I. Secondary Lead Production Dynamics

-

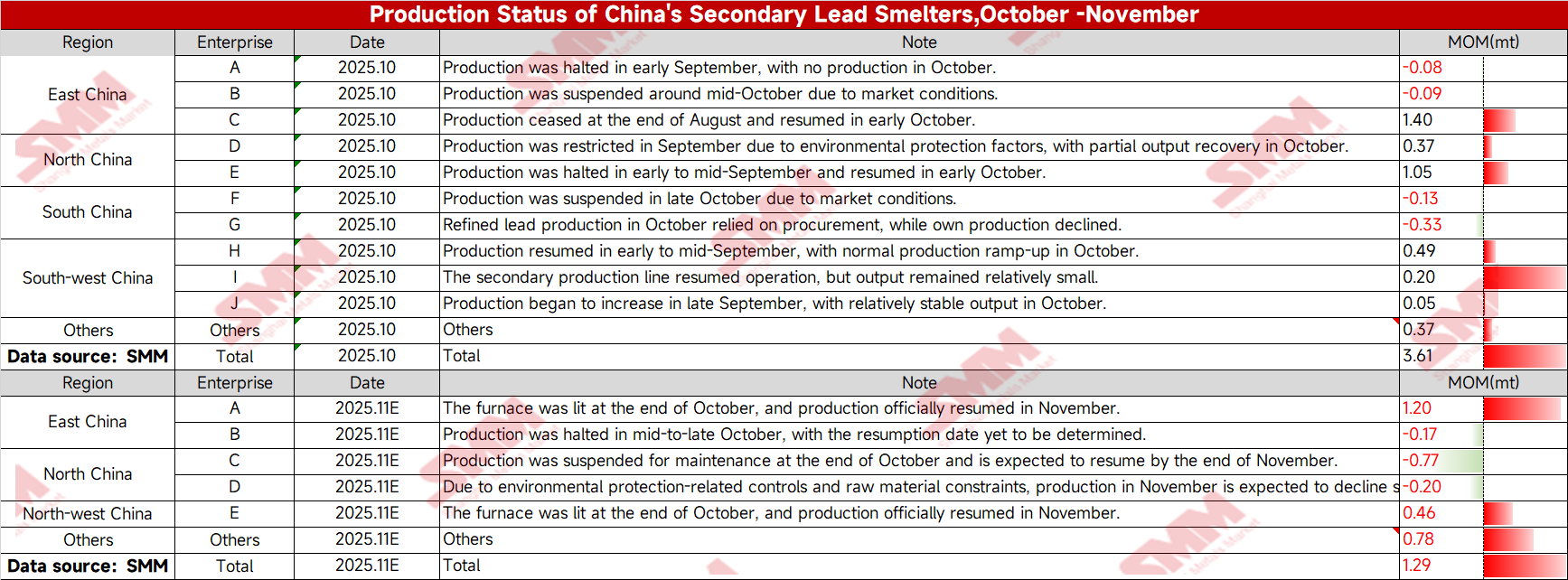

Multiple Smelters Resumed Production in October, Output Increased as Expected

In October, multiple secondary lead smelters resumed production, and secondary lead output rose as expected. After entering November, large secondary lead smelters are still expected to resume production, and secondary lead output is projected to maintain a growth trend.

-

Market Focus

Currently, the market is highly focused on whether raw material supply can continuously support the increase in secondary lead production. SMM analyzes the relevant situation based on public information, market communication, and internal database models for reference by market participants.

II. Analysis of Raw Material Inventories of Secondary Lead Smelters

-

Current Status of Raw Material Inventories

As of October 31, the monthly days of raw material inventories of secondary lead smelters were 1–2 days higher than the historical average. However, this inventory increase was not due to an increase in the retirement volume of waste lead-acid batteries in the market.

-

Background and Changes in the Waste Lead-Acid Battery Market

Market Situation in Early August 2025

In early August 2025, lead prices hit a nearly two-month low, while scrap lead-acid batteries were in an undersupply situation with persistently high prices. The loss margin for secondary lead smelting widened, leading to widespread production reductions and suspensions among secondary lead smelters.

Market Reaction After Production Suspension

The suspension of production by secondary lead smelters prompted a reduction in raw material procurement offers. The competitive pressure for waste lead-acid batteries subsequently weakened, and other operating smelters successively lowered their procurement offers.

Price Fluctuations and Inventory Transfer

From mid-to-late August, scrap lead-acid battery prices pulled back significantly, reaching a temporary low in mid-September. As lead prices fluctuated upward and the pace of production resumptions at secondary lead smelters accelerated, scrap lead-acid battery prices gradually rebounded. During this period, recyclers sold due to fear of price declines caused by lower raw material offers from secondary lead smelters, and their scrap battery inventories were gradually transferred to smelters, becoming the smelters' raw material inventories.

Reasons for Eased Raw Material Inventories in October

In summary, the easing of raw material inventories at secondary lead smelters in October was mainly attributable to improved willingness to sell among recyclers and reduced digestion of waste lead-acid battery inventories by smelting enterprises due to production suspensions. III. Transformation and Raw Material Procurement Strategies of Secondary Lead Smelters

-

Overcapacity and Transformation Trend

Severe overcapacity in secondary lead has made the undersupply of waste lead-acid batteries a market norm. Currently, secondary lead smelters are gradually transitioning into multi-raw material producers utilizing both lead concentrates and waste lead-acid batteries. According to enterprises with transformation intentions, dependence on waste lead-acid batteries as raw material is expected to decrease from 95% to 20% after successful transformation.

-

Procurement Strategy and Recycler Response

The purchasing attitude of secondary lead smelters toward waste lead-acid batteries has, to some extent, influenced recyclers’ willingness to sell. Unlike the hoarding behavior seen in H1, recyclers are now maintaining normal turnover of battery scrap due to concerns over price declines, leading to stabilized raw material arrivals at smelters.

IV. Secondary Lead Production and Market Outlook

-

Arrivals and Production Stability

Stable arrivals of waste lead-acid batteries support continuous production at secondary lead smelters. However, secondary lead output remains influenced by smelters’ production willingness (profitability). If transformation succeeds, secondary lead smelters may increase primary lead output while reducing secondary refined lead production accordingly.

-

Market Outlook

Overall, against the backdrop of production resumptions and transformation in the supply side, raw material supply and production patterns in the secondary lead market are undergoing changes. Market participants should closely monitor production dynamics at secondary lead smelters and supply-demand shifts in the raw material market to prepare for potential future fluctuations. The above analysis is based on SMM’s market surveys and data models, for reference only.

Data Source Statement: Except for publicly available information, other data are derived by SMM based on public information, market communication, and SMM's internal database model, and are for reference only, not constituting decision-making advice.

![SHFE Lead Rebounded Slightly After an Intraday Dip and Closed with a Small Bearish Candlestick [Lead Futures Brief Review]](https://imgqn.smm.cn/usercenter/qnyHQ20251217171721.jpeg)

![LME Lead Bottomed Out, While SHFE Lead Retreated After Rapid Rise and Consolidated [SMM Lead Morning Brief]](https://imgqn.smm.cn/usercenter/EhsCj20251217171721.jpeg)