The monthly output data of SMM China's basic metals is scheduled to be released around the 8th of each month, aiming at starting from the essence, excavating the real fundamental situation, opening up the illusion of the capital market for people in the industry chain and investors, and more clearly grasping the future trend of the non-ferrous market.

Summary of basic Metal production in China in June 2020

Electrolytic copper

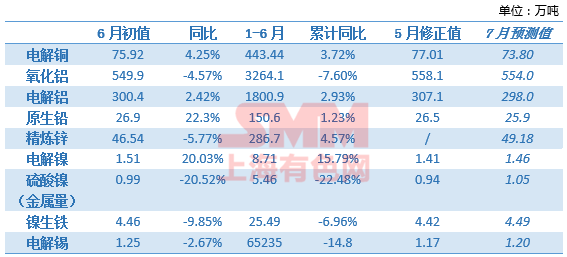

In June 2020, SMM China produced 759200 tons of electrolytic copper, down 1.42% from the previous month and an increase of 4.25% over the same period last year. From January to June, SMM China produced a total of 4.4344 million tons of electrolytic copper, an increase of 3.72 percent over the same period last year. The domestic output of electrolytic copper decreased slightly in June from the previous month, but higher than the expected value in May, mainly due to the delayed maintenance plan of the refinery, and the impact of maintenance in June was less than the expected value. In addition, the domestic supply of crude copper scrap improved in June, and the output of refineries using this part of the raw materials also increased.

In June, the price gap of fine waste continued to widen, domestic scrap copper inventory outflowed, superimposed import arrival improved, domestic crude scrap copper supply increased, and crude copper processing fees rebounded by 250 yuan / ton compared with the previous month. However, the mine end still maintains a tense situation, and the interference to production is still expanding. Due to the overhaul of domestic refineries in July, it is expected that the output of domestic electrolytic copper will drop month-on-month in July.

According to the production plans of various refineries, SMM expects domestic electrolytic copper production in July 2020 to be 738000 tons, down 2.79% from the previous month and 2.28% from the same period last year. By July, cumulative electrolytic copper production was 5.1724 million tons, an increase of 2.82% over the same period last year.

Alumina

According to SMM data, China produced 5.709 million tons of alumina in June (30 days), of which metallurgical grade alumina was 5.499 million tons, and the average daily output of metallurgical grade was 183000 tons, an increase of 1.82% from the previous month and a decrease of 4.57% from the same period last year. In the first half of the year, China's cumulative metallurgical grade alumina output was 32.641 million tons, 7.6% lower than the same period last In the context of the mild rise in alumina prices during the month, the annual operating capacity of alumina in the northern region increased slightly compared with May, and the production reduction of individual alumina plants at the end of the month did not affect the output of that month.

As of the first ten days of July, the operating capacity of metallurgical grade alumina is 66.9 million tons, and the output of metallurgical grade alumina is expected to be 5.54 million tons in July (31 days), with the average daily output rising slightly to 184700 tons. On the whole, China's alumina market is still a month of increasing and reducing production in July. In terms of production reduction, the new materials of Chinalco Huaxing and Shanxi began to produce flexibly at the end of the month, and some alumina plants in southwest China had a roaster maintenance plan in July. In terms of increasing production, Guodian's Shanxi and Henan alumina plants have resumed or plan to resume production. Guodian Investment Sichuan will mass produce alumina products in July, and under the stimulation of rising alumina prices, there may be more reduced production capacity to resume production.

Electrolytic aluminum

According to SMM data, 3.004 million tons of electrolytic aluminum were produced in China in June 2020 (30 days), an increase of 2.42 per cent over the same period last year. By the end of June, the national operating capacity of electrolytic aluminum was 36.76 million tons / year, the completed capacity was 41.23 million tons / year, and the operating rate of national electrolytic aluminum enterprises was 89 percent. The overall operating rate was 0.3 percent higher than that at the end of May 2020. By the end of June, the operating capacity of domestic electrolytic aluminum has increased by 180000 tons / year compared with the end of May. Since June, under the stimulation of high profits, the domestic electrolytic aluminum production capacity has been gradually put into operation, and the monthly output growth rate has accelerated compared with the same period last year.

In the first half of 2020, the cumulative output of domestic electrolytic aluminum was 18.009 million tons, an increase of 2.93% over the same period last year; the cumulative consumption of domestic electrolytic aluminum was 17.69 million tons, and the cumulative year-on-year decline rapidly narrowed to 0.18%. Electrolytic aluminum continued to go to the warehouse in June, mainly due to the temperature at the supply end and the rise in demand for aluminum downstream. In July, the new capacity of electrolytic aluminum in Yunnan, Inner Mongolia and other places will continue to increase, and net imports are expected to increase slightly compared with June. SMM estimates that domestic electrolytic aluminum production in July (31 days) is 3.12 million tons, an increase of 1.79% over the same period last year, and the monthly consumption growth rate will narrow around 6.15% as supply rises and the margin of demand weakens.

Primary lead

In June 2020, China's primary lead output was 269000 tons, up 1.58 percent from the previous month and 22.3 percent from the same period last year. Cumulative output rose 1.23% in the first half of 2020 compared with the same period last year.

According to the investigation and understanding, the overall fluctuation range of lead price in June is not big, but in the middle of the month, due to the cumulative pressure of inventory, lead price once approached the Wanshui mark, the profits of smelting enterprises narrowed, and the enthusiasm for production was limited. During this period, Yunnan Chihong entered the routine maintenance, Henan Yuguang was in the state of replacement production line, coupled with the equipment failures of some enterprises, affecting part of the output contribution; and June was in the middle of the year, some enterprises considered the production and sales volume in the first half of the year, there was a mid-year impulse, at the same time, Chifengshan gold, silver and lead recovered after overhaul, and the overall output continued to increase, which was basically in line with the forecast of the previous report. In addition, the output increased significantly in June compared with the same period last year, mainly due to environmental protection. In June 2019, Henan, a major lead-producing province, due to the aggravation of heavy pollution weather, the local environmental protection department carried out air pollution control work, and large refineries went into overhaul, but this year this factor was basically removed, and the output increased greatly compared with the same period last year.

In addition, looking forward to July, the output of primary lead is expected to show a downward trend. Main reason: in July, Henan Yuguang was still in the state of replacement production line, and the output was further tightened; at the same time, Yunnan Chihong, Hunan Shuikoushan, Jingui and so on entered maintenance, so the overall output decreased. On the other hand, in July, traditional consumption season is expected to boost lead prices one after another, coupled with the lifting of ore import restrictions, imported ore TC rose, and smelting profit repair boosted the production enthusiasm of some refineries. SMM expects primary lead production to drop by about 10,000 tons to 259000 tons in July from the previous month.

Refined zinc

In June 2020, SMM China produced 465400 tons of refined zinc, down 1.85 percent or 8800 tons from the previous month, or 5.77 percent less than the same period last year. From January to June, the total refined zinc production was 2.867 million tons, a cumulative growth rate of 4.57% over the same period last year. In June, the sample alloy output of domestic refining zinc smelters was 66129 tons, down 5.53% from the previous month.

According to SMM research, the domestic refined zinc output in June is slightly lower than the expected value in May. In June, the overhaul and resumption of work and production increase of domestic refining zinc refineries coexist, among which the reasons for the reduction of refining zinc in June are as follows: planned maintenance of refineries in Shaanxi, Hunan and Anhui, in addition, refineries in Yunnan have reduced their daily output due to equipment failures and other factors. In terms of increment, a large refinery in Shaanxi has increased production one after another, while some refineries in Inner Mongolia and Yunnan have resumed production after overhauling.

In July, the stock level of raw materials in domestic smelters continues to rise. at present, the average stock of raw materials is about 28 days, and the shortage of zinc concentrate is regionally divided. on the whole, the shortage of zinc concentrate supply is basically alleviated. Domestic zinc concentrate processing fees are also rising month-on-month. According to SMM's schedule for each refinery in July, the increment mainly comes from the maintenance and restoration of refineries in Yunnan, Anhui, Inner Mongolia and other regions. Although refineries in Gansu and Inner Mongolia also have maintenance, the overall impact is relatively limited. It is expected that domestic refined zinc production will increase by 26400 tons to 491800 tons month-on-month in July.

Refined tin

The output of refined tin in June 2020 was 12490 tons, an increase of 6.51 per cent over May. With the gradual resumption of work abroad, demand has picked up somewhat. Although the downstream orders are not as good as the same period last year, they are better than in the first few months of this year, and the refinery as a whole has increased production. However, the supply of raw materials is still tight, the control of the epidemic in Myanmar has been extended again to July 15, the operating rate of local mining enterprises is at a low level, and the situation of tight supply of raw materials is expected to continue until mid-late July. Due to the shortage of tin ore, processing fees have been depressed, and some smelters have been forced to reduce production due to lack of raw materials. Most refineries say they will maintain stable production next month, and refined tin production is expected to fall to around 12000 tons in July, taking into account the tight end of the mine, the off-season of the industry and the production cuts of some factories.

Electrolytic nickel

In June 2020, the national output of electrolytic nickel was 15100 tons, an increase of 7.32 percent over the previous month and 20.03 percent over the same period last year. The total output in June was 1030 tons higher than that in May. Among them, the output of Gansu smelter increased by nearly 1000 tons over the previous month, returning to the output level of March and April. It is reported that the annual output plan remains unchanged, and there may be a follow-up maintenance period, but the time has not yet been determined. The output of Xinjiang smelter also increased slightly in June compared with the previous month. Jilin smelter is still flat compared with the previous month; Tianjin smelter output gradually recovered this month, this month increased to 260 tons; The output of Shandong smelter has declined somewhat, which is mainly restricted by overseas raw material procurement, while Guangxi smelter continues to suspend electrolytic nickel production.

It is estimated that the national output of electrolytic nickel is expected to be 14600 tons in July 2010. except for the reduction in the production of Shandong smelter, the production of smelters in other regions is still stable according to the original plan, and the domestic output of electrolytic nickel may fall back to the level of May today.

Nickel pig iron

In June 2020, the national output of nickel pig iron increased by 0.81 per cent month-on-month to 44600 nickel tons, down 9.85 per cent from the same period last year. In terms of grade, the output of high nickel iron in June was 37500 nickel tons, an increase of 1.44% over the previous month, while that of low nickel iron was 7100 nickel tons in June, down 2.43% from the previous month. The slight increase in nickel pig iron production in June is mainly related to the release of some new production capacity of high-nickel pig iron. In June, some manufacturers in high-cost areas of Inner Mongolia suspended production or switched to other ferroalloys, but as production in this area gradually decreased, so the decline in June was small, and the release of new capacity was enough to make up for this reduction. In addition, the iron plant maintenance production line resumed and put into operation in the third quarter, so the decline in ferronickel production in the third quarter was limited. The reduction of low nickel pig iron is mainly due to the fact that the natural number of days in June is less than that in May, and it is caused by the overhaul of 200 series stainless steel plants. In July, high-nickel pig iron across the country is expected to continue to increase slightly from the previous month, with an increase of 0.61% to 44900 nickel tons, down 9.85% from the same period last year. The export volume of Philippine nickel mines will rebound sharply in July, the arrival of ironworks nickel mines in Hong Kong will increase, the degree of shortage will be suspended, and the new production capacity of some manufacturers is still being released, so production will continue to increase slightly.

Nickel sulfate

In June 2020, the national output of nickel sulfate was 9900 tons of metal, and the physical amount was 45000 physical tons, an increase of 5.14 percent over the previous month and a decrease of 20.52 percent over the same period last year. Among them, the output of battery grade nickel sulfate is 39800 physical tons, and that of electroplating grade nickel sulfate is 5200 physical tons. The output of nickel sulfate increased slightly month-on-month this month, which is mainly related to the resumption of production in North China No.1 Nickel Sulfate Plant. In June, the order situation of downstream precursors showed no obvious signs of improvement, and the market demand for nickel sulfate was weak; the transaction price of battery-grade nickel sulfate market was still close to the cost or upside down, and some manufacturers chose to do processing for some traders with advantages in raw material cost to maintain factory operation.

It is understood that some of the intermediate products that did not arrive on time in June will arrive in Hong Kong in July, and some nickel sulfate plants will have a more adequate supply of raw materials, and there are plans to increase production slightly, so it is expected that the national output of nickel sulfate will continue to increase slightly in July 2020 from the previous month, an increase of 5.78% to 10500 tons of metal.

Output of metal products in June 2020

Description:

1. The value with * is the correction value, and the italic value is the predicted value.

2. The output of nickel pig iron refers to the data after the physical quantity is converted into metal.

Research methodology

1. Research methods

SMM production research is conducted by professional analysts by telephone, field research and other methods, regular monthly tracking of Chinese metal production enterprises, and to issue China's metal production report.

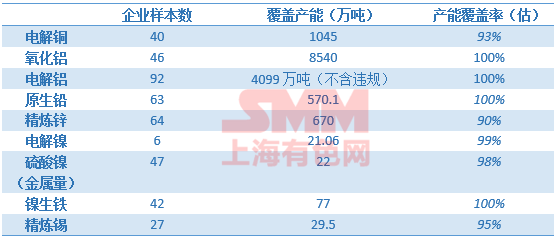

In the process of research, ensure the basic coverage proportion of the sample, and continue to expand; at the same time, consider the capacity scale, regional distribution, the nature of the enterprise and other detailed factors to reasonably select and distribute the sample, so that each sub-data is equally representative.

The production data include the output of last month (initial value), the output of the month before last month (revised) and the production schedule forecast of that month's output. In general, SMM makes less correction to the output, that is, the correction value = the initial value, but still retains the possibility of correction.

It will be released to the public before the 10th of each month through official channels such as SMM official website (www.smm.cn), WeChat subscription account (Nonferrous Today) and mobile phone station (m.smm.cn).

2. Sample introduction

"Click to participate in the second China (Yingtan) Copper Industry Summit Forum and the 15th China International Copper Industry chain Summit"

Scan the code to sign up for the summit or apply to join the SMM industry exchange group: