November 28, 2025

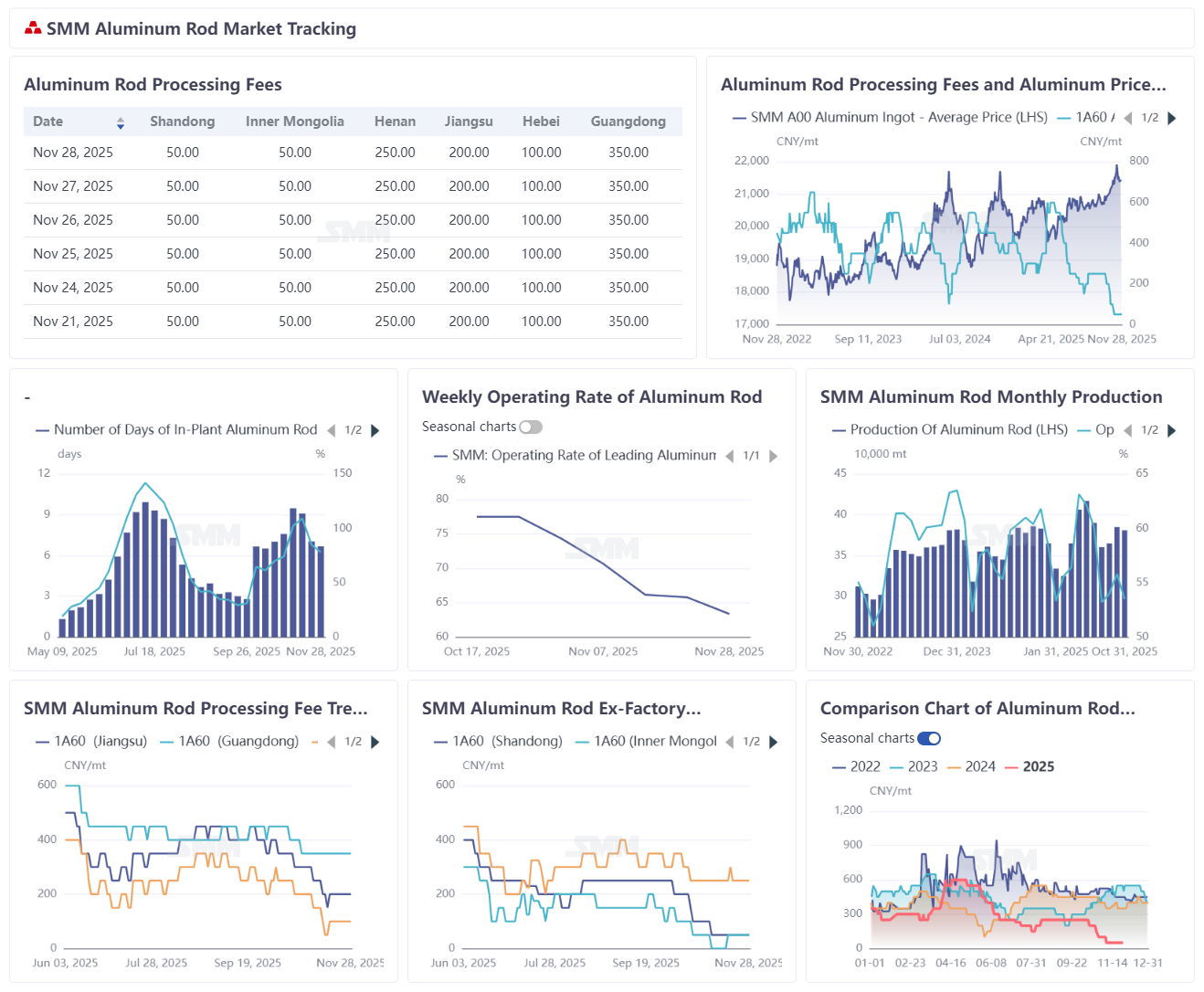

According to SMM statistics, as of November 28, 2025, domestic aluminum rod producers' inventory days stood at 6.68 days, a decrease of 0.36 days week-on-week, indicating an inventory drawdown trend with slightly eased supply-side pressure. The inventory ratio was recorded at 78.17%, down 6.74 percentage points from the previous week. Aluminum rod processing fees continued hovering at low levels throughout the week. Coupled with the bottoming-out recovery of aluminum prices, support for processing fee hikes remained insufficient. Downstream procurement sentiment improved modestly during the week, yet market inventories remained undigested. Amid ongoing supply-demand imbalance, the momentum for processing fee recovery remained relatively weak. Regarding regional processing fees (as of October 31, 2025): Jiangsu offered RMB 200-300/mt, Hebei RMB 100-200/mt, and South China RMB 300-400/mt. For other regions: Shandong quoted RMB 0-100/mt, Inner Mongolia RMB -50-150/mt, and Henan RMB 200-300/mt. Current processing fees are consolidating at the bottom with limited downside potential. As fee fluctuations closely correlate with plant inventories and aluminum prices, inventories are expected to return to safe levels by December, providing fundamental support for processing fees.

This week's aluminum cable operating rate rose 0.6 percentage points week-on-week to 63%, continuing its moderate recovery trend. This improvement stems from marginally better orders as the industry gradually emerges from seasonal lows, supporting production recovery. Though orders have improved, they haven't reached peak-season delivery levels. Winter temperatures now constrain project progress, while grid-side procurement sustainability expectations weaken. With year-end approaching, companies show limited willingness to build finished product inventories, maintaining only normal delivery-paced production. Although November saw concentrated grid bidding (with new order growth expected in December), deliverable orders within this year remain limited. The market awaits next year's grid concentrated delivery cycle - maintaining medium-to-long-term demand optimism despite persistent short-term weakness. Next week, while the operating rate remains on a recovery path, constraints including winter construction limits, weakening grid procurement momentum, subdued year-end stocking interest, and unremarkable order growth will cap further upside potential.