SMM10, 19 October: on October 19, the "2018 China Nonferrous Metals Industry Annual meeting and 2019 (SMM) Metal Price Forecast Conference" sponsored by Shanghai Nonferrous Metals Network (SMM) was solemnly held in Pudong, Shanghai. Hong Lu, senior analyst of small metals at SMM, made a detailed analysis of the global cobalt and lithium market. Hong Lu believes that electric cobalt may rebound slightly for a while in the fourth quarter, cobalt salt rebound power is limited, and entered the off-season of consumption in November. Cobalt prices may once again enter the falling channel. As the oversupply becomes more pronounced in 2019, prices will face further downward pressure. On the lithium side, lithium carbonate prices are expected to remain depressed, while lithium ore is significantly surplus but prices are still high, there is relatively plenty of room to fall. The subsequent decline is expected to force lithium mine prices to fall, while falling lithium mine prices will further lower the cost support of lithium carbonate prices, and lithium hydroxide prices will accelerate their decline in the second quarter of next year, gradually reducing the premium to lithium carbonate.

Cobalt: the time for a significant oversupply of Cobalt in the World may have arrived

Demand side

According to SMM, lithium-ion battery industry accounts for more than 80% of cobalt demand, of which power lithium battery is the core driving force of demand growth.

Demand structure of Cobalt in China in 2017 and 2020:

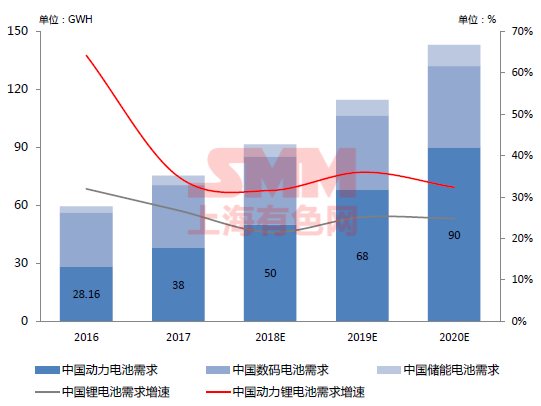

Market demand and growth rate of Lithium Ion batteries in China from 2016 to 2020:

In 2018 and 2019, the increment of cobalt demand in China's new energy automobile industry was 3200 cobalt metal tons and 4900 cobalt metal tons respectively. SMM expects full-year production of about 1 million new energy vehicles in 2018, up about 25 per cent from a year earlier. NCM ternary battery is mainly used in passenger cars, lithium iron phosphate battery is mainly used in pure electric bus, lithium manganate battery is mainly used in plug mixed bus market, special vehicle market, because the cost of ternary material is rising too fast. The proportion of ternary batteries will decline, and the proportion of lithium manganate and lithium iron phosphate will increase. SMM forecasts that the incremental demand for cobalt in China's new energy vehicle industry will be 3200 cobalt metal tons and 4900 cobalt metal tons in 2018 and 2019, respectively. SMM forecasts that demand for cobalt in China's new energy vehicle market will grow at a compound annual rate of about 47 per cent between 2017 and 2020.

Supply side

SMM expects global cobalt supplies to exceed 145000 tons in 2018, up 12 per cent from a year earlier, and expects global cobalt supplies to grow at a compound annual rate of about 9.5 per cent between 2016 and 2020.

Among them, the global supply of cobalt resources from 2018 to 2020 needs to focus on:

Kamoto Copper and Cobalt Project (Glencore): production is expected to resume in 2018, with production guidance of 11000 tons in 2018 and 34000 tons in 2019. 32000 tons in 2020.

Metalkol RTR Copper and Cobalt Project (Eurasian Resources): it is expected to go into production by the end of 2018 with a designed capacity of 14000 tons.

China Color Group Deziwa Copper and Cobalt Mine Project: it is expected to go into production by the end of 2018 and has a planned output of 7000 tons in 2019.

(Chemaf):, the Mutoshi copper and cobalt project, is expected to go into production in the fourth quarter of 2019 with a planned capacity of 16000 tons.

From January 2017 to June 2018, China's cobalt raw material inventory increased by 21000 tons of metal tons. In the first half of 2018, China imported about 39400 tons of cobalt raw materials, an increase of 27.5 percent over the previous month and 12 percent over the same period last year. Among them, cobalt ore was 7800 tons, an increase of 101 percent over the previous month, an increase of 87 percent over the same period last year, and 31600 tons of intermediate products in cobalt hydrometallurgy, an increase of 17 percent over the previous month and an increase of 2 percent over the same period last year. According to SMM research, in the first half of 2018, China produced 64000 tons of ternary materials, corresponding to cobalt consumption of 8000 metal tons, lithium cobalt acid production of 27000 physical tons, corresponding to cobalt consumption of 16000 metal tons. In addition to lithium cathode, cobalt powder and electrolytic cobalt consumption of 6000 metal tons. In the first half of 2018, a total of 30, 000 tons of cobalt raw materials were consumed, and the inventory of raw materials and smelting cobalt raw materials increased by 9400 tons of metal tons. Taking into account the fact that in 2017 China imported 69000 tons of cobalt raw materials, consumed 57500 tons and increased its stocks by 11500 tons. Stocks have increased by 21000 tons since 2017.

From January 2017 to June 2018, China imported cobalt raw materials:

The global supply of cobalt may reach 17700 tons in 2018, a significant oversupply or arrival. There is no dominant gap between supply and demand in the global cobalt market, but the spot oversupply is not significant under the pressure of hoarding and speculative storage. In 2018, the global supply of cobalt raw materials is expected to be 146700 tons, the demand is expected to be 129000 tons, and the supply surplus is 17700 tons. The global cobalt raw material increment in 2018 mainly comes from Glencore's Kamoto copper-cobalt ore, Tenke copper-cobalt ore, RTR copper-cobalt ore, PE527 copper-cobalt ore, Mikas copper-cobalt ore, medium color Deziwa copper-cobalt ore. SMM expects global cobalt to remain in excess of demand by 2020, peaking at 23000 tons in 2019.

Global Cobalt supply and demand balance from 2016 to 2020:

SMM expects that the increase in low-cost waste and the digital market downturn double attack, cobalt prices will shock down.

Cobalt market price outlook:

Price chart of SMM electrolytic cobalt and cobalt sulfate since 2016:

Cobalt metal:

Under the support of speculation and fundamentals, the price of 2017Q1 electrolytic cobalt has soared all the way, entering Q2 downstream consumption is insufficient, consumption inventory is the main, price rational consolidation, Q3 is at the time of rigid demand replenishment, internal and external price difference repair started. Q4 foreign media once again pull up but downstream consumption is weak, valuable non-market real consumption contraction. Domestic and international electricity cobalt continued to rise in the first quarter of 2018, but terminal consumption gradually showed fatigue after the Spring Festival, finally stopped rising in April and entered an inflection point, and then fell all the way down. The domestic market was the first to lead the decline, followed by a decline in overseas cobalt.

SMM expects cobalt in the fourth quarter high shock, terminal consumption is not good, oversupply does not change the overall situation, speculators continue to speculate difficult, the price center of gravity may go down.

Cobalt sulfate:

There was a rise in cobalt sulfate versus cobalt metal prices in the first quarter of 2017, mainly because downstream consumption grew significantly and the market expected subsequent cobalt prices to continue to rise, thus hoarding stocks in advance. However, the terminal to inventory in the second quarter, the manufacturers do not ship smoothly have to go to the finished product inventory, rising water no longer exists. The price of cobalt sulfate is sensitive to the fluctuation of electric cobalt price, and the rise and fall is the same as that of electric cobalt. The change of rising and sticking water reflects the difference between the basic strength of their supply and demand market. The coefficient of cobalt sulfate to electrolytic cobalt has fallen from a high of 1.05 in March 2018 to 0.98 in August, reflecting the weakness of the cobalt salt consumer market.

SMM expects a limited rebound in cobalt salt in the fourth quarter, in November into the off-season consumption, demand once again into the decline channel, while the supply of cobalt raw materials to maintain a steady slight increase, price rebound is not enough.

Lithium: the main reason for the halving of prices is that the growth rate of demand is not as fast as that of supply.

Demand side

SMM expects demand from the lithium-ion battery industry to rise by 10 per cent in 2020.

Lithium demand in China in 2017 and 2020:

Market demand and growth rate of Lithium Ion batteries in China from 2016 to 2020:

In 2018 and 2019, the demand for lithium in China's new energy vehicle industry increased by 3200 tons and 4900 tons, respectively. SMM expects full-year production of about 1 million new energy vehicles in 2018, up about 25 per cent from a year earlier. NCM ternary battery is mainly used in passenger cars, lithium iron phosphate battery is mainly used in pure electric bus, lithium manganate battery is mainly used in plug mixed bus market, special vehicle market, because the cost of ternary material is rising too fast. The proportion of ternary batteries will decline, and the proportion of lithium manganate and lithium iron phosphate will increase. SMM forecasts that demand for lithium in China's new energy vehicle industry will increase by 7400 tons in 2018 and 17000 tons in 2019. SMM forecasts that demand for lithium in China's new energy vehicle market will grow at a compound annual rate of about 33 per cent between 2017 and 2020.

Supply side

From 2017 to June 2018, the inventory of lithium raw materials in China increased by 61900 tons of lithium carbonate equivalent. In the first half of 2018, China imported about 96000 tons of lithium carbonate equivalent, an increase of 5 per cent from the previous month and 73 per cent from the same period last year. Among them, raw ore imports of 26600 tons of lithium carbonate equivalent, an increase of 12 percent over the previous month, an increase of 434 percent over the same period last year, and 69000 tons of concentrate imports, an increase of 2 percent over the previous month and an increase of 38 percent over the same period last year.

According to SMM research, in the first half of 2018, China produced 50, 000 tons of lithium carbonate and 21000 tons of lithium hydroxide. Excluding the salt lake supply of 11000 tons, the corresponding lithium consumption is 58000 tons of lithium carbonate equivalent. SMM expects lithium carbonate production of 110000 tons, an increase of 32.5 percent over the same period last year, and lithium hydroxide production of 50, 000 tons, an increase of 16 percent over the same period last year.

In the first half of 2018, a total of 58000 tons of lithium raw materials were consumed, and the inventory of lithium raw materials increased by 37600 tons of metal tons. Considering that in 2017, China imported 146300 tons of lithium raw materials, consumed 122000 tons, and increased its stocks by 24300 tons. Lithium ore stocks increased by 61900 tons between 2017 and the first half of 2018.

From January 2017 to June 2018, China imported lithium raw materials:

Total consumption of lithium raw materials by lithium salt production in China from January to June 2018:

Global lithium supply from 2016 to 2020:

The global supply of lithium resources from 2018 to 2020 focuses on:

Wodgina (Mineral Resources) mined 180 tons of raw ore in 2017 and plans to export 4.5 million tons of raw ore in 2018 and 5.5 million tons in 2019. Refined minerals are expected to go into production in the fourth quarter of 2019.

Pilgangoora (Altura,Pilbara Minerals):) is expected to ship in mid-2018. A total planned capacity of 550000 tons of lithium concentrate.

Bald Hill (Tawana/AMAL): production is expected in the fourth quarter of 2019. Planned production capacity of 160000 tons of lithium concentrate.

Greenbushes (Tianqi, Yabao): lithium concentrate is planned to expand to 1.34 million tons per year.

From 2017 to June 2018, the inventory of lithium raw materials in China increased by 61900 tons of lithium carbonate equivalent. In the first half of 2018, China imported about 96000 tons of lithium carbonate equivalent, an increase of 5 per cent from the previous month and 73 per cent from the same period last year. Among them, raw ore imports of 26600 tons of lithium carbonate equivalent, an increase of 12 percent over the previous month, an increase of 434 percent over the same period last year, and 69000 tons of concentrate imports, an increase of 2 percent over the previous month and an increase of 38 percent over the same period last year. According to SMM research, in the first half of 2018, China produced 50, 000 tons of lithium carbonate and 21000 tons of lithium hydroxide. Excluding the salt lake supply of 11000 tons, the corresponding lithium consumption is 58000 tons of lithium carbonate equivalent. In the first half of 2018, a total of 58000 tons of lithium raw materials were consumed, and the inventory of lithium raw materials increased by 37600 tons of metal tons. Considering that in 2017, China imported 146300 tons of lithium raw materials, consumed 122000 tons, and increased its stocks by 24300 tons. Stocks have increased by 61900 tons since 2017.

From January 2017 to June 2018, China imported lithium raw materials:

China's lithium carbonate production capacity is likely to exceed 250000 tons in 2018, and salt lake lithium production capacity permeability will be 20 per cent. 2018 is the inflection point of supply and demand of lithium carbonate in China, and the pattern of supply and demand has officially changed from tight balance to loose supply and excess capacity of 150000 tons of lithium carbonate and 54000 tons of lithium hydroxide at the end of 2017. Other countries in the world have a capacity of 140000 tons of lithium carbonate and 40, 000 tons of lithium hydroxide. It is expected that by the end of 2018, China's lithium carbonate production capacity will exceed 250000 tons, salt lake lithium permeability 20%, and lithium hydroxide production capacity expanded to 100000 tons. The new capacity of lithium carbonate in 2018 mainly comes from: Jiangte Motor, Sichuan Zhiyuan, Jiangxi Nanshi, Jiangxi Ganfeng, Hebei Tianyuan, Dongtai Lithium Resources, Jiujiang Ronghui, etc. The new production capacity of lithium hydroxide mainly comes from Ruifu in Shandong, Yongzheng in Quzhou, Baojiang in Jiangxi, Ganfeng in Jiangxi, Yabao in Jiangxi and so on. The total production capacity of lithium carbonate will be 180000 tons from 2019 to 2020. SMM expects China's lithium carbonate production capacity to exceed 390000 tons by 2020, of which salt lake lithium capacity permeability may exceed 30 per cent.

Energy production structure of lithium salt in China from 2017 to 2020:

SMM expects a glut of lithium mines and an increase in the share of lithium in salt lakes to put further downward pressure on lithium prices in 2019.

Lithium market price outlook:

SMM lithium salt price chart since 2016:

Lithium carbonate:

After a 15 per cent increase in Q1FMC prices in 2016, domestic lithium salt prices rose to a 10-year high, followed by the Q2 market into the off-season, downstream on-demand procurement, lithium carbonate prices rational correction. The demand for Q3 lithium batteries rose, reached a new balance between supply and demand and lasted until 2017Q2. due to the maintenance of the sky, which greatly affected the market supply, the price of lithium carbonate rose, and then, supported by demand, the price stabilized between 15 and 170000. To the fourth quarter due to the decline in market demand and supply continued to increase, supply and demand imbalance, prices all the way down. Affected by the Watma incident in the first half of 2018, the demand for lithium iron phosphate has been seriously weakened, and the price reduction of salt lake lithium has also put further pressure on the price reduction. The current price of battery-grade lithium carbonate has dropped below 80,000 yuan per ton.

SMM forecasts that lithium carbonate prices will remain depressed, while lithium ore is significantly surplus but prices remain high, with relatively plenty of room to fall. The subsequent fall in lithium prices is expected to force down lithium prices, which will further lower the cost support for lithium carbonate prices. In addition, the amount of lithium released from salt lake will also further stimulate the price of lithium carbonate. The complete cost of extracting lithium from salt lake is about 46, 000 yuan / ton, and the smelting cost ranges from 2 to 26000 yuan / ton, accounting for about 16% of the market supply. It is expected that as this proportion increases, the focus of lithium carbonate price trading will continue to decline.

Lithium hydroxide:

Generally speaking, lithium hydroxide contains lower lithium content, and the price is slightly lower than lithium carbonate. In 2016, high nickel ternary must be hyped with the concept of lithium hydroxide, lithium hydroxide to lithium carbonate premium. In the second half of 2017, 90% of the downstream demand for lithium hydroxide is still mainly ceramic glass grease, high nickel accounts for very little, and there is no shortage of lithium carbonate, so the price increase is not as good as lithium carbonate. After the second quarter of 2018, the situation of lithium carbonate oversupply was more severe, and lithium hydroxide, the fine powder used by high nickel, was still facing the dilemma of insufficient capacity, so the price fell less than lithium carbonate, again generating a premium to lithium carbonate.

SMM forecasts that lithium hydroxide prices will accelerate in the second quarter of next year, with a gradual reduction in the premium to lithium carbonate. The main reason is that the capacity bottleneck on the supply side will make a breakthrough with the expansion of production by the existing leading plants. In addition, new energy vehicles will catch fire frequently in the second half of this year, and the market will be more cautious about the progress of high nickel ternary development. Consumption expectations for lithium hydroxide will also be more rational.