SMM7 March 14: at the 2020 (Fifth) China International Nickel-Cobalt-Lithium Summit Forum and China International New Energy Lithium Materials Conference held by SMM, Qin Jingjing, Chief analyst of Cobalt and Lithium from Shanghai Nonferrous net, gave a keynote speech on the analysis of supply and demand and price trend of the global lithium market from 2020 to 2022 with active policy support.

The change of Lithium City in 2020 under the influence of epidemic situation

Qin Jingjing said that on the supply side, the supply of Australian mines and Argentine salt lakes shrank significantly in the first quarter; on the demand side, car markets in Europe and the United States cut production on a large scale in April, and demand in emerging digital markets such as Africa and India recovered slowly.

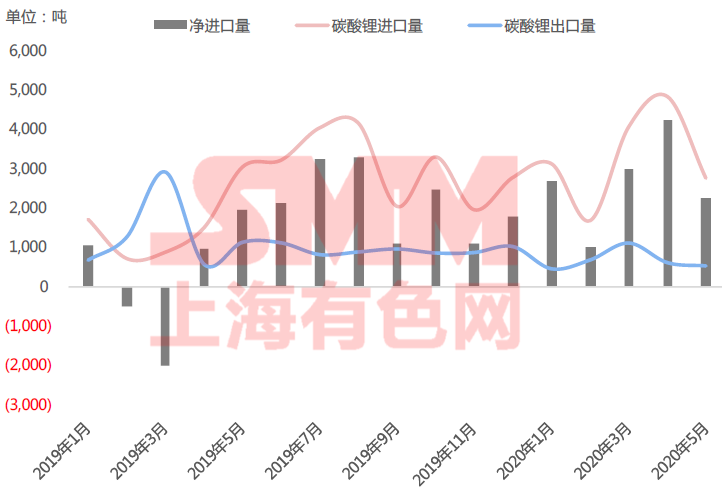

China's export volume of lithium hydroxide, which has become a net importer of lithium carbonate, has been significantly repaired since March.

Since May 2019, with the rapid decline in domestic lithium carbonate prices, the overseas lithium carbonate market began to "destroy orders", and a large number of products poured into the Chinese market; in addition, as the overseas markets are mainly high-nickel models, the demand for lithium carbonate is low, more overseas salt lake enterprises have focused on the Chinese market, and the supply and price of domestic lithium carbonate may continue to face the pressure of overseas lithium imports in the future.

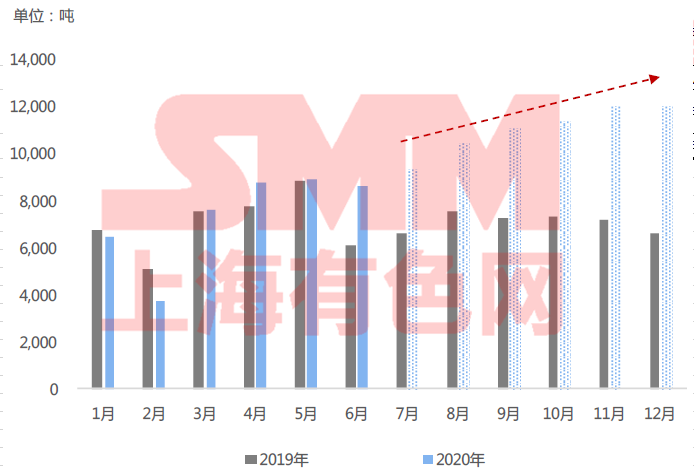

There are two main reasons for the sharp decline in lithium hydroxide exports in the first quarter of 2020: 1, taking into account the Chinese New year holiday, overseas markets have been prepared in advance in the fourth quarter of 2019; 2, the spread of the epidemic has blocked import and export logistics. As the epidemic situation in China, Japan and South Korea was gradually brought under control, the export of lithium hydroxide was obviously repaired in April.

The output of lithium carbonate has recovered rapidly since March and there may be a significant increase in lithium hydroxide in the second half of the year.

Taking into account the cost differences between different raw materials and the trend of lithium carbonate homogenization, the release of lithium carbonate in China in the second half of the year will still mainly come from salt lake brine and lithium mica. SMM estimates that China will produce 170000 tons of lithium carbonate in 2020.

With the release of new lithium hydroxide production lines and optimistic demand expectations for the European car market, SMM expects China's lithium hydroxide production in 2020 to be 110000 tons.

Carding of supply and demand structure and Price Prospect of Lithium Industry in 2020

European countries' new energy stimulus policies continue to increase the trend of electrification in the market.

On May 19th, the European Union proposed to include electric vehicles in the green economy recovery plan, including: 1) promoting a clean energy vehicle procurement plan of 20 billion euros in the next two years, 2) establishing a clean energy vehicle investment fund of 400-60 billion euros, 3) building 2 million new public charging piles by 2025, and 4) exempting zero-emission vehicles from value-added tax.

At present, among the main EU countries selling new energy vehicles, Germany, France, Italy, the Netherlands, Sweden and Spain have VAT rates of 19%, 20%, 22%, 21%, 25% and 21%, respectively. If the VAT exemption program for zero-emission cars is launched, it is expected that most of the benefits will be transferred to the consumer side, driving the retail price of zero-emission vehicles down by about 20%, and the performance-to-price ratio will be significantly improved.

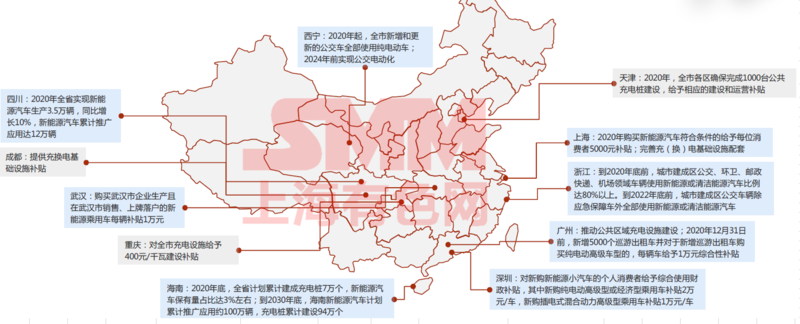

China's new energy subsidy policy continues local policies to provide subsidies or index supplements.

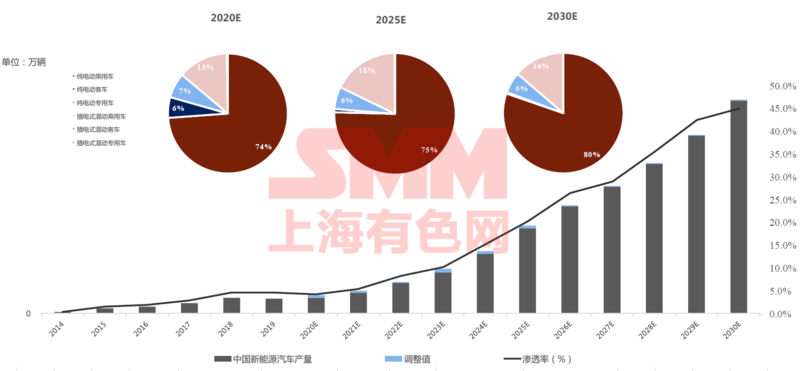

On April 29, 11 departments, including the National Development and Reform Commission and the Ministry of Science and Technology, issued the Circular on several measures to stabilize and expand Automobile consumption, slowing down the decline and pace of subsidies from 2020 to 2022 and speeding up the settlement of subsidy funds. The preferential policy of exemption from vehicle purchase tax for new energy vehicles will be extended until the end of 2022. Qin Jingjing said that by 2025, the competitiveness of new energy vehicles will be significantly improved, accounting for 25% of the total car sales in that year, and by 2030, new energy vehicles will form a competitive advantage in the market, accounting for 40% of the total car sales in that year.

Global supply and demand structure of Lithium Raw Materials in 2020

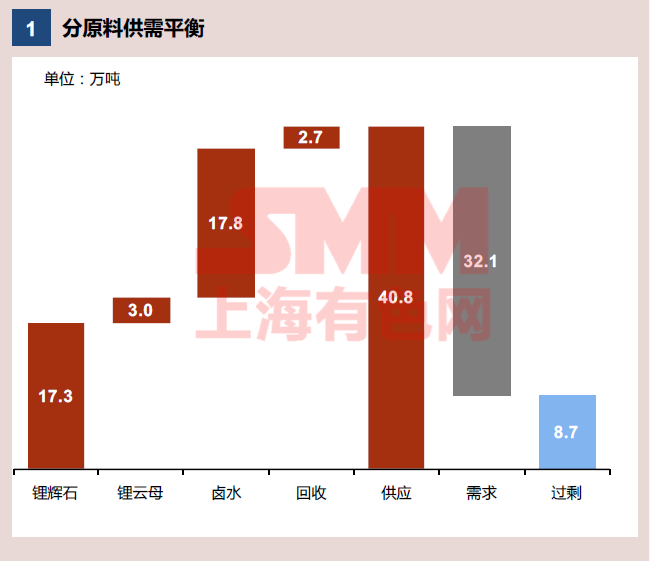

Before 2019, the main raw material of lithium carbonate is spodumene, but salt lake brine and lithium mica develop rapidly because of their cost advantages. SMM predicts that salt lake brine will become the most important lithium raw material in the world by 2020.

The global lithium raw material supply is expected to be 408000 tons in 2020, the LCE, demand is estimated to be 321000 tons, and the LCE, surplus is estimated to be 87000 tons. The lithium-ion battery industry will dominate the demand for lithium raw materials for a long time in the future.

In terms of lithium carbonate, China is expected to have a surplus of 73000 tons of lithium carbonate in 2020, and the lithium-ion battery industry is the main driving force for the growth of lithium carbonate demand.

In terms of lithium hydroxide, the surplus of lithium hydroxide in China is about 7000 tons of LCE, in 2020, and its supply and demand structure is better than that of lithium carbonate.

In terms of electric carbon, the cost of lithium mica enterprises has shifted to the left obviously, and the current battery-grade lithium carbonate market has been oversold.

The main results are as follows: 1) for battery-grade lithium carbonate, salt lake brine has the most obvious advantage of raw material cost;

2) for lithium mica companies that can achieve "one-step" production of battery-grade lithium carbonate, the cost has been greatly reduced. With the development of technology in the future, compared with spodumene, lithium mica will maintain a cost advantage in the lithium carbonate market.

3) spodumene will be mainly used in lithium hydroxide market in the next 5 years.

Long-term Prospect of New Energy vehicle Industry from 2020 to 2030

Qin Jingjing said that in the next 10 years, the compound growth rate of China's new energy vehicle production will be 30%, and the proportion of new energy passenger vehicles will reach 94% in 2030. Ternary battery is the main type of battery in new energy passenger vehicles, and the process of high nickelization in China will be accelerated in the next 10 years.

SMM believes that the removal effect of lithium ore is remarkable, smelting products and domestic ore stocks still need time to digest, and the global lithium raw materials may achieve a balance between supply and demand in 2022.

Scan the code to apply to join the SMM Cobalt and Lithium Industry Exchange Group