Новости SMM от 25 ноября:

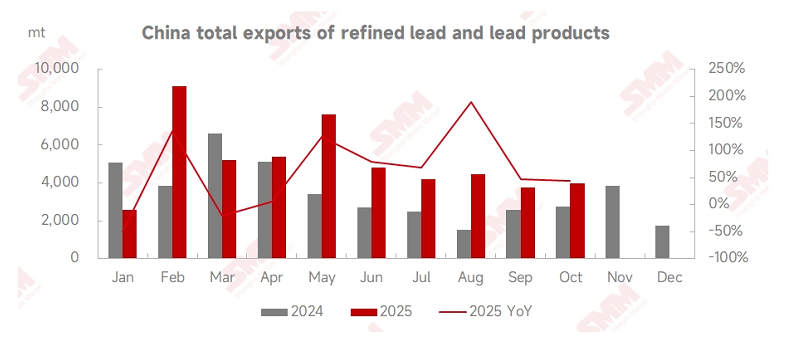

По данным таможенной статистики, экспорт рафинированного свинца из Китая в октябре 2025 года составил 2 098 тонн, увеличившись на 41,2% в месячном исчислении и на 11,25% в годовом. Совокупный экспорт рафинированного свинца и свинцовой продукции с января по октябрь достиг 51 156 тонн, что на 41,56% больше, чем годом ранее. Со стороны импорта, Китай импортировал 3 812 тонн рафинированного свинца и 14 477 тонн свинцового сплава в октябре. Общий объем импорта рафинированного свинца и свинцовой продукции за первые десять месяцев составил 140 240 тонн, снизившись на 28,97% в годовом исчислении.

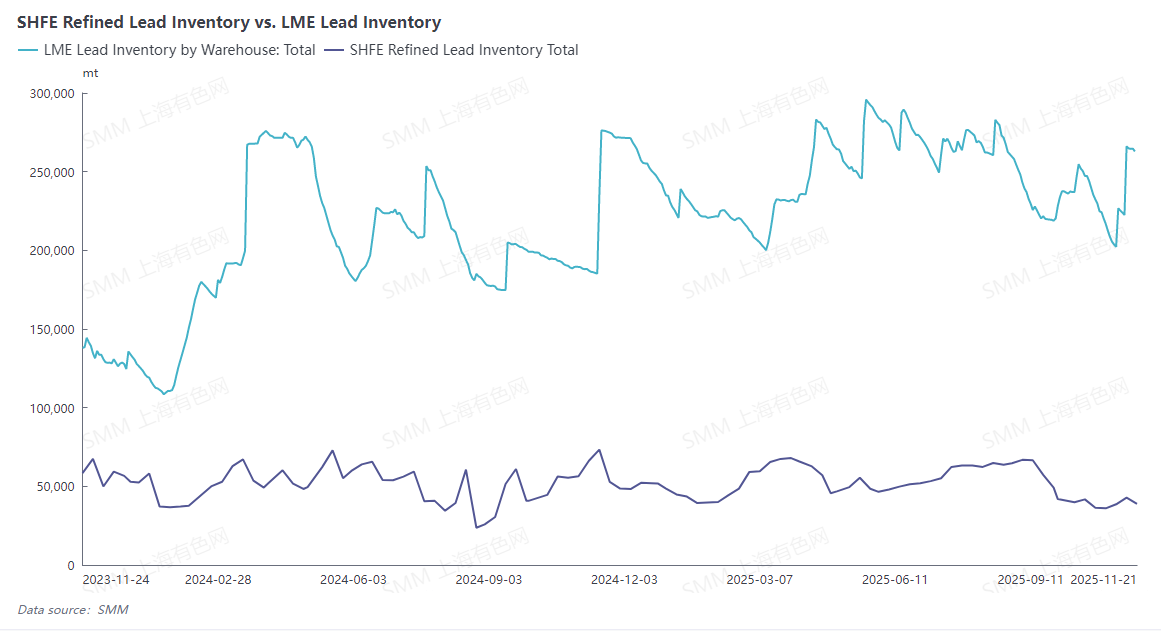

В начале октября макроэкономические настроения были медвежьими, наряду с ростом запасов свинца на Лондонской бирже металлов (LME), которые еженедельно увеличивались более чем на 10 тыс. тонн. Цены на свинец на LME упали ниже отметки в 2 000 долларов, достигнув минимума в 1 963 доллара за тонну. Тем временем, фьючерсы на свинец на Шанхайской фьючерсной бирже (SHFE) оказались под давлением из-за динамики на LME, колеблясь на низких уровнях в начале октября. К концу октября меры контроля, связанные с охраной окружающей среды, привели к остановке производства на некоторых заводах в Северном Китае и сбоям в логистике в Центральном Китае. В сочетании с колебаниями складских запасов свинцовых чушков на низком уровне, ценовой центр свинца на SHFE колебался с восходящим трендом. Запасы свинца на LME продолжали снижаться в конце октября, что способствовало подъему цен на LME. В этот период предложения по свинцовым чушкам из-за рубежа снизились в месячном исчислении, а импортные чушки, поступающие на китайский рынок, в основном были из заказов, размещенных в сентябре.

В начале ноября технические фонды подтолкнули цены на свинец вверх, фьючерсы на SHFE достигли почти семимесячного максимума, что способствовало росту цен на LME до пика в 2 097 долларов за тонну. К середине ноября запасы свинца на LME резко выросли, возможно, из-за неусвоенного сокращения запасов в конце октября, наряду с переходом к медвежьим макроэкономическим настроениям, что вызвало нисходящие колебания на LME. Свинец на SHFE также вернулся к фундаментальным факторам, закрываясь ниже несколько дней подряд и достигнув минимума в 17 115 юаней за тонну. Активность по сделкам с импортным свинцом оставалась низкой, поступающие чушки в основном были из ранее заключенных заказов. Кроме того, геополитические изменения в ноябре повлияли на торговые отношения, в определенной степени воздействуя на сделки с импортным свинцом. В целом, SMM прогнозирует, что импорт свинцовых чушков в Китай в ноябре может незначительно снизиться.

Заявление об источниках данных: За исключением общедоступной информации, остальные данные получены SMM на основе публичной информации, рыночной коммуникации и внутренней базы данных и моделей SMM, носят справочный характер и не являются рекомендацией для принятия решений.

![На фоне роста длинных позиций наиболее активно торгуемый майский контракт на свинец SHFE 2605 сегодня продемонстрировал односторонний восходящий тренд [Краткий обзор фьючерсов на свинец]](https://imgqn.smm.cn/usercenter/rDPju20251217171722.jpg)