungsten resources are scattered in Vietnam, Spain, the United Kingdom, North Korea and other countries.

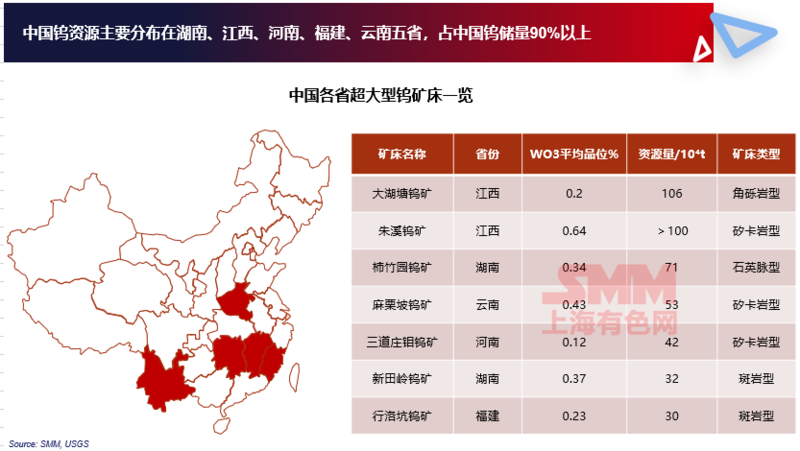

China's tungsten resources are mainly distributed in Hunan, Jiangxi, Henan, Fujian and Yunnan provinces, accounting for more than 90% of China's tungsten reserves.

The table on the right lists several super-large tungsten deposits in China, including Dahutang Tungsten Mine and Zhuxi Tungsten Mine in Jiangxi, Shizhuyuan Tungsten Mine and Xintianling Tungsten Mine in Hunan, and Malipo Tungsten Mine in Yunnan, Sandaozhuang Tungsten Mine in Henan and Xingluokeng Tungsten Mine in Fujian.

At present, the identification rate of tungsten resources in China is only 30%. Driven by the active exploration of major tungsten enterprises, the potential of domestic tungsten resources is expected to be further released in the future.

Tungsten resources in China

Tungsten concentrate output

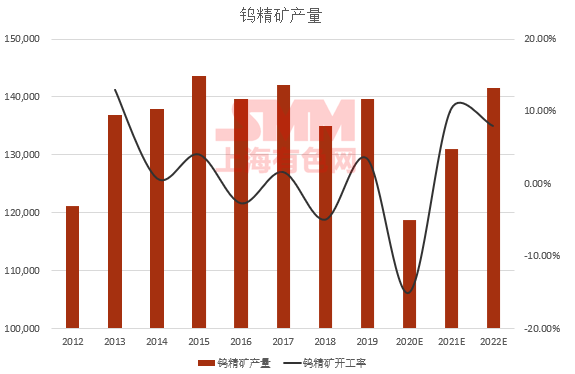

According to SMM, China's tungsten concentrate production was 121000 tons in 2012, and has basically increased year by year since 2013, with only a slight decline of 3 per cent and 5 per cent in 2016 and 2018, respectively.

The decline in production in 2016 is related to the industry self-discipline of large domestic enterprises. In November 2015, the price of tungsten concentrate fell to its lowest point in recent years, and the eight major tungsten enterprises in China jointly decided to limit the production of tungsten concentrate by 20%. So during the period of December 2015 and March 2016, tungsten concentrate production dropped significantly.

The slight decline in output in 2018 is mainly due to several reasons: first of all, in that year, with the strengthening of safety supervision, environmental protection, and resources, some tungsten mines stopped production and some trading enterprises of mineral products stopped production or changed industries. Second, with the regulatory authorities stepping up the verification of resource exploitation in the past two years, the phenomenon of overmining in areas such as Jiangxi and Hunan has been effectively alleviated, and the overmining rate has dropped significantly; and we know that the overmining rate of domestic tungsten resources may be close to 50% in 2017.

Compared with 18 years, the situation in 19 years tends to be stable, and the total output of tungsten concentrate is about 140000 tons. At the symposium of the China Tungsten Association in May 2019, the eight major domestic tungsten enterprises agreed to reduce production to a certain extent in order to jointly maintain the supply order of the tungsten raw material market.

2020, as we all know, is a very special year. Affected by the epidemic of Xinguan pneumonia, the production of tungsten concentrate in China decreased greatly in the first half of the year, especially in the first quarter of this year. Combined with the situation for the whole year, we think that the total output this year will drop by about 15% compared with the same period last year.

In the following two years, 2021 and 2022, mine production and downstream demand will gradually recover. However, due to domestic policy control, resource endowment, mining cost, safety and environmental protection and other problems, the output of the main tungsten mine is difficult to achieve great growth in the future. So the growth rate in the past two years will be about 10%.

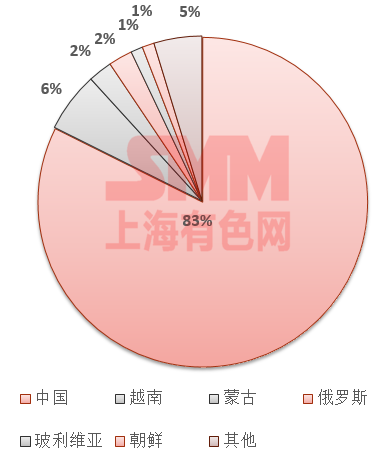

In 2019, China's tungsten concentrate production accounts for more than 80% of the world's total output. In addition, the main producing countries are Vietnam, Mongolia, Russia and so on.

Global distribution of tungsten concentrates in 2019

China's imported tungsten products are mainly concentrated in tungsten concentrate, or among the main tungsten products, the only net imported product is tungsten concentrate.

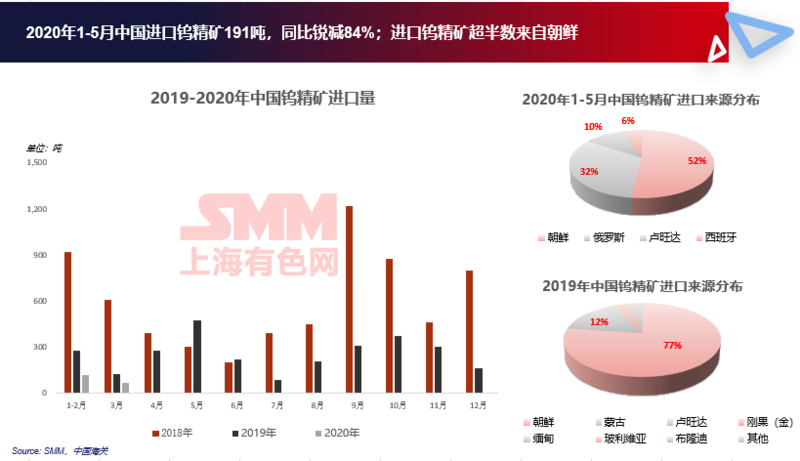

China imported 2846 tons of tungsten concentrate in 2019, a sharp decrease of 57 per cent compared with 2018.

From January to May 2020, China imported 191 tons of tungsten concentrate, a sharp decrease of 84% compared with the same period last year. Of course, we can understand that it is affected by epidemic factors.

China generally imports tungsten concentrate from North Korea, Russia, Mongolia, Rwanda and other countries.

In 2019, 77% of China's total tungsten concentrate imports came from North Korea and 12% from Mongolia. In the first five months of this year, the proportion changed, with 52% from North Korea, 32% from Russia and 10% from Rwanda. The proportion of North Korea and Mongolia has declined, while that of Russia and Rwanda has increased.

Import of raw materials

Output of cemented carbide

In the downstream consumption field of tungsten, cemented carbide accounts for the largest proportion of consumption both at home and abroad. At present, China's cemented carbide accounts for about 60% of all tungsten consumption, which is still a little behind the developed countries, with 70% in the European Union and more than 80% in Japan.

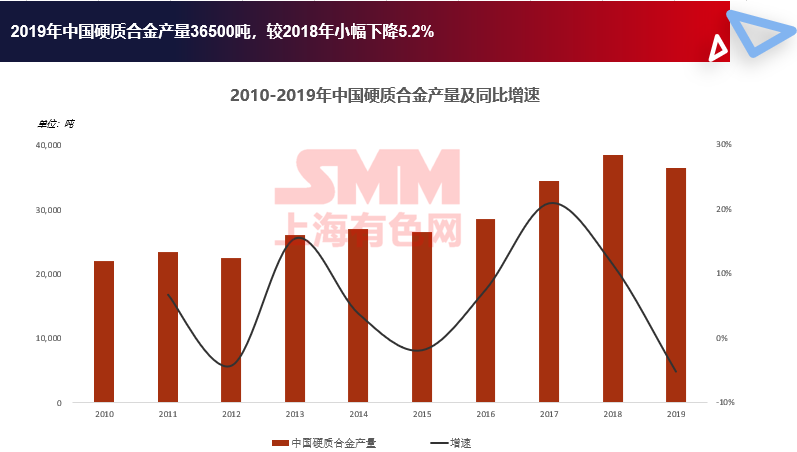

China's cemented carbide production was 22000 tons in 2010, and has since increased slightly year by year, reaching a peak of 38500 tons in 2018, compared with a slight decline of 5.2 per cent in 2019.

The situation this year is of course grim. Demand at home and abroad has shrunk sharply, and the growth rate of cemented carbide production is bound to decline, and will gradually recover with the gradual relief of the epidemic and cost support.

Export of Tungsten products in China

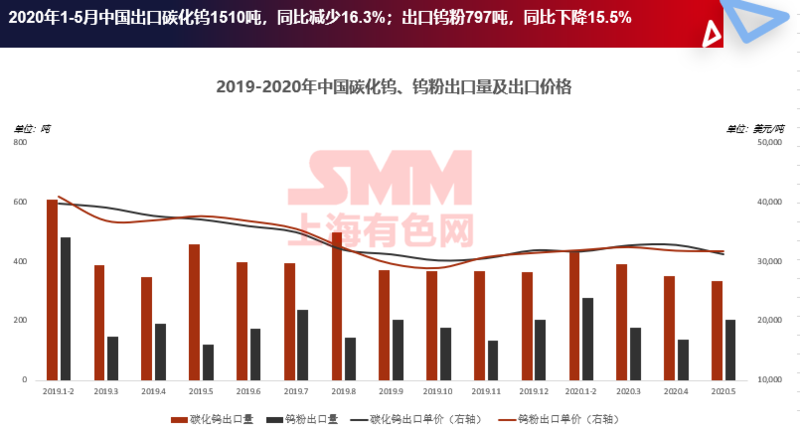

In 2019, China exported a total of 4571 tons of tungsten carbide, down 23 percent from 5952 tons in 2018. The opposite is true for tungsten powder. China exported 2219 tons of tungsten powder in 2019, an increase of 24% compared with 2018.

From January to May 2020, China exported 1510 tons of tungsten carbide, down 16.3 percent from the same period last year, and exported 797 tons of tungsten powder, down 15.5 percent from the same period last year. We understand that the main reason for the decline is that the reduction in demand brought about by the overseas shutdown caused by the epidemic is the biggest and most important factor in the decline in our exports.

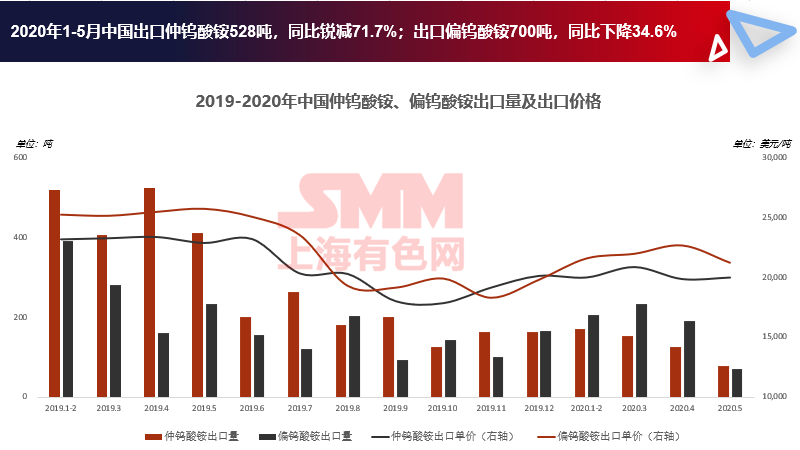

China's exports of APT totaled 3161 tons in 2019, down 44 per cent from 5641 tons in 2018. The case of ammonium metatungstate is the opposite. In 2019, China's exports of ammonium metatungstate totaled 2057 tons, up 27.3 percent from 1616 tons in 2018.

What's the situation this year? From January to May 2020, China exported APT528 tons, a decrease of 72 per cent compared with the same period last year. Exports of ammonium metatungstate were 700 tons, down 35 percent from 1070 tons in the same period last year.

China exported 3335 tons of blue tungsten in 2019, down 51 per cent from 6777 tons in 2018. Similarly, China exported 4358 tons of tungsten trioxide in 2019, down 41 per cent from 7376 tons in 2018.

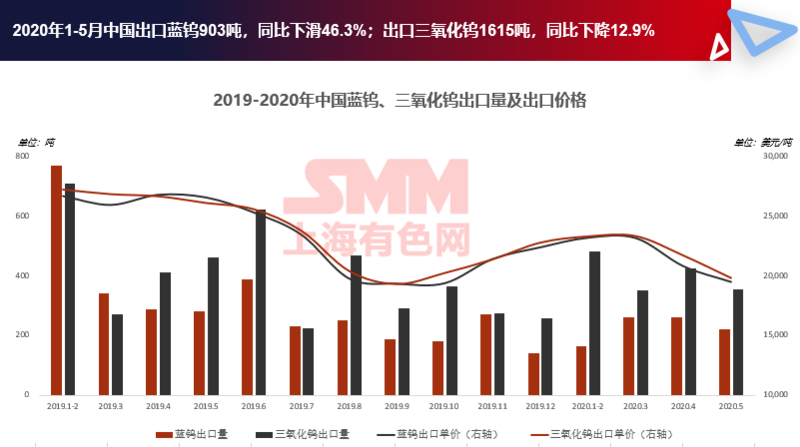

From January to May this year, the export volume of blue tungsten was 903 tons, a decrease of 46% compared with the same period last year. The export volume of tungsten trioxide was 1615 tons, a decrease of 13% compared with the same period last year.

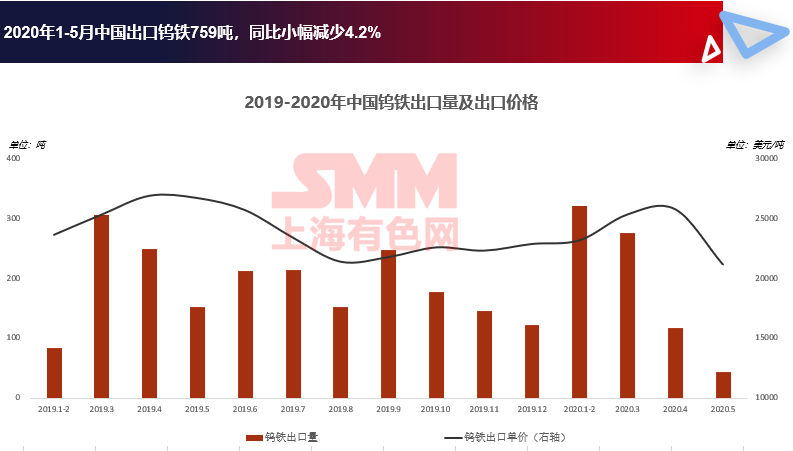

Unlike products such as APT, tungsten powder and tungsten carbide, China exported a total of 759 tons of ferrotungsten from January to May this year, down only 4 per cent from 792tons in the same period last year. According to more detailed data, ferrotungsten exports increased by 53% in the first quarter of this year compared with the first quarter of 2019. This is because after the domestic outbreak in January, major overseas ferrotungsten importers, such as Japan and the Netherlands, worried that China's exports would be affected by the epidemic and increased their orders in the first quarter to meet the needs of later production. Therefore, it can also be seen from the picture that our export volume increased substantially in the first quarter of this year, and began to decline in the second quarter.

Above, we reviewed the domestic export of tungsten products from last year to this year. It can be seen that no matter what kind of products are affected by the epidemic to varying degrees this year, the export volume has been reduced, which is a test of our domestic tungsten consumption capacity.

"Click to view the SMM tungsten industry chain database

Macro environment

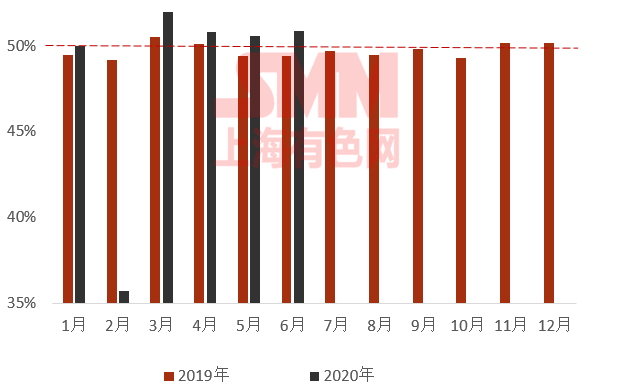

According to the National Bureau of Statistics, the official manufacturing PMI in June this year was 50.9%, up 0.3% from the previous value, and remained above the rise and fall line for four consecutive months, that is, above the dotted line on the left. This shows that China's economy continues to improve. Judging from the sub-index, the production index rose 0.9 percentage points to 53.9%, and the new orders index rebounded 0.5 percentage points to 51.4%, indicating that demand is gradually recovering. New export orders 42.6, up 7.3 percentage points from the previous value, rebounded by a large extent. On the one hand, the expectation of a rebound in external demand brought about by the resumption of work in Europe may have increased, but on the other hand, it is still significantly lower than the rise and fall line.

Purchasing Manager Index of China's Manufacturing Industry from 2019 to 2020

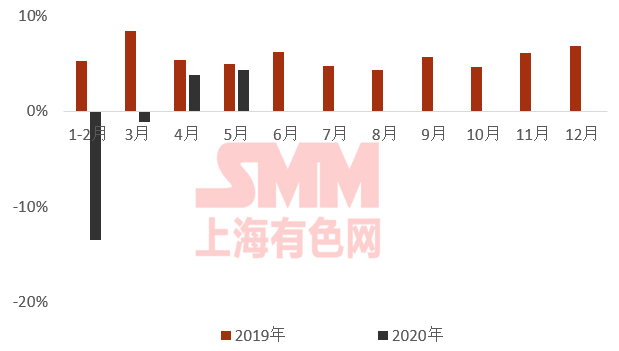

Also according to the statistics of the Bureau of Statistics, the added value of industries above scale increased by 4.4% in May 2020 compared with the same period last year, 0.5 percentage point faster than the previous month, and continued to pick up on the basis of turning negative to positive in April. From the picture, we can see that from last year to this year, only the January-February data of this year is negative, which is the most serious period of the epidemic in our country.

Year-on-year growth rate of industrial added value above scale in China from 2019 to 2020

Since the beginning of May, the resumption of work and production has been further promoted, and industrial production has been accelerated. The production of most industries and products continued to recover, and new products maintained rapid growth. In addition, the growth of the equipment manufacturing industry continued to accelerate, and the growth of infrastructure-related products was good.

Generally speaking, fiscal policy will be gradually launched in the second half of the year, special treasury bonds will be launched, the issuance of special bonds will be accelerated, and infrastructure support is expected to continue to strengthen to boost investment demand. In terms of risks, overseas demand is still facing uncertainty. On the one hand, Sino-US relations are on the one hand. The epidemic in the United States has not yet stabilized and rebounded. The number of new cases in a single day has reached a record high, and the uncertainty is strong, which is expected to have a certain impact on external demand. Export-oriented enterprises will still be under pressure.

Today is the 15th, and the annual rate of China's second-quarter GDP will be released tomorrow, July 16. This value was-6.8% in the first quarter. At present, almost all institutions predict that China's GDP will return to positive growth in the second quarter.

Review of China's Tungsten Industry Policy and Major events from 2018 to 2020

In August 2018, the United States imposed a 25% tariff on 16 billion US dollars of Chinese exports to the United States. In the same period, China counteracted by reciprocity.

In May 2019, ten enterprises of the presidium of the China Tungsten Association agreed to jointly maintain the supply order of the tungsten raw material market and reduce the output of tungsten concentrate by no less than 10% in 2019.

In September 2019, Mashan Tungsten Co., Ltd., a wholly-owned subsidiary of Vietnam Mashan Resources Company, acquired Germany's Sitco tungsten business; after 135rounds of bidding, 28300 tons of APT seized and auctioned by Kunming Pan-Asia Nonferrous Metals Exchange was successfully bid by global mining giant Luoyang Molybdenum Industry for 3.268 billion yuan.

In November 2019, Minmetals Tungsten Industry Co., Ltd. successfully sold all 431.95 tons of tungsten bars involved in the Pan-Asia case for 65.9564 million yuan.

In December 2019, the tariff Commission of the State Council: from January 1, 2020, the provisional import rates of tungsten scrap and niobium scrap will be abolished, and the most-favored-nation tax rate will be resumed; the Ministry of Commerce announced the list of state-owned enterprises exporting tungsten and tungsten products in 202021, with a total of 16 enterprises.

In May 2020, Ganzhou City put forward and drafted the "Code for the Construction of Green Tungsten Mine" jointly with the Zhengzhou Research Institute of the Chinese Academy of Sciences, which will be implemented from May 1, 2020; Minister of Ecology and Environment: the second round of central environmental protection inspectors will be launched this year.

Price forecast

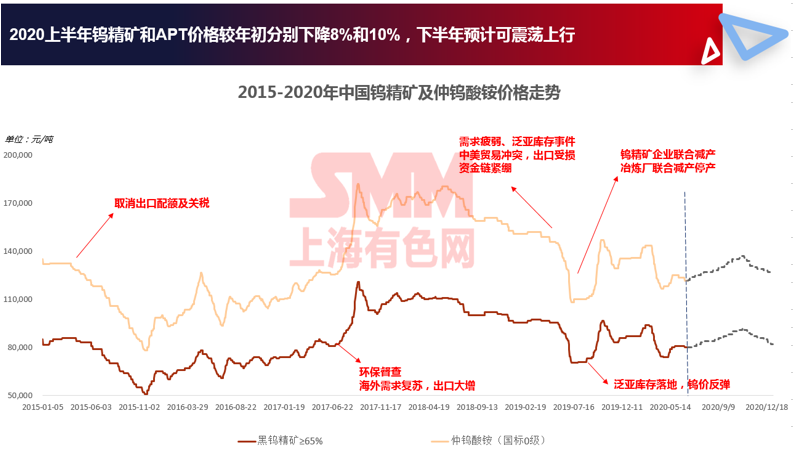

Affected by the abolition of export quotas and tariffs from 2014 to 2015, tungsten prices fell to the cost line. Then, after the combined influence of industry self-discipline from 2016 to 2017, enterprise production limit quotation, national collection and storage, and environmental protection supervision, the price of tungsten concentrate regained its position of 100000 yuan / ton in 17 years.

In 2018, the overall tungsten price level is high, the enthusiasm of enterprises to start work is high, and the production capacity of APT is released massively; but at the same time, the consumption capacity of the back-end is still weak, and trade frictions between China and the United States also begin to affect exports, so many factors are superimposed. The domestic tungsten market in 2019 is in a state of significant surplus. Prices continue to fall, smelters hang upside down under great pressure, the capital side of the industry is tight, and it is difficult for tungsten enterprises to survive. So in May, the leading tungsten concentrate enterprises decided to reduce production by no less than 10%, and 17 smelters in Ganzhou also jointly proposed to limit production and stop production. In September, after the pan-sub-tungsten product inventory auction, the greatest uncertainty to suppress the rise in tungsten prices was eliminated, and tungsten prices began to pick up.

Affected by epidemic factors at home and abroad this year, the performance of domestic consumption and exports is not satisfactory, and prices fell in the first half of the year. By the end of June, tungsten concentrate prices were down 8% from the beginning of the year and apt prices were down 10% from the beginning of the year.

We believe that after repeatedly bottoming out prices in June, prices accumulated upward momentum in July, and with the recovery of consumption in downstream areas such as cemented carbide, the whole will fluctuate upward in a certain space in the second half of the year. The mainstream operating space of tungsten concentrate is between 80-90 thousand yuan / ton, and the main operating space of APT is between 12-140000 yuan / ton.

Scan the code to apply to join the SMM industry communication group: