SHANGHAI, Apr 27 (SMM) – SMM surveyed 41 major aluminium processors in 12 provinces and found that their average operating rate remained largely flat from a week ago at 77.9% last week. Aside from robust demand for construction materials, aluminium plate/sheet and strip producers in Henan province reported a surge in new orders from the construction and medical sectors. Stockpiling by traders and distributors also contributed to higher orders, but this is unlikely to sustain. Notably, aluminium billet producers continued to replace aluminium scrap with primary aluminium amid strong demand and sharply rising processing fees.

Overall operating rates are likely to remain largely stable this week as the negative impact from weaker export orders will not be felt until May.

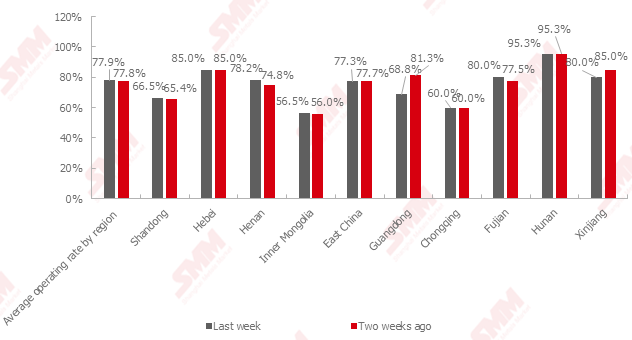

Operating rates at major aluminium processors by region (updated on April 24)

Source: SMM

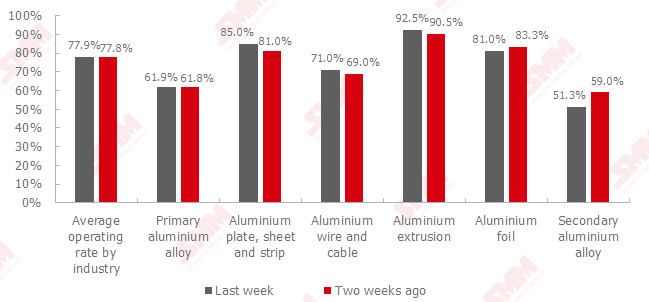

Operating rates at major aluminium processors by industry (updated on April 24)

Source: SMM

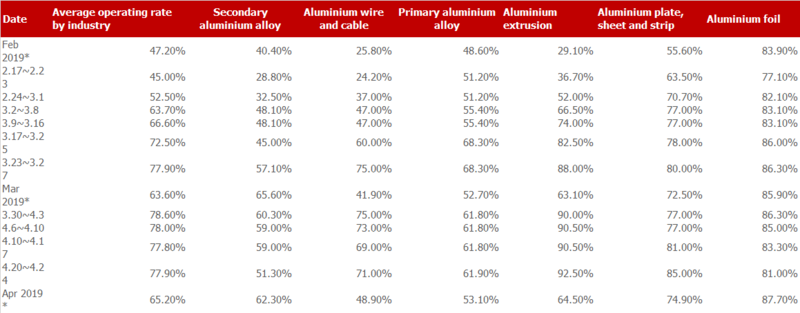

Weekly operating rates at major aluminium processors by industry

Source: SMM

Note: * refers to monthly operating rates.

Aluminium extrusion: Operating rates at aluminium extrusion producers remained stable. Extrusion consumption was mostly driven by domestic buyers, with exports accounting for a relatively small share. Demand for construction extrusion has been strong since the end of March, while strong demand from domestic rail transport sector and subsidies in the photovoltaic industry have partly made up for decline in export orders for industrial extrusion. Some extrusion producers began to raise processing fees, suspend taking new orders and adjust delivery time in response to recent surge in aluminium billet processing fees. Brisk orders from construction sector are expected to last until mid-May. Large producers are likely to report stable orders, while smaller producers may face uncertainties.

Aluminium plate/sheet and strip: Operating rates at large aluminium plate/sheet and strip producers edger higher from a week ago. Hampered exports prompted producers to actively develop domestic market and adjust product portfolios. Most of the large producers in Henan reported improving orders, particularly driven by construction and medical apparatus sectors, while demand from automobile and packaging sectors remained sluggish. Some traders and distributors stockpiled actively following recent rise in aluminium prices, but this may be unsustainable.

Aluminium foil: Operating rates at aluminium foil producers continued to decline as lower new orders led to product restructuring and industry reshuffling. Weaker export orders drove producers to focus on the domestic market. The impact of COVID-19 on end-user sectors also had ripple effects to aluminium foil prices Air-conditioner foil producers were hit the hardest, as weaker demand has caused processing fees of air-conditioner foil to decline 10-14%. This drove air-conditioner foil producers to clear inventories while shifting their production toward sectors with high value-added and strong demand, such as battery foil and pharmacutical foil. Pharmacutical foil gained favour amid COVID-19. Operating rates at electronics foil producers fell slightly. Exports of food foil to Europe and the US were little affected. Hot sealing foil began to enter the high season. Current orders could allow production to sustain through June 15-20.

Aluminium wire and cable: Operating rates at large aluminium wire and cable producers remained largely stable. Current orders are mostly backlog orders received before the Chinese New Year. A few producers said sufficient orders from ultra-high voltage projects that they received at the end of last year would allow them to produce through August. Export orders remained sluggish, but accounted for a small proportion. Operating rates are likely to remain stable in the next two weeks, but may slowly rise with the gradual resumptions of power grid projects.

Secondary aluminium alloy: Operating rates at secondary aluminium alloy producers declined 7.8 percentage points as tight aluminium scrap supply and concerns about orders in May prompted some producers to reduce output. More taint, a type of aluminium scrap with aluminium content of at least 98%, flowed to aluminium billet (for use after being re-melted) producers amid rising processing fees of aluminium billets, which further tightened raw material supply for secondary aluminium producers. A lack of orders in May and raw material issues are likely to continue to weigh on operating rates.

Producers of aluminium billet (for use after being re-melted) have chosen primary aluminium as the main ingredient as demand was strong while processing fees rose steadily. Primary aluminium is expected to continue to replace aluminium scrap, given strong demand for aluminium billets.

Primary aluminium alloy: Operating rates at major primary aluminium alloy producers remained little changed at 61.9%. Orders at producers that cut output flowed to major competitors. As some aluminium wheel plants plan to take 10 days off for the Labour Day holidays, operating rates at major primary aluminium alloy producers are unlikely to recover significantly in May.