SHANGHAI, Jul 1 (SMM) – Manufacturing activity across nickel downstream sectors in China expanded for the fourth consecutive month in June, but the expansion continued to slow from a month ago.

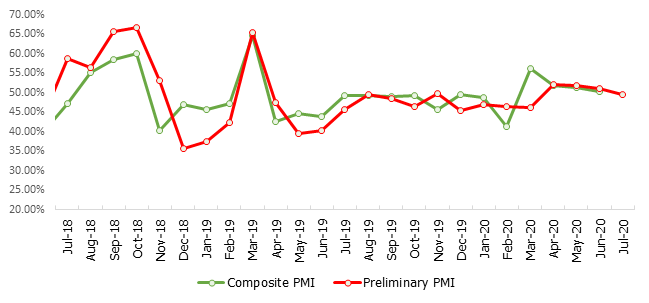

SMM data showed that the purchasing manager's index (PMI) for downstream nickel industries, including stainless steel, electroplating, alloy and battery, stood at 50.25 in June, down 1.18 point from May. A reading above 50 indicates expansion.

The preliminary nickel downstream sectors PMI for July is assessed at 49.45, slipping 0.81 point from the final reading for June and dipping into contractionary territory.

Production sub-index flat in June with higher output of #300 stainless steel but slower operation in electroplating

The composite sub-index for production in June was unchanged from a month ago at 52.25, staying in expansion. The production sub-index in the stainless steel sector slipped 0.96 point month on month to 53.14, as intensified losses drove some medium-scale and small stainless steel mills to cut output. However, the decline in output was offset by ramped-up production at large plants, which kept the stainless steel production activity in expansion.

The production sub-index in the electroplating sector further contracted to 37.69 amid continued headwinds facing producers. Some electroplating plants in south China have adjusted their working schedule to give workers more time off per week so as to reduce the business pressure from sluggish orders. Operations in other nickel downstream sectors were largely stable in June.

New orders sub-index fell to contraction, orders in sectors other than battery weakened in June

According to SMM data, the overall sub-index for new orders across downstream nickel sectors flipped to a contraction territory of 48.9 in June, down 2.68 points from May. The new orders sub-index in the stainless steel sector dipped 4.19 points on the month to 49.33, as inventories lingered at high levels with trades and prices weakening from May.

In the alloy sector, the new orders sub-index eased to 48.21. Some alloy plants reported subdued orders last month, especially for electrical heating alloy products. High-nickel content alloy saw almost no new orders in June and orders for high-temperature alloy also decreased. The new orders sub-index in the battery sector climbed to 53.41 as overseas consumption revived with support from stimulus measures in America and European countries.

Raw materials inventory sub-index in expansion amid stockpiling of NPI, purchases of electroplating nickel slowed

The overall sub-index for raw materials inventories came in at 52.58 for June, 5.99 points lower from May but still in expansion. Most stainless steel mills maintained stable purchases on normal operation, but some large-scale stainless steel makers tended to lengthen the inventory cycle and procured raw material NPI in advance for the production in August. This drove up the feedstock inventories and kept the sub-index for raw materials stocks in the stainless steel sector at 53.81 in June.

The sub-index in the electroplating sector stood at 40.78, as electroplating plants purchased in smaller amounts with lower frequency last month. Domestic traders of electroplating nickel said their trade volumes slipped more than 20% month on month in June. Some market participants believed that the electroplating sector has entered a slow season in advance last month.

Finished goods inventory sub-index contracted with inventory pressure mounting in some sectors

The overall sub-index for finished products stocks fell 2.62 points from a month ago to 48.68 in June, below the growth-contraction threshold. Finished products inventories at stainless steel mills piled up as production expanded while transactions weakened from the previous month. This saw the finished products inventory sub-index for the stainless steel sector at 48.68.

The sub-index for the electroplating sector posted 49.16. Inventory in the electroplating sector, typically at stable levels, increased last month as an escalation in the coronavirus outbreak overseas dragged on exports from China.

![[SMM Analysis] The April turn: how Chinese stainless mills came around to higher NPI prices](https://imgqn.smm.cn/production/admin/votes/imagesDAZmS20260504170607.png)

![[SMM Stainless Steel Flash] UK/EU Steel Prices Surge Amid Tariffs; India Grants Relief to SMEs](https://imgqn.smm.cn/usercenter/GmHLU20251217171733.jpg)