SHANGHAI, Apr 20 (SMM) – SMM surveyed 41 major aluminium processors in 12 provinces and found that their average operating rate remained largely flat from a week ago at 77.8% last week. Construction extrusion producers are operating close to full capacity and their operating rates will probably remain largely stable. Overall orders in other processing segments hardly increased, except for brisk orders from construction and medical fields.

Overall operating rates are likely to fall slightly this week due to concerns over export orders in May.

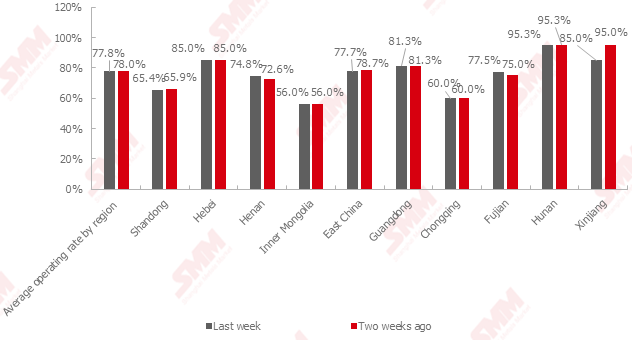

Operating rates at major aluminium processors by region (updated on April 17)

Source: SMM

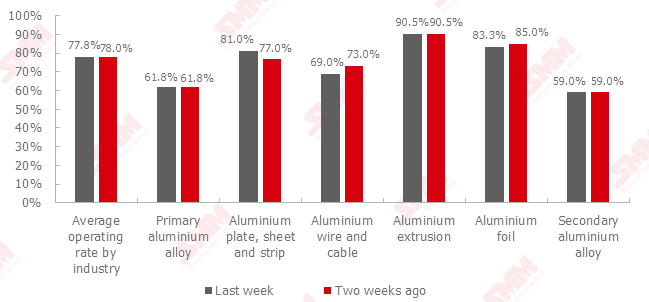

Operating rates at major aluminium processors by industry (updated on April 17)

Source: SMM

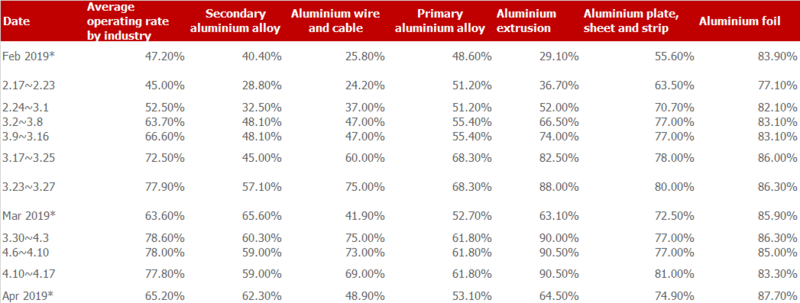

Weekly operating rates at major aluminium processors by industry

Source: SMM

Note: * refers to monthly operating rates.

Aluminium extrusion: Operating rates at aluminium extrusion producers remained stable, with construction extrusion outperforming industrial extrusion. Orders remained stable at large producers, but were weak at small and medium-scale producers. The negative impact on exports from COVID-19 lingered on the spot markets. Raw material stocks at extrusion producers increased and were sufficient for several months at a few producers. Inventory pressure of finished products has eased slightly after producers delivered backlog orders. Operating rates are expected to remain largely stable in April.

Aluminium plate/sheet and strip: Operating rates at large aluminium plate/sheet and strip producers edger higher from a week ago. Backlog orders allowed producers to maintain stable production. Orders from construction and medical fields were relatively strong, while orders from automobile and packaging sectors remained weak. The escalation of COVID-19 overseas continued to take a toll on exports and kept finished product inventories high at producers. Large plate/sheet and strip producers either sourced raw materials from their parent companies or bought from the market as needed. Producers are worried about the orders in May and June after backlog orders are delivered.

Aluminium foil: Operating rates at aluminium foil producers dropped 1.7 percentage points from the previous week as overseas demand declined about one third, even as domestic demand improved slightly. Exports to Southeast Asia have halted. Exports to Europe and the US were slightly better than to Southeast Asia, but declined from the same period last year. Weak orders and thin profits prompted air-conditioner foil producers to shift to other products. Robust orders for pharmaceutical foil incentivised producers to run at full capacity. Weaker exports forced electronics and packaging foil producers to reduce operating rates. Operating rates at aluminium foil producers are likely to continue to decrease slightly in late April as the outbreak of COVID-19 in Europe and the US has not shown signs of improving.

Aluminium wire and cable: Operating rates at large aluminium wire and cable producers dropped as weaker exports, especially to Central Asia, Western Asia and South America where ports were locked down, disrupted shipments. On-hand domestic orders were mostly received last year, with limited new orders so far this year. State Grid did not issue a large number of tenders while construction of power distribution projects remained slow. Producers have a bearish outlook on orders in the first half of the year.

Secondary aluminium alloy: Operating rates at large secondary aluminium alloy producers remained stable. Current orders are mostly from domestic clients, with export orders still sluggish. The price spread between primary aluminum and ADC12 secondary aluminum narrowed amid rising aluminum prices, which made it uneconomical to use primary metal as a substitute for aluminum scrap. Aluminum scrap suppliers held back cargoes after aluminum prices rose, tightening raw material supply for secondary aluminium producers. Export-oriented producers lowered prices to win clients from domestic markets. Cost support encouraged secondary aluminium producers to raise offers slightly last Friday. However, die-castings producers will hardly accept higher raw material prices if recovery of automobile consumption remains slow, which will probably force secondary aluminium producers to reduce output.

Primary aluminium alloy: Operating rates at the top five primary aluminium alloy producers remained unchanged at 61.8% due to stable orders. Producers maintained stable production to fulfill monthly orders. A few producers whose finished product inventories declined planned to increase output next month. SMM sees little possibility of significant increase in operating rates at primary aluminium alloy producers in the short term, in light of weak orders and low operating rates at aluminum wheel plants.