On July 30 local time, the US White House announced that President Trump signed a proclamation imposing tariffs on several categories of imported copper products. The proclamation stated that starting August 1, a 50% tariff would be universally applied to imported semi-finished copper products (such as copper pipe & tube, copper wire, copper billet, copper plate, and copper tube) and copper-intensive derivatives (such as pipe fittings, cables, connectors, and electrical components). The White House clarified that copper input materials (including copper ore, concentrates, matte copper, copper cathode, and copper anode) and copper scrap are not subject to "Section 232" or reciprocal tariffs. Under Section 232 of the US Trade Expansion Act of 1962, the US President has the authority to impose tariffs or set quotas on imports based on "national security" considerations. Subsequently, the LC price spread rapidly narrowed. On August 11, the increased probability of a US Fed interest rate cut weakened the US dollar, driving up risk assets and precious metals, with copper prices continuing to rise and breaking through 79,000 yuan/mt. After retracing some gains, prices stabilized around 78,500 yuan/mt. On August 22, A-shares rose, with the Shanghai Composite Index surpassing 3,800 points, hitting a new 10-year high. By August 25, expectations for a Fed rate cut were further reinforced, boosting risk assets. With successive positive macro developments domestically and overseas, copper prices surged again, approaching the 80,000 yuan/mt threshold. In August, copper fundamentals were in the off-season for consumption, compounded by high prices, resulting in overall mediocre demand. On August 31, per the "Notice on Standardizing Investment Promotion Policies" (No. 770, 2025) jointly issued by four ministries including the National Development and Reform Commission, local governments were required to regulate investment promotion policies, with non-compliant contracts signed after May 2024 to be terminated by August 31, 2025. Policy changes in the recycled materials sector gradually permeated the industry chain, laying the groundwork for higher copper prices in the future.

Analyzing Market Strategies to Position for and Drive Up September Copper Prices

Macro Front:

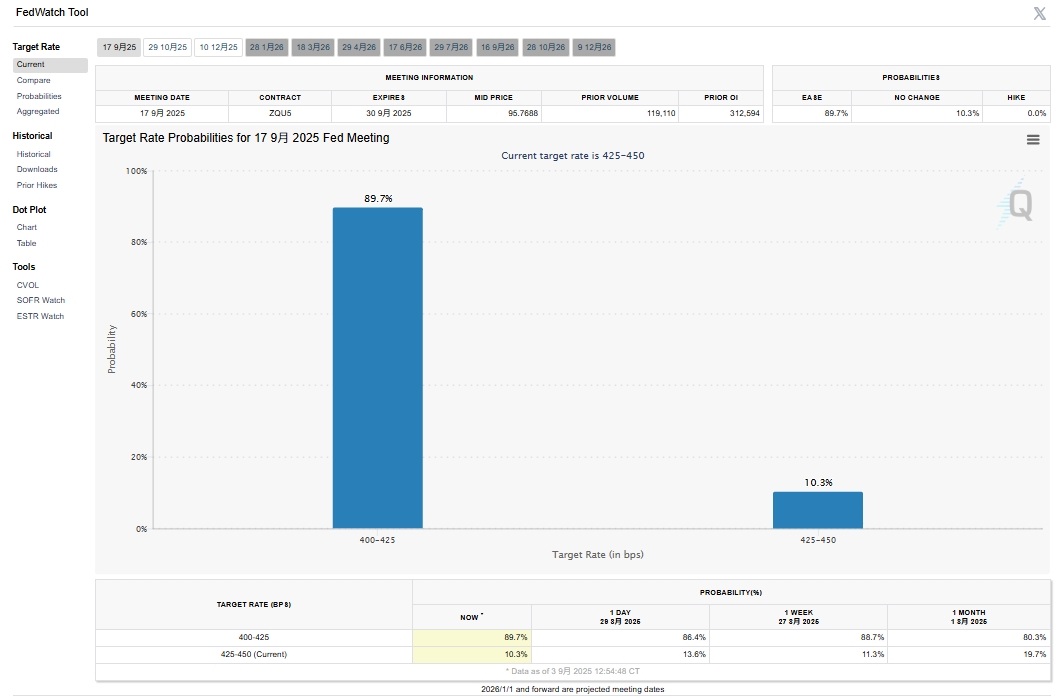

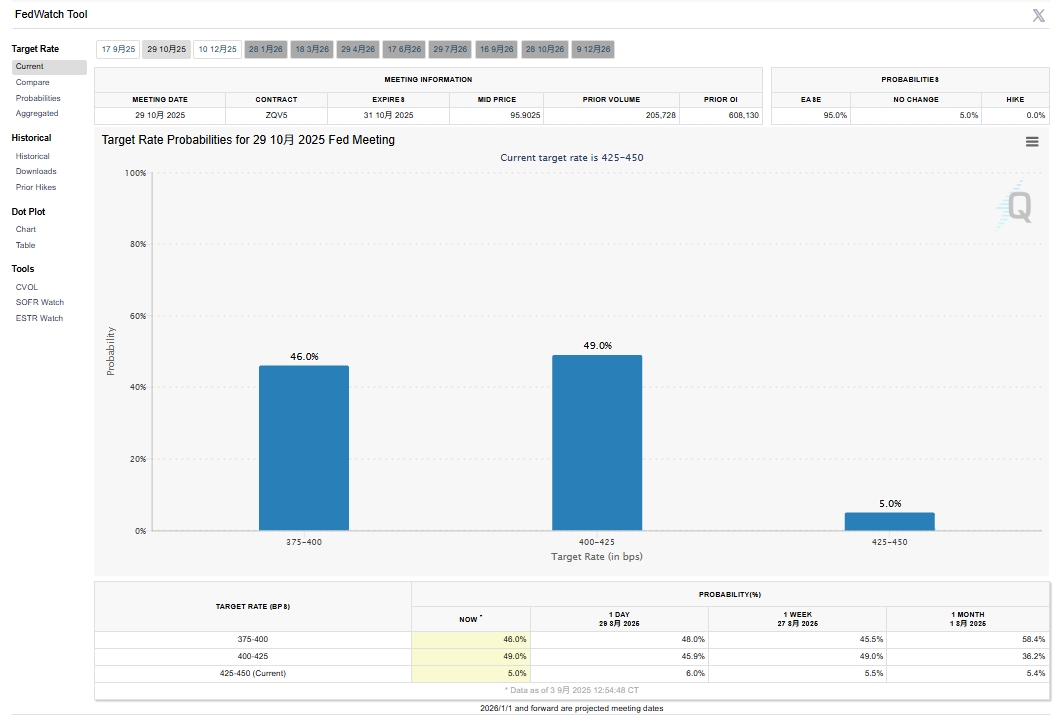

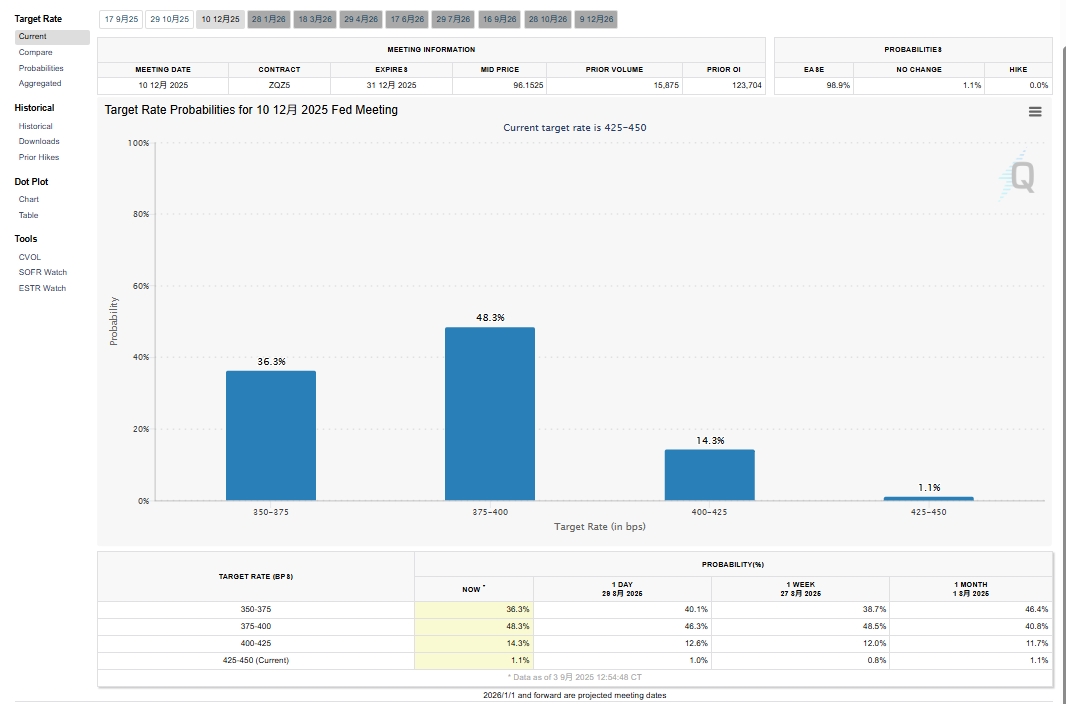

Data source: CME FedWatch Tool

Expectations for a September US Fed rate cut grew stronger. According to the latest CME FedWatch data, the probability of a 25bp cut in September reached 89.7%, followed by a 46% chance of another 25bp cut in October and 36.8% in December. Market bets on a September rate cut were strongest, benefiting precious metals and risk assets. Gold hit new highs, while copper followed the rally, breaking through the 80,000 yuan/mt mark during the night session on September 2 and reaching 80,700 yuan/mt on September 3. LME copper peaked at $10,038/mt, while the SHFE copper import arbitrage loss widened from the 100-200 yuan/mt range to 300-400 yuan/mt. Although sentiment weakened after copper prices breached 80,000 yuan/mt, why did the market remain confident in positioning for higher prices in September and beyond? Beyond macro tailwinds, fundamentals also played a role.

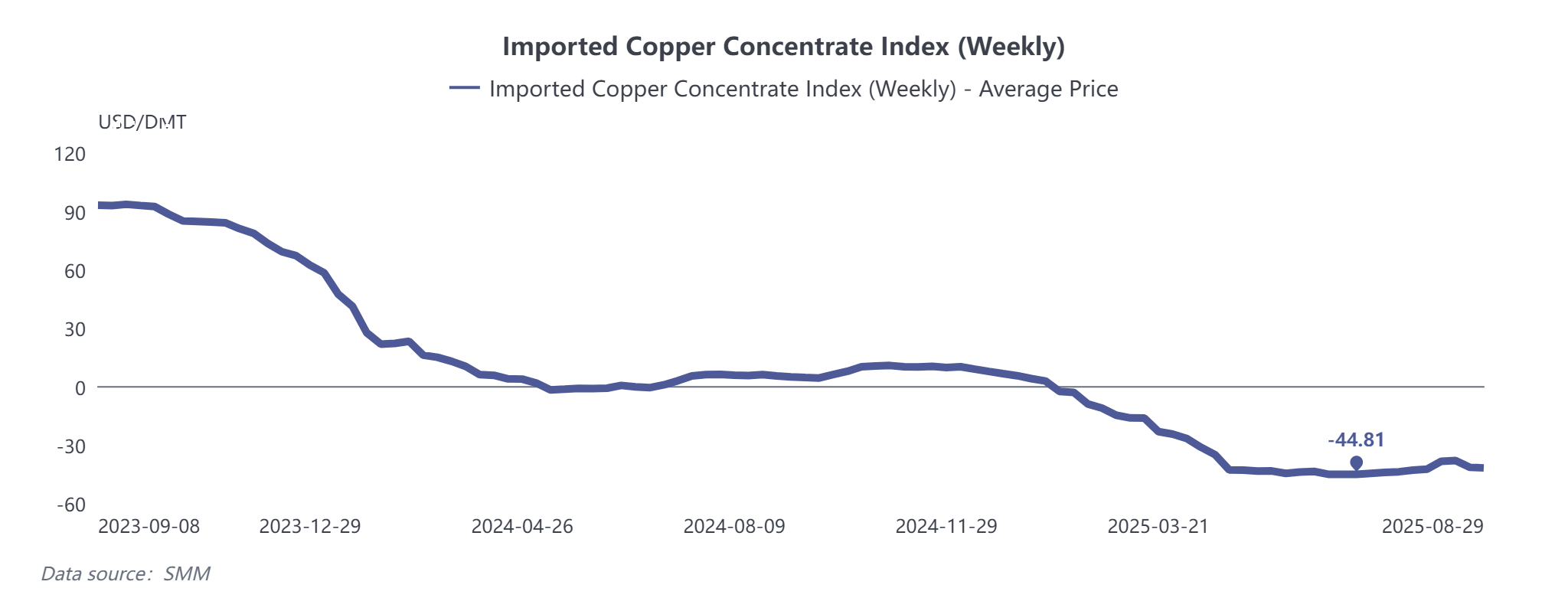

Copper Concentrates: The tight balance persisted. Although TCs briefly rebounded due to Grasberg’s inventory clearance, they fell again by over $40/dmt after the clearance ended and BHP’s tender price was finalized, with further downside risks.

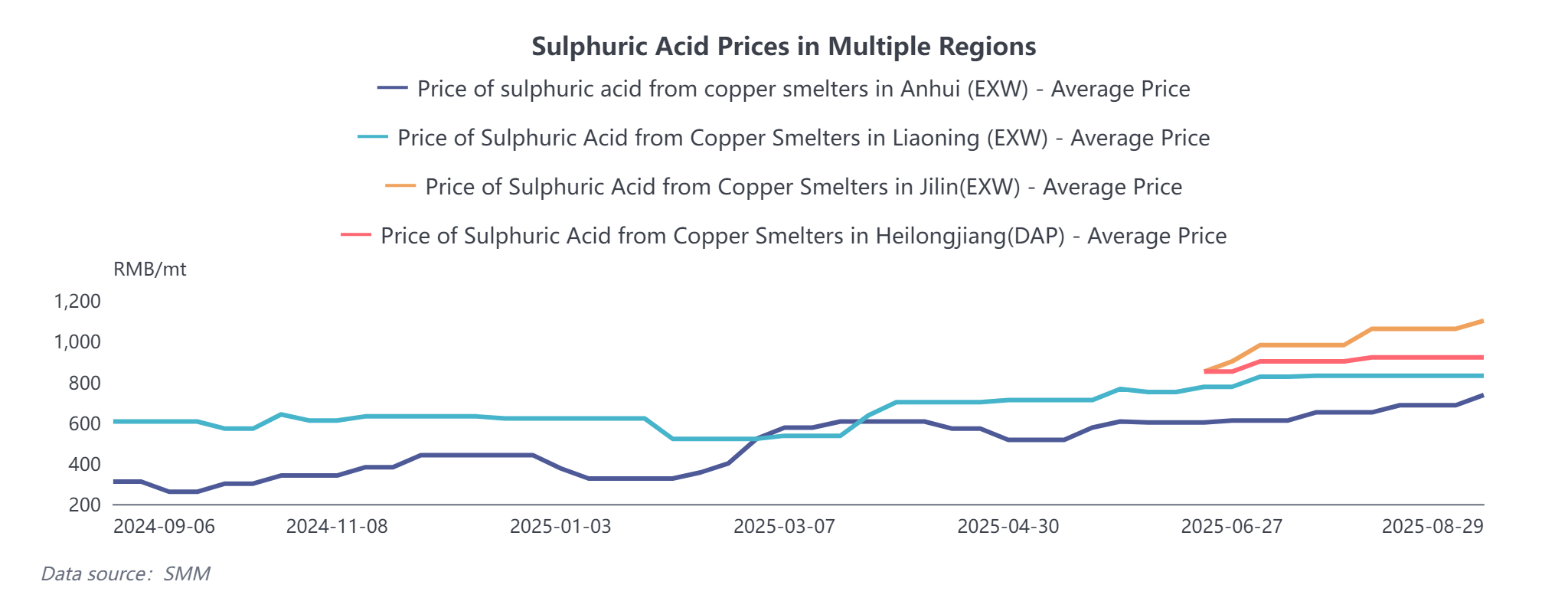

Sulphuric Acid: Rising sulphur prices pushed up smelting acid prices, keeping smelter by-product revenues relatively healthy and offsetting some smelting losses.

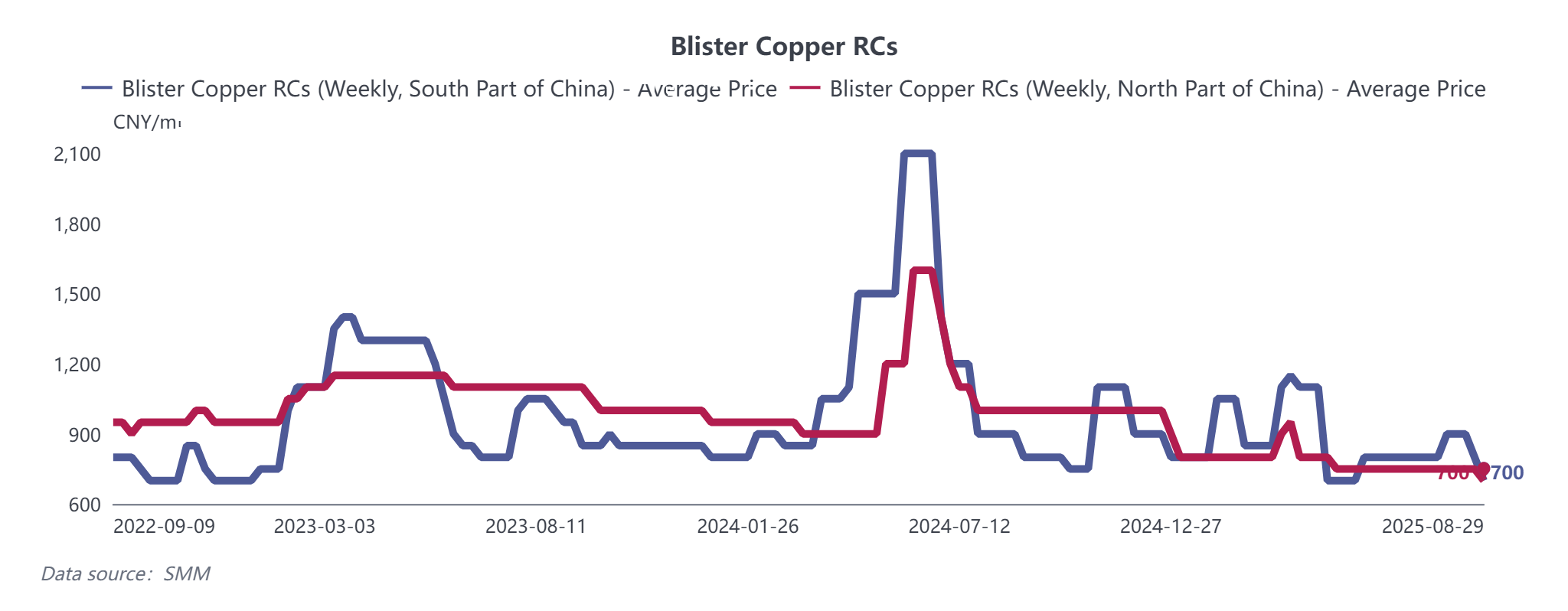

Copper Anode: Affected by the aforementioned No. 770 policy, scrap-derived copper anode and copper cathode faced disruptions. As of August 29, SMM’s weekly blister copper RCs in south China fell by 100 yuan/mt WoW, while north China RCs dropped by 50 yuan/mt WoW. Domestic anode plate processing fees also declined by 100 yuan/mt WoW. While most long-term contracts in September can be delivered as usual, scrap-derived anode copper will continue to feel policy impacts.

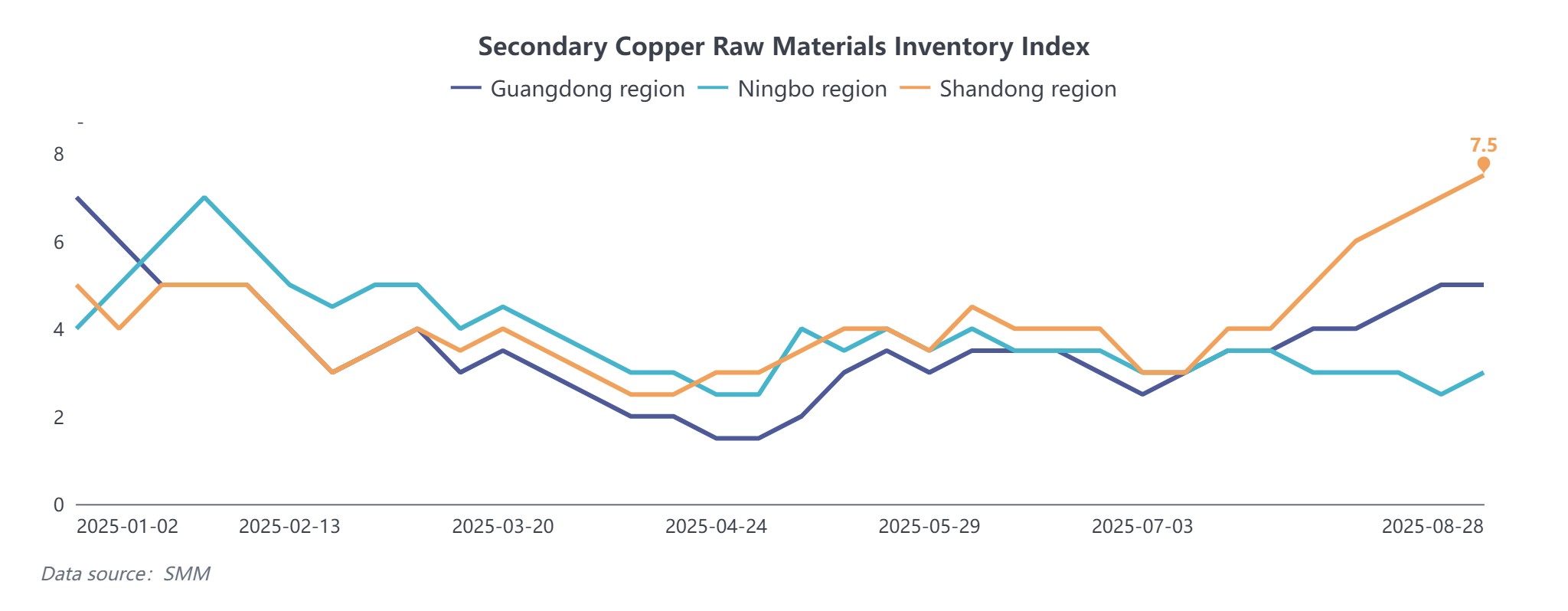

Secondary Copper: Policy adjustments, including investment promotion rollbacks and reverse invoicing, raised costs for secondary copper producers, with Jiangxi being the most affected. Operating rates for secondary copper rod continued to decline, while suppliers, anticipating higher prices, built inventories. SMM’s social inventory coefficient for recycled copper raw materials showed a recent increase. Due to tariffs, much imported secondary copper is routed through Japan, Malaysia, and Thailand. Cumulative secondary copper imports from January-July 2025 did not decline significantly, but rising smelting demand will keep the market tight.

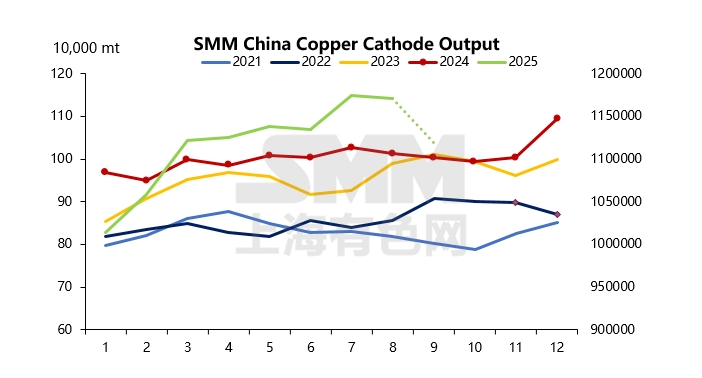

Copper Cathode: The above factors point to tighter smelter feedstock. Entering September, beyond scheduled maintenance, some smelters may cut production due to scrap copper shortages, reducing supply in Jiangxi and north China. As the traditional September-October peak season begins, consumption is expected to improve, though end-user demand varies: power > transportation > home appliances > real estate. Many market participants factor in import supplements, with imported copper arriving in mid-to-late August after the arbitrage window opened. However, import data shows over 60% of shipments are EQ copper. According to SMM data, China's copper cathode production in September is expected to drop by 52,500 mt (down 4.48% MoM). Even with import supplements, the deliverable supply may decrease, potentially leading to an expanded BACK structure ahead of the delivery date in September.

Considering these factors, copper prices still have room to rise amid macro and supply-side narratives as consumption is expected to enter the peak season. However, once prices exceed 80,000 yuan/mt, downstream new orders and cargo pick-up speed may face further pressure. Resistance is anticipated if prices surge above 81,000 yuan/mt.