Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

Language:

Language:

SHANGHAI, Mar 12 (SMM) – It has been more than 3 months after China is hit by the COVID-19 pandemic, and restrictions on industrial activities and transportation were the harshest in February. During this period, SMM is continuously tracking market recovery on the metals market. Please see our detailed findings for the nonferrous metals sector below.

We will keep you posted on the latest happenings via our website www.metal.com and our social media channels on Linkedin and Twitter.

Please register for our webinars in March as we continue to connect you with the latest happening in the China ferrous and nonferrous metals market.

The next session is happening on Wednesday March 18, 5pm CST, where we present to you a macro update of the resumption of metals industry as China recovers gradually from COVID-19 , with a deep-dive in the ferrous metals markets.

Book your slots now. https://attendee.gotowebinar.com/register/3230865845340759563

Nonferrous raw materials supply

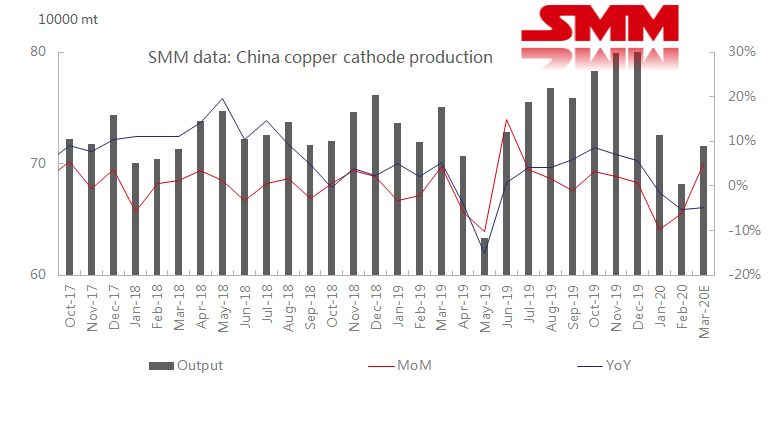

Copper: SMM data showed that China produced 683,100 mt of copper cathode last month, down 5.9% from January and 5.07% from February 2019. Transport curbs significantly affected logistics in China in February, disrupting deliveries of copper cathode and sulphuric acid from smelters and prompting smelters that did not suspend production during the Chinese New Year holiday to trim output last month.

In late February, the Chinese authorities gradually removed curbs on trans-regional transportation, which helped to slow inventory growth of sulphuric acid and eased pressure on copper smelters.

Production of copper cathode in China is estimated to rebound in March, increasing 4.74% from February to 715,500 mt to produce a year-over-year decline of 2.54%. This will bring production in the first three months of 2020 to 2.12 million mt, down 3.73% year on year.

Some smelters are recovering their production, while slower-than-expected demand recovery, high inventories and lingering sulphuric acid woes force some smelters to extend maintenance into this month, keeping production from recovering to normal levels.

Primary lead: Smelters of primary lead in China stepped up production this week on the back of high treatment charges (TCs) for lead concentrate and the recovery of logistics.

SMM data showed that primary lead output in China declined greater than expected in February on the COVID-19 impact, falling more than 40,000 mt from January to 214,000 mt, down 16.6% on the month and 4.9% on the year. Most lead smelters delayed their resumption after the Chinese New Year holiday. Major producers such as Hunan Yuteng and Yunnan Zhenxing also extended their suspension after maintenance and did not recover operations until late-February.

Some smelters cut their scheduled output for February or carried out overhauls on facilities as post-holiday transportation curbs led to supply disruption of raw materials and inventory buildup of lead ingot and by-product sulphuric acid.

Secondary lead: Major secondary lead producers in China have resumed operations on the back of signs of containment of COVID-19 in China, but tight battery scrap supply deterred them from stepping up operations. Trades of battery scrap were light in regions like Tianjin and Hebei, while better in Jiangsu, Zhejiang, Shandong, Jiangxi and other regions.

Refined zinc: China’s zinc output declined in February as sulphuric acid inventory woes, raw material supply shortages and manpower issues forced smelters to slash production.

About 453,000 mt of refined zinc was produced in China last month, down 14.3% from the revised output of 528,500 mt in January but up 7.75% from February 2019. Zinc capacity which was covered in the SMM survey remained unchanged at 6.09 million mt on an annualised basis.

Transport curbs aimed at containing the COVID-19 outbreak crippled road transportation before mid-February, leading to storage capacity shortages for the byproduct sulphuric acid at large and medium-scale zinc smelters who did not suspend production during the CNY holiday. Some large smelters in Shaanxi, Inner Mongolia and other regions had to curtail production last month.

Some smelters scaled back production last month due to tight supply of raw materials as logistical constraints kept them from replenishing their stocks which remained at on-demand levels ahead of the CNY holiday.

Meanwhile, delayed return of workers forced smelters in Hunan, Yunnan and other regions to remain shut for a longer period of time. Shorter working days in February also contributed to lower monthly production figures.

Nickel pig iron (NPI): The virus impact on domestic production of NPI has faded in March, with the operating rates of NPI plants rising to 65.52% from 63.99% a month earlier, showed the latest SMM survey.

Last month, some producers in Inner Mongolia and Liaoning were compelled to reduce output or bring forward maintenance due to limited availability of adjuvant amid a coronavirus outbreak. This was estimated to impact NPI production by 20,000-30,000 mt in physical volumes in February.

SMM expects NPI production in China to recover in March on the easing impact of coronavirus on adjuvant materials supply. Domestic NPI output is estimated to rise 2.36% from February to 43,100 mt in Ni content in March, with production of high-grade materials increasing 1.73% to 36,400 mt in Ni content, while that of low-grade materials expanding 6.02% to 6,700 mt in Ni content.

However, NPI prices will remain under pressure in the short term as elevated stainless steel inventories weigh on prices and it may still take two months for the destocking.

Refined nickel: Production of refined nickel in China felt an overall smaller impact from the pandemic outbreak, as the virus was contained on time in some major production areas and smelters mostly maintained normal operations during the CNY holiday. Nickel smelters in Gansu and Xinjiang are operating as previously planned, while those in Shandong and Tianjin have swung to low gear. Overall refined nickel output in February limitedly declined from January.

Smelters in Guangxi planned to resume production of refined nickel in the fourth quarter, and smelters in Jilin have only generated small amounts of refined nickel products.

SMM expects the average operating rates at refined nickel smelters to rise to 70% in March, from 61% in February.

In the overseas market, refined nickel production in Canada, Russia, South Africa, Norway where majority of the capacity is located has been impacted little by the COVID-19 outbreak, and no output cut schedule was heard. Meanwhile, nickel inventories across LME-listed warehouses are currently at high levels.

Cobalt salts: Producers of cobalt salts in Guangdong, Jiangxi, Shanghai and Hunan mostly maintained operations or restarted production in early February, given limited impact from COVID-19. Some plants in Jiangxi, Jiangsu and Zhejiang reopened in the second half of February due to logistics restrictions and shortage of raw materials. Those producers kept operating rates at low levels for February, and have resumed 50-60% of capacity so far.

Several cobalt salt producers in Sichuan, Zhejiang, Jiangxi, Shandong and Guangdong recovered production in early March, and are gradually raising operating rates. Producers in Hubei will officially resume operations in mid-March. The operating rates of Chinese cobalt salts plants are expected to rise to normal levels in March, from only 30-40% in February. As of March 11, the rates stood at 50-60% for most cobalt salts mills.

Lithium salts: Smelters in Jiangxi and Sichuan reduced production in February due to the virus impact. Output in Qinghai, areas that felt a limited impact from the virus, was also lower last month as producers usually schedule output cut on weather issues in winter and some plants scaled back production on elevated inventories.

In February, production of lithium carbonate declined the most in Jiangxi, by 68.1% from a month earlier, SMM assessed. Lithium carbonate production in Qinghai was estimated to fall 17.9% last month, while output in Sichuan shrank only 10% given the continuous production of a major mill over the Chinese New Year holiday.

Smelters in different areas had resumed operations in the second half of February, with the operating rates likely improving markedly in March. SMM expects the average rate to rise to 80% in the second half of March.

Cobalt (II, III) oxide, ternary precursor: Producers of cobalt (II, III) oxide were limitedly hit by the COVID-19 given a high concentration ratio of the industry. Operating rates of most cobalt (II, III) oxide plants have reached 60-70% as of March 11, and the rate will remain buoyant in March. For most producers of ternary precursor, the operating rates have climbed to 60%, with some major producers lifting rates to 70-80%.

Some producers of cobalt (II, III) oxide and ternary precursor in Guizhou, Zhejiang, Gansu and Hunan maintained operations during the CNY holiday and have lowered their operating rates. Producers in most areas restarted work in early February, and some plants in Zhejiang, Ningxia and Jiangxi only recovered in the second half of February. Producers in Hubei are scheduled to return in mid-March.

SMM research found that inventories of cobalt (II, III) oxide piled up in February due to sluggish purchases by downstream producers of batteries and lithium cobalt oxide (LCO), who operated at low rates last month.

Refined tin: Upstream smelters have restarted production, but tin ore supply constraints are likely to force some smelters to slightly scale back operations. Operating rates across tin smelters in China are expected to recover to 43.8% in March.

Demand for nonferrous metals

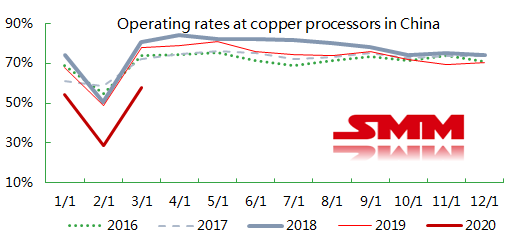

Copper: Operating rates across Chinese copper processors averaged 28.95% in February, down 25.33 percentage points month on month and 19.8 percentage points year on year, SMM survey showed. Some producers in east and south China (production and sales hubs of copper semis) resumed on February 10, but production was slow due to trans-provincial transport restrictions and 14-day self-quarantine for migrant workers.

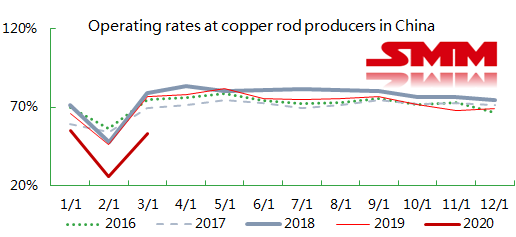

Copper rod, which accounted for more than half of copper products, was the worst performer among copper processing, as delayed restarts of the major consumers —power and real estate projects depressed demand for copper rod, wire and cable. A plunge in copper rod producer operating rates pushed overall production of copper products lower in February.

The average operating rate across Chinese copper processors is expected to increase 29 percentage points from February to 57.96% in March, 19.83 percentage points lower than the same month of 2019. Copper processors have recovered their operations to about 80% of regular levels, following the containment of the pandemic in China, and some plants are expected to recover to normal levels in late March.

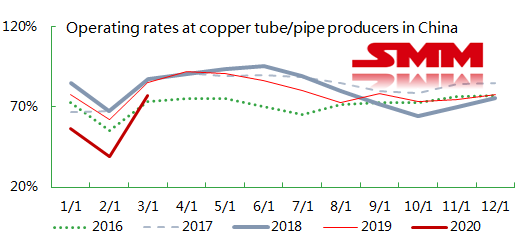

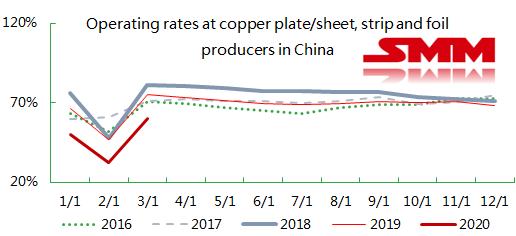

In March, operating rates at copper rod producers are expected to increase 27.71 percentage points to 53.58%, to produce a year-over-year decline of 23.6 percentage points; operating rates at copper pipe/tube producers are expected to increase 37.83 percentage points month on month but decrease 8.35 percentage points year on year to 76.89%; operating rates at copper plate/sheet, strip and foil producers are expected to increase 27.21 percentage points month on month but decrease 15.63 percentage points year on year to 59.82%.

The resumption of copper processors in east and south China progressed faster in other Chinese regions following the recovery of logistics, but the virus impact extended into the first half of this month, leading to a sharp decline in the monthly copper processor operating rates from March 2019. Concerns about demand which is not expected to fully recover until at least April, currently are the biggest drag on production of copper products.

Orders for copper rods recovered slower than those for copper plates/sheets, strips and tubes/pipes, as power and construction resumed work slower than home appliances. State grid operators tightened their investment from last year. That, coupled with the fallout from the coronavirus, casts a shadow over the power sector this year and dampens the prospects of copper consumption in copper rods. While lower copper prices boosted orders, the absence of a substantial recovery in consumption slowed deliveries of copper products to end-users, growing inventories of finished goods at copper processors and affecting production at some plants.

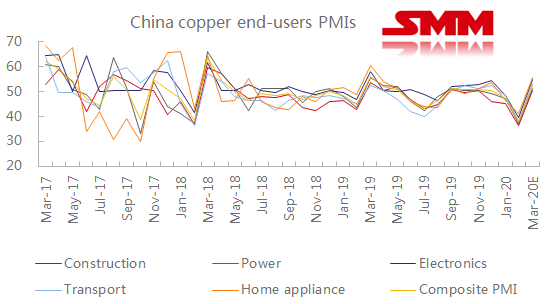

SMM purchasing managers' index (PMI) for China copper downstream, which gives an snapshot of operating conditions in construction, power, electronics, transport and home appliance sectors, dropped to 37.97 in February, below the 50-mark that separates growth from contraction.

Most of the property, state grid projects in China remained closed in February, as most regions required construction sites not to resume work earlier than March 1. The COVID-19 also dealt a blow to the auto industry. Data from the China Passenger Car Association (CPCA) showed that production and sales of sedans, multi-purpose vehicles (MPVs) and sport utility vehicles (SUVs) in China in February dropped 80.6% and 78.5% from a year earlier, respectively. Subdued consumption, meanwhile, kept large-scale Chinese home appliance producers from ramping up capacity. Home appliance producers are also beleaguered by high inventories and the US-China trade war which has hit exports.

The copper downstream PMI is expected to increase 14.46 points to 52.43 in March, returning to expansionary territory, as factories and construction sites resumed work. The broad recovery across end-users is expected in late March to April at the earliest, as downstream consumption is still recovering and as cash flow issues at small and medium enterprises will slow new orders.

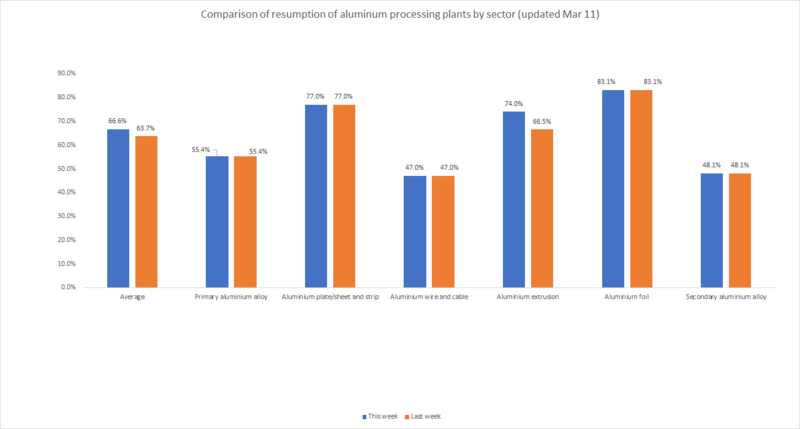

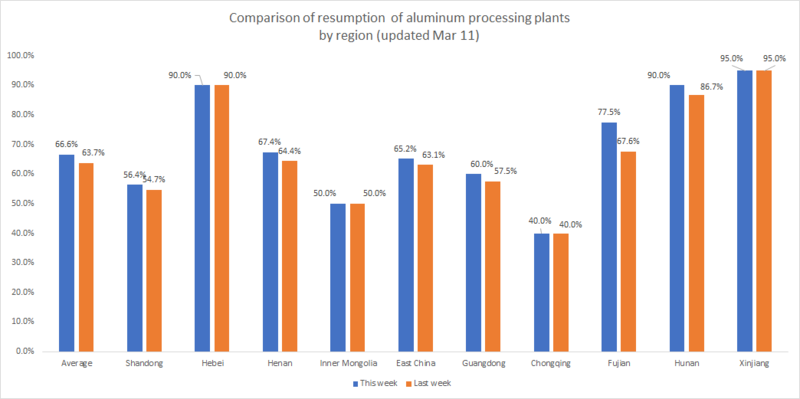

Aluminium processing: Weak orders and sluggish end-user consumption have surpassed COVID-19 containment measures to be the top headwinds against production at aluminium processors, according to SMM’s weekly survey across 41 aluminium processors in China. Operating rates at leading processors have recovered to normal levels, and the broad recovery across the whole industry is expected by the end of this month.

Source: SMM

Lead-acid battery: Leading Chinese battery producer Camel Group said on Wednesday March 11 that its lead-acid battery plant and lead recycling plant in the COVID-19 epicentre of Hubei have resumed production after receiving approval from local authorities. Hubei previously said March 11 was the earliest businesses in the province could resume work. Authorities Wednesday issued a notice that laid out industry categories that could or could not resume operations based on the level of health risk in the region.

The latest SMM survey showed that all lead-acid producers in China, except for those in Hubei, have reopened by Wednesday, and that operating rates at some of major producers have exceeded 70% as labour tightness eased after the end of self-quarantine period. Some small lead-acid battery producers in Hebei and Henan and other regions remained shut until March, given manpower and logistics issues. Their production suspended lasted for nearly two months.

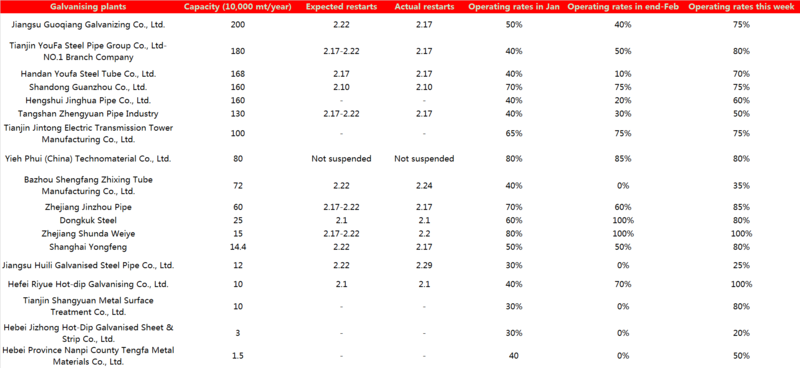

Galvanising: Most galvanising plants have resumed operations as of March 11, but they are still facing some headwinds such as manpower issues, which is especially seen at small producers and producers in north China, and slow resumption of end-users’ demand.

Large-scale galvanising plants have lifted their capacity utilisation rates to 70-80%, stepped up raw materials stockpiling on lower zinc prices and prepared inventories of finished products on optimistic prospects for demand recovery. Medium-scale and small producers, meanwhile, held operating rates at low levels due to limited new orders as most downstream projects have not resumed construction.

Operating rates of zinc galvanising plants

Source: SMM

Die-casting zinc alloy: Producers of die-casting zinc alloy remain in a recovery mode this week with operating rates significantly higher than the previous week. Operating rates at large- and medium- scale producers have climbed to 70%, while the rates at small plants stood around 50%.

The number of new orders also recovered but has not returned to pre-holiday levels. Frontloading of orders was seen at some downstream companies as zinc prices slipped, but any impact in the near term will be eased with the resumption of downstream demand.

The COVID-19 impact on domestic production of die-casting zinc alloy waned, but uncertainties around the virus development overseas may affect China’s exports of die-casting zinc alloy. SMM expects the business climate level in the sector this month to resume 70-80% of the levels pre-holiday.

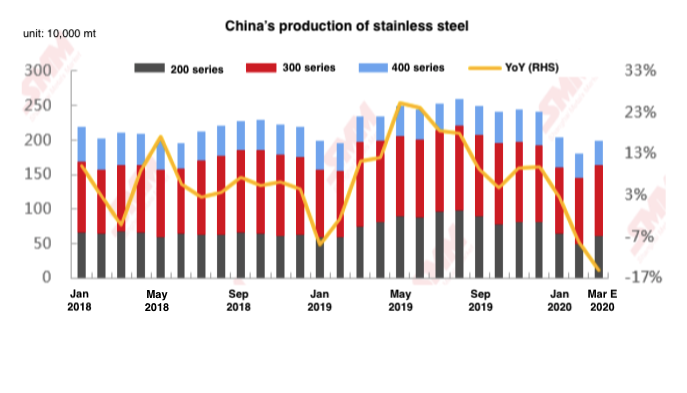

Stainless steel: Stainless steel output in February was about 1.8 million mt, a month-on-month decline of about 12%, and 8.3% lower compared to a year ago.

Average operating rate of stainless steel enterprises in February was around 67% amid the coronavirus outbreak which has delayed resumption of operations. Operating rate in March is expected to rebound to about 75%. The increase will be capped as high inventory levels and subdued downstream demand slow the resumption, and some of the stainless steel plants have not reached their optimised production state amid weak orders. On the other hand, some of the mills in China are still facing manpower shortage as there are workers who are unable to return to work due to transport and quarantine restrictions.

Stainless steel output has been at high levels since 2019, with year-on-year output growth reaching 25% in May 2019. In general, output tends to decline from November as steel mills usually carry out routine maintenance towards year-end, and output tends to fall in February because of lesser number of production days (2 days less) as compared to other months of the year.

Source: SMM

Electroplating sector: Electroplating plants were badly hit when the COVID-19 pandemic began its widespread in China, as these plants are scattered across the country and relied heavily on orders to maintain operations, and most of them halted production during the Chinese New Year holidays. Many of the plants have resumed operations since March 6 and began to receive orders, but overall output is limited. The larger electroplating plants are currently operating at desirable levels, and the capacity release rate is about 70%-80%.

Nickel alloy sector: At present, most of the alloy casting plants have resumed production, and some of the large state-owned steel mills were to maintain continuous production in February, with output release of around 85%. Plants that have resumed operations mostly have a capacity release rate of about 50%. Due to the relatively long production period of some of the military alloy plants, some of the orders will be delayed. Most of the plants also plan to restock raw materials on sable demand.

Cathode materials: Operating rates of cathode materials plants were significantly weighed by the delayed resumption of downstream battery producers. A handful of cathode materials mills in Henan, Guizhou and Shandong continued their operations during the CNY holiday, while producers in most provinces and cities returned from holidays in the first half of February, and focused on fulfilling pre-holiday orders. As of March 11, more than 90% of the cathode materials producers in China have restarted operations.

As of March 11, operating rates of most cathode materials plants have recovered to 50-60% with the rates at major mills rising to 70-80%, compared to an overall rate below 40% in February. Some producers of lithium manganese oxide (LMO) and LCO reported higher operating rates of 70%, while producers of ternary materials and lithium iron phosphate (LFP) mostly kept their rates at 60%. SMM expects overall operating rates to normalise between late-March and April.

Battery: Battery mills and carmakers, except for major producers such as Tesla, maintained low operating rates last month as the COVID-19 outbreak dampened consumption and resulted in sharp declines in production of new energy vehicles and batteries. Battery mills in Anhui, Tianjin, Jiangsu, Fujian and Guangdong resumed operations successively in the second half of February. About 60% of battery makers in China have reopened as of March 11, with the operating rates also climbing. Producers of consumer batteries resumed at a faster pace compared to power battery mills, and have started to restock raw materials.

Further Reading

SMM Webinar Series: Ferrous Supply Chain Update (Mar 11, 2020)

Cobalt and lithium producers in Hubei to resume in mid-March (Mar 11, 2020)

Chinese steelmakers recovered production while end-user recovery progressed slowly (Mar 11, 2020)

Exclusive: China's base metals output in February (Mar 9, 2020)

China unwrought aluminium, aluminium products exports dropped 25% YoY in January-February (Mar 9, 2020)

Operating rates of China silicon plants fell to 4-year low as COVID-19 disrupted raw materials supply (Mar 10, 2020)

China nickel manufacturing contracted for eleventh consecutive month in February (Mar 2, 2020)

For queries, please contact Lemon Zhao at lemonzhao@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn