SHANGHAI, Jun 18 (SMM) — Rebar prices rose slowly and fell sharply this week, and the overall prices fluctuated downward. The national average rebar price stood at 4,990 yuan/mt as of June 17, down 53 yuan/mt from last week. After the Dragon Boat Festival, the off-season market performance gradually became obvious, and the decline in the apparent demand for rebar expanded, with a month-on-month decline of 7.05%, an increase of 3.15 percentage points from last week. Decrease volume of the daily transaction was still within expectations, and social inventories officially ushered in a turning point in the accumulation of stocks.

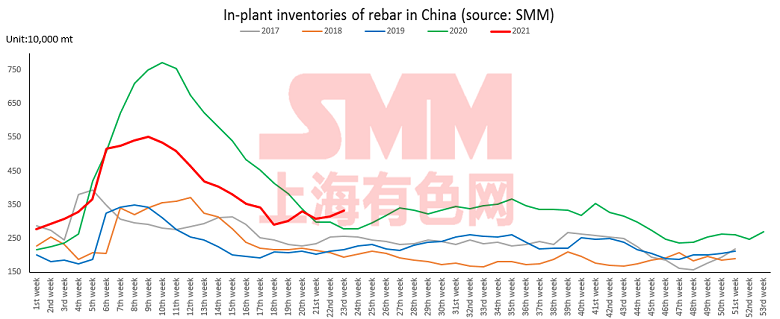

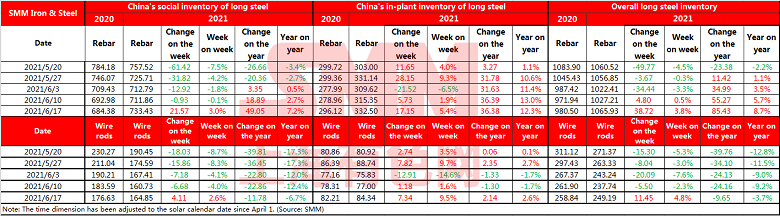

Inventories of rebar across Chinese steelmakers and social warehouses stood at 10.66 million mt as of June 17, up 3.8% from a week ago. Stocks are up 8.7% from a year earlier.

Inventories at Chinese steelmakers rose 171,500 mt on the week and stood at 3.33 million mt. Stocks are up 5.4% from a week ago and up 12.3% from a year earlier.

Inventories at social warehouses rose 215,700 mt on the week and stood at 7.33 million mt, up 3% from a week ago and 7.2% higher from a year ago.

The recent general fluctuating and downward trend of rebar prices was in line with the expectation of weak supply and demand in the off-season. In the absence of obvious positive news, it is easier to change the weak and fluctuating market.

The hawkish policy of the Fed's interest rate meeting on the evening of June 16 exceeded market expectations. Although it did not raise interest rates directly, the Fed will gradually recover liquidity through other means. China will still face the challenge of inflation for a long time.

The National Bureau of Statistics released May’s macro data on June 16. The relevant data was negative. Among them, real estate investment fell from a high level, and leading indexes such as real estate sales, land purchases, and funding sources fell. Infrastructure investment was weak, the need for counter-cyclical adjustment declined, and local fiscal space was limited. .

The characteristics of the supply side are high cost and high supply, low profit and low transaction. Since the fundamentals of raw materials are stronger than those of finished products, most steel companies are already at the basic line of profit and loss, and there is limited upward space for the output under the environment of peak carbon, . Judging from the China Iron and Steel Association’s May daily crude steel production data, it was down 1.7% month on month and up 6.6% year on year. Therefore, it is expected that the operating rate and output will continue to run at a high level, and decrease from the previous month.

At present, there are obvious signs of weakening demand in the off-season, while the decline is relatively slow. The reason is that under the new policy of "two centralized" land supply, the scale of the first batch of land supply in many places exceeds 40% of the annual plan and has been started in March-April. From January to May, the construction area of real estate development enterprises increased by 10.1% year on year, indicating that rigid demand will be more resilient in the second and third quarters. However, the land transaction data in May weakened. In addition, sales data declined, and the slower rate of capital withdrawal will further curb the subsequent land acquisition scale of real estate companies, and real estate investment will continue to be under pressure. Therefore, domestic steel demand will face certain uncertainty in the second half of the year.

Mining accidents occurred frequently, and large-scale safety inspections across the country will continue to make the raw material side stronger. Steel enterprises are already at the bottom of the basic line of profit and loss, and the price support is strong. In addition, the scope of production restrictions before July 1 is expanding, and the supply is expected to shrink.

The upward momentum is insufficient and the transaction support is weak and difficult to continue, the downward space is limited with strong bottom support, and the anti-draw height is also low. Steel prices will continue to fluctuate rangebound in the near term.