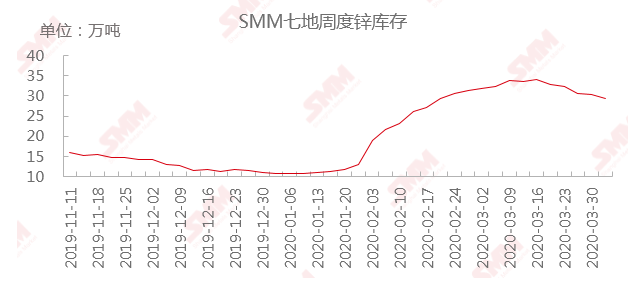

SMM4, March 3: since the return of the Spring Festival holiday, affected by the domestic epidemic, enterprises can not resume work, zinc ingot inventory all the way up. In March, the domestic epidemic situation was effectively controlled, zinc ingot inventory also appeared an inflection point. From March 16, the zinc city entered the process of going to the warehouse. According to SMM research, as of April 3, the total inventory of zinc ingots in SIM7 was 292600 tons, down 11400 tons from March 30 and 14400 tons from March 27.

"Click to view the SMM zinc industry chain database

The main reasons for the decline in zinc ingot stocks are as follows:

On the one hand, the domestic epidemic situation has been effectively controlled, downstream enterprises have basically returned to work, and terminal demand has gradually improved. In galvanizing, the operating rate of large and small enterprises has differentiated. Among them, the operating rate of large galvanizing plants has gradually risen to about 80%, and some enterprises will even increase to full capacity, but the operating rate of small galvanizing plants remains low because of limited orders. On the whole, due to the high black inventory, the corresponding zinc ingot inventory is also maintained at a higher level, the overall drive to the warehouse; galvanized structural parts concentrated in the large galvanized pipe factory order is better, the stock is also more. Die casting zinc alloy, according to SMM research, the current terminal domestic demand has been restored, superimposed in mid-March zinc prices plummeted, terminal orders surged, for the follow-up orders in April there is an obvious overdraft, superimposed downstream enterprises low price replenishment, the overall inventory of raw materials and finished products are still high, superimposed foreign trade orders mostly fade, die casting zinc alloy enterprises are expected to order in April is not optimistic. Zinc oxide industry due to the drag of the automotive industry, the operating rate has not yet returned to the previous level, enterprises are mainly driven by low-cost reserves to go to the warehouse.

At present, the domestic consumer side is still greatly affected by the setback in exports, external demand is bleak, although domestic demand has recovered, but the overall concentration in large and medium-sized enterprises. In April, tight supply at the end of the mine has led to production cuts at some smelters, but the recovery of Baiyin and Chihong has partially offset the reduction, and subsequent attention may still need to be paid to the reduction of domestic processing fees and the supply of raw materials to smelters. If the supply of follow-up raw materials continues to be tight, it may lead to more production cuts in smelters.