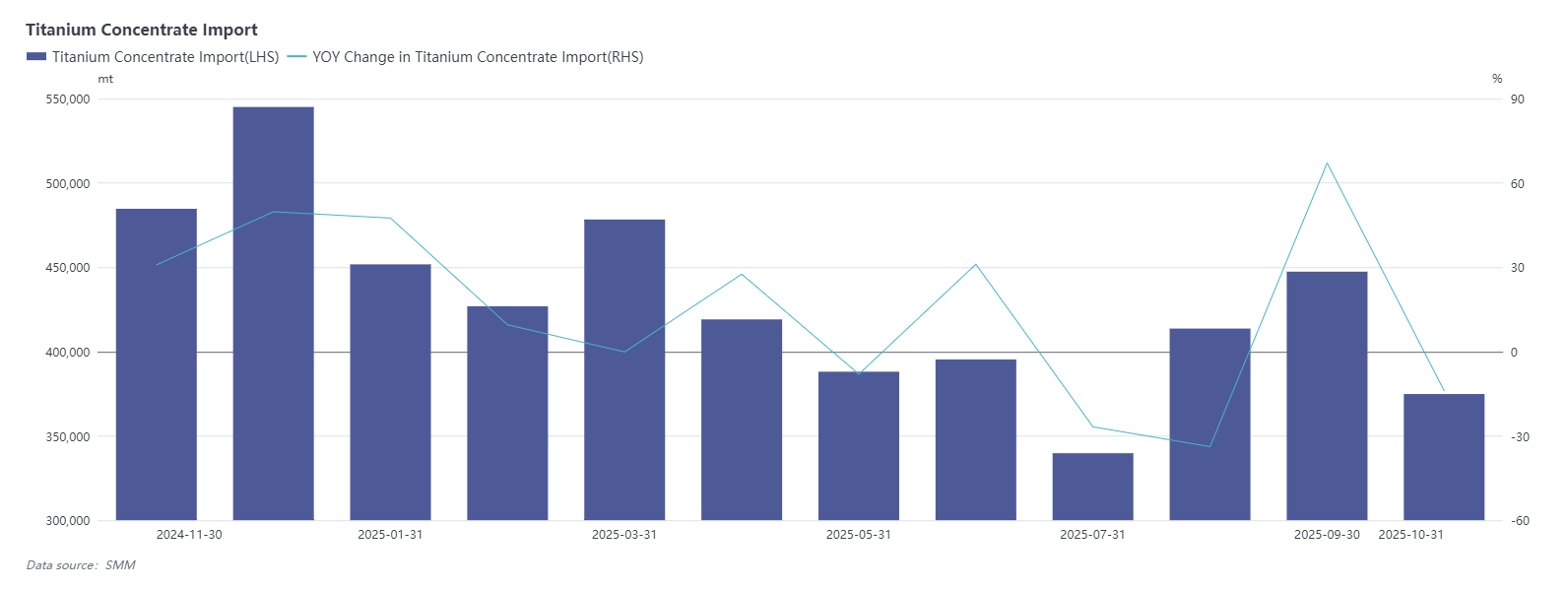

Titanium Concentrate Imports Fall 16% MoM as "Silver October" Demand Disappoints

In October 2025, China's titanium concentrate imports reached 374,800 tonnes, a decrease of 16.22% month-on-month. The cumulative import volume for the year reached 4.1349 million tonnes, representing a cumulative year-on-year increase of 2.87%. Entering October, import volumes weakened further, primarily corresponding to lower overall market demand downstream. After the "Golden September" market showed a phased recovery, the "Silver October" demand performance fell short of expectations. Weak demand gradually transmitted upstream, leading to intensified competition in the imported titanium concentrate market and overall downward pressure on prices.

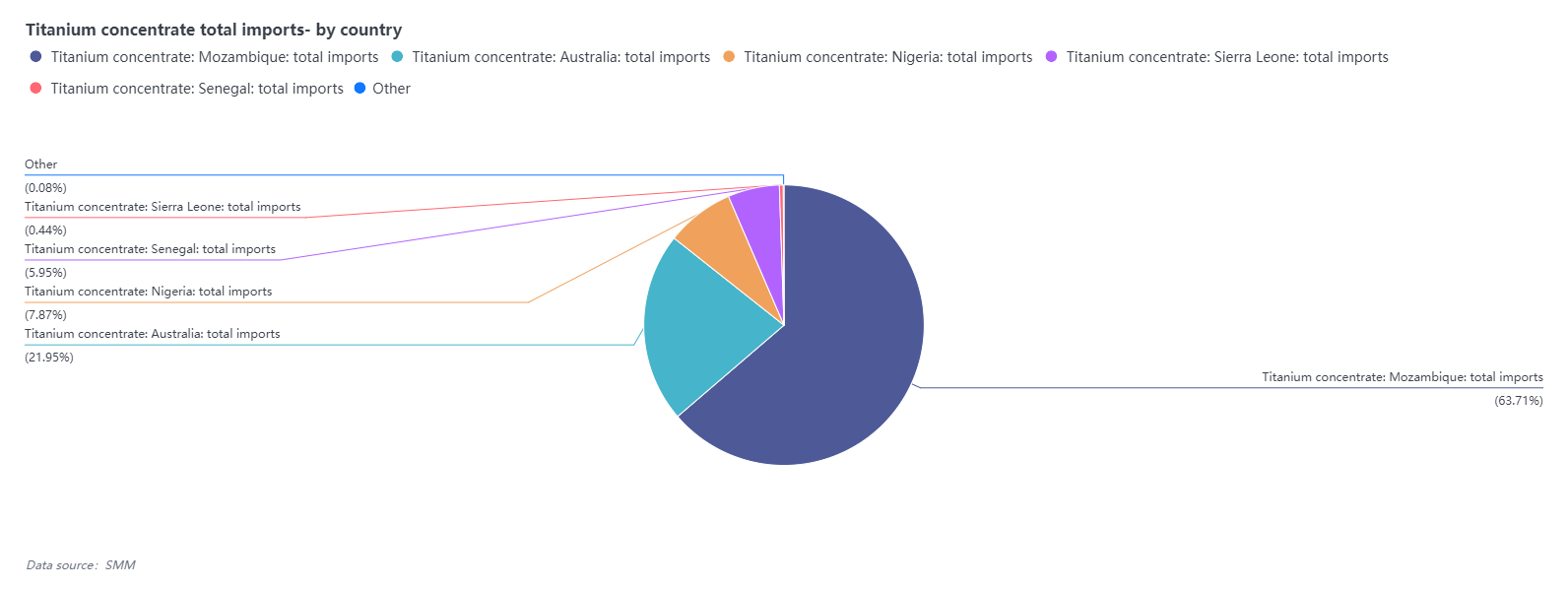

Looking at import source countries, Mozambique remained the top source, with exports to China reaching 189,000 tonnes in September, reflecting that Africa continues to be the main supply region for China's titanium concentrate imports. However, the competitiveness of Mozambican ore in the domestic market is relatively limited, and the advantage of imported ore still mainly relies on grade support. The current market pricing mechanism is becoming more complex, generally adopting a "one mine, one negotiation" model. Considering the overall lack of boost in the downstream titanium dioxide market, titanium concentrate demand is expected to remain difficult to improve significantly in the short term.

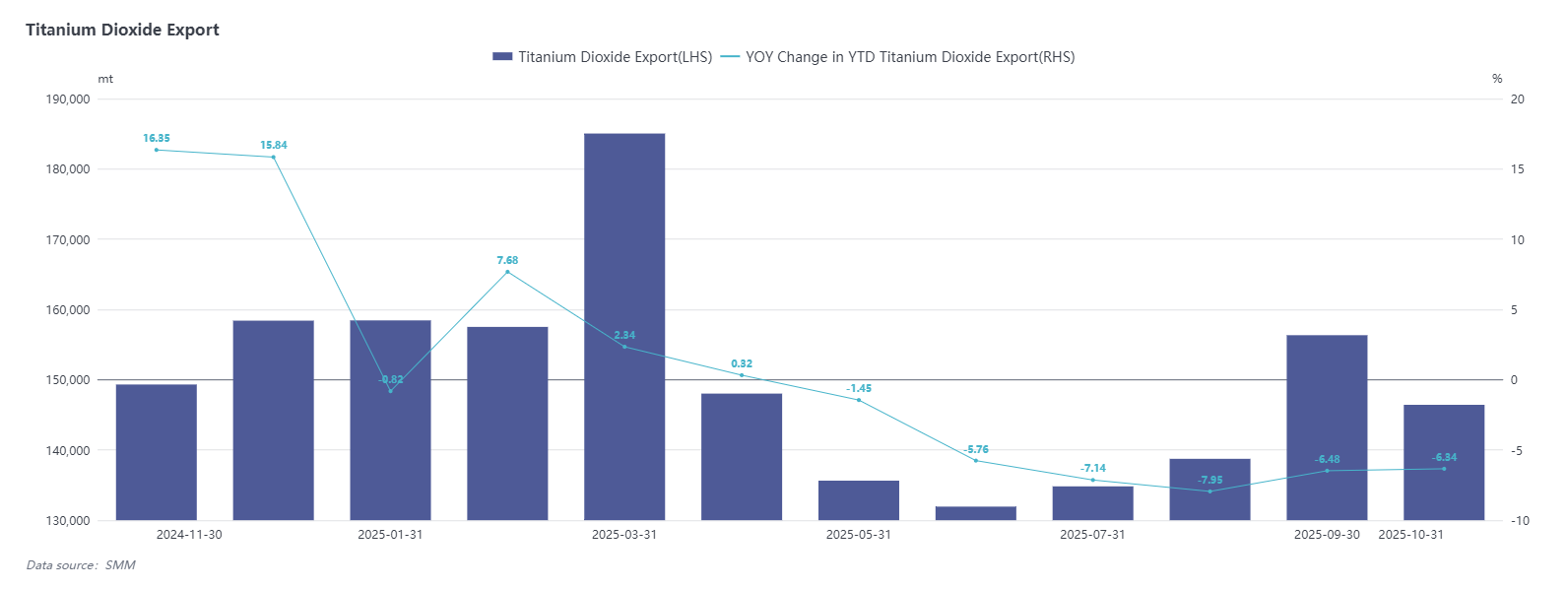

Titanium Dioxide Exports Down 6.3% MoM as High Overseas Inventories Curb Demand

In October 2025, China's titanium dioxide exports were 146,000 tonnes, down 6.34% month-on-month. Exports from January to October totaled 1.2928 million tonnes, a cumulative year-on-year decrease of 6.34%. Titanium dioxide exports showed a slowing trend in October, mainly affected by persistently high inventory levels in overseas markets. On one hand, previous concentrated arrivals led to slow inventory digestion in major importing countries, correspondingly slowing their procurement pace. On the other hand, weak manufacturing sentiment in some global regions, insufficient demand support from downstream sectors like coatings and plastics, coupled with seasonal off-peak factors, collectively suppressed import demand for titanium dioxide. Although the domestic supply side remains stable, short-term exports will likely remain under pressure against the backdrop of overall weakening external demand.

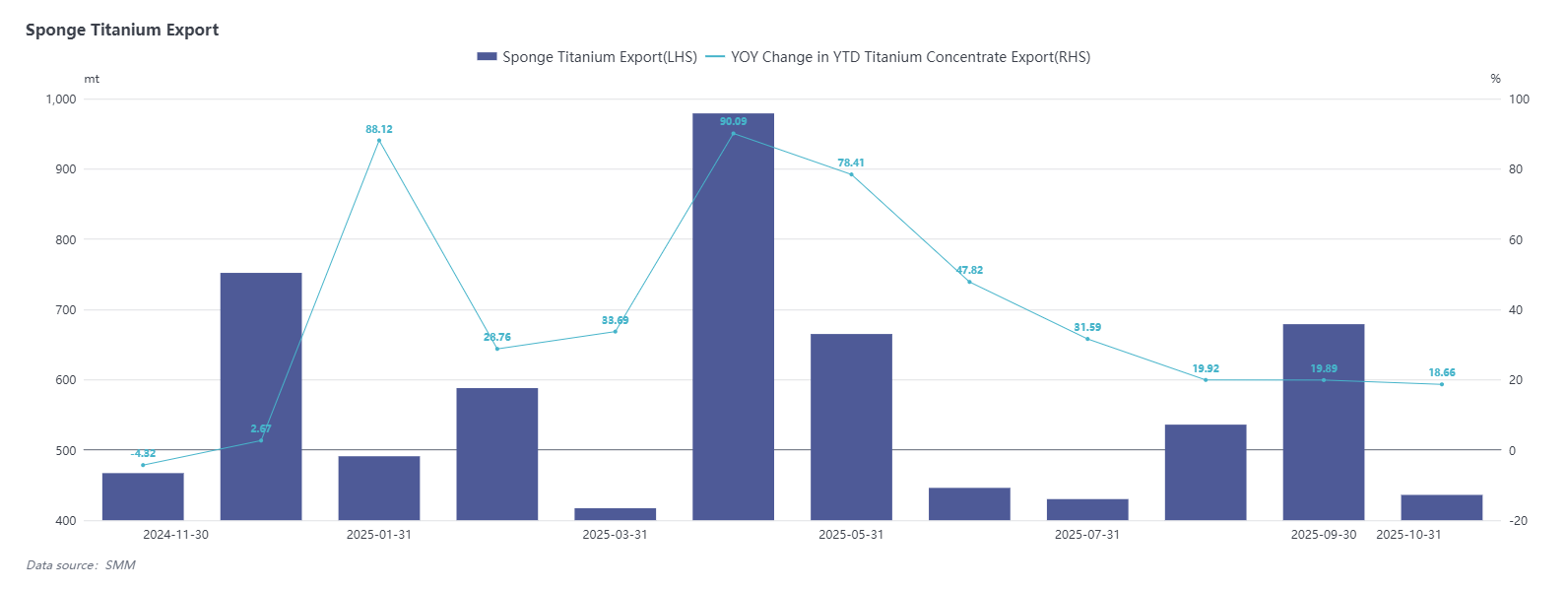

Sponge Titanium Exports Drop 35.8% MoM as Weak Demand Persists in Titanium Market

In October, China's sponge titanium exports were 436 tonnes, a decrease of 35.79% month-on-month. Cumulative exports from January to October 2025 were 5,667 tonnes, a cumulative year-on-year increase of 18.66%. Judging from the data, single-month exports declined in October, but looking at the whole year, sponge titanium exports overall maintained a growth trend, reflecting the gradual emergence of the effectiveness of international market expansion in the first half of the year. Behind this trend, China's international competitiveness in the high-end sponge titanium sector continues to improve, becoming a key factor supporting export growth.

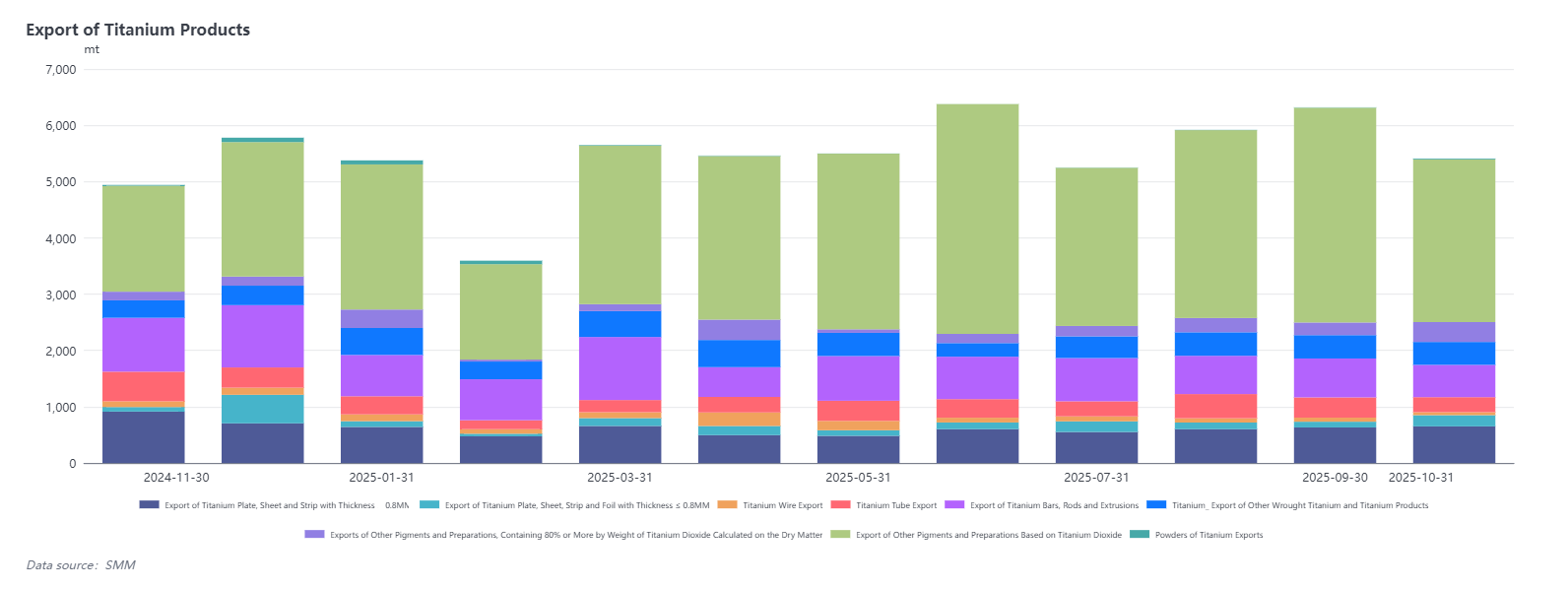

During the same period, titanium material exports also showed a certain degree of contraction, with the cumulative export volume being approximately 5,400 tonnes, overall declining compared to the previous period. This indicates that current international titanium market demand is generally weak, with a slowdown in procurement pace. Besides the macro-environmental impact, this phenomenon may also be related to the early release of some orders in the third quarter, which to some extent pulled forward subsequent demand.

October Summary: Overall Pressure on Titanium Market as Upstream and Downstream Demand Weakens Simultaneously

China's titanium market exhibited a pattern of weak supply and demand in October. Upstream titanium concentrate imports fell 16.22% MoM to 374,800 tonnes, as disappointing "Silver October" demand intensified market competition and put downward pressure on prices. Midstream titanium dioxide exports decreased 6.34% MoM to 146,000 tonnes, constrained by high overseas inventories and insufficient manufacturing momentum. Downstream sponge titanium exports fell sharply by 35.79% MoM to 436 tonnes; although cumulative exports maintained year-on-year growth, the short-term demand slowdown was evident.

From a market structure perspective, Mozambique remains the primary source for titanium concentrate imports, but its competitiveness still relies on grade advantages. Titanium dioxide continues to face pressure from high overseas inventories. Although sponge titanium maintains an advantage in the high-end sector, its short-term export momentum has weakened due to the global demand downturn and the front-loading of Q3 orders. Overall, the titanium market continued its adjustment trend in October, with both upstream and downstream enterprises facing the challenge of insufficient demand. A strong recovery is expected to have limited momentum in the short term.

![[SMM Analysis] Titanium Dioxide Prices Rise Amid Cost Pressures and Geopolitical Tensions](https://imgqn.smm.cn/usercenter/QmrGh20251217171725.jpg)

![Cost-Driven Titanium Dioxide Price Increases Took Effect, Market Price Adjustments Released Upward Signals [SMM Titanium Weekly Review]](https://imgqn.smm.cn/usercenter/ZVhtl20251217171724.jpeg)

![Imported Titanium Ore Market Under Pressure, Sluggish Port Sales Forced Traders to Cut Prices for Shipments [SMM Titanium Spot Flash Report]](https://imgqn.smm.cn/usercenter/JPzPS20251217171723.jpeg)