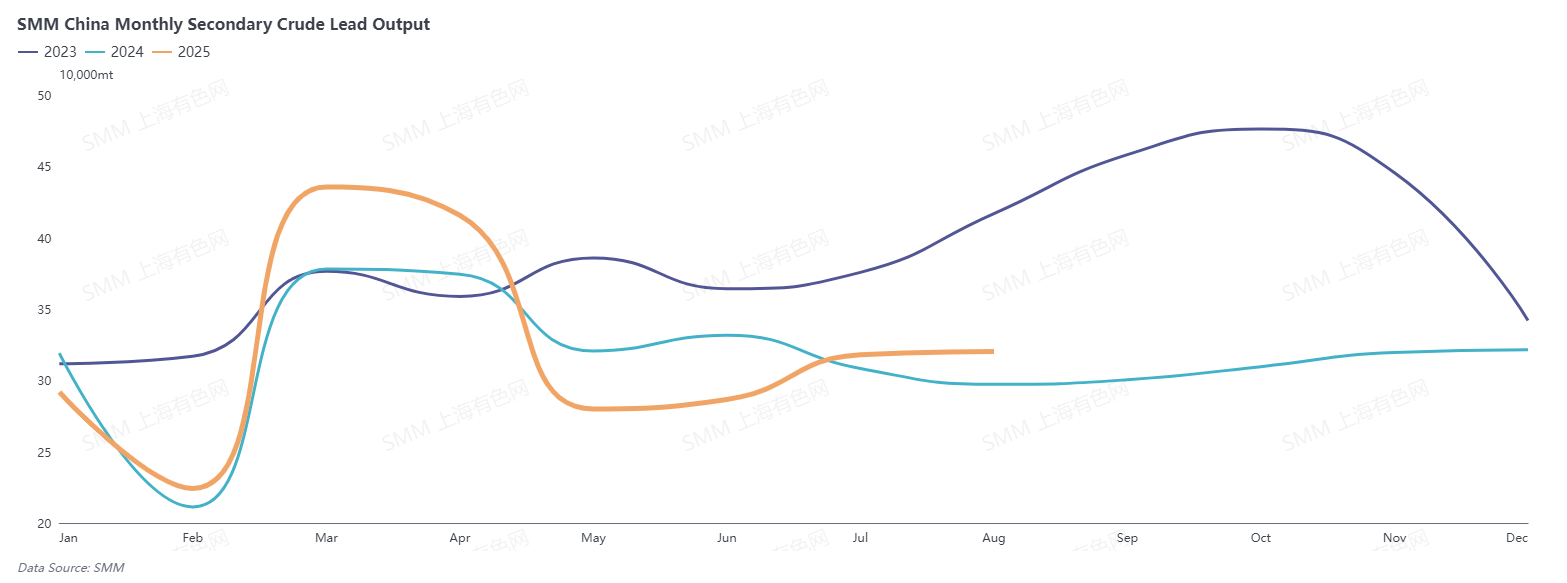

August 2025 secondary-lead output disappointed, edging up just 0.71 % month-on-month and 7.73 % year-on-year; secondary refined lead actually fell 3.54 % MoM, although it remained 1.98 % above last year's level.

The modest rise in total secondary output was driven by two factors:

A crude-lead smelter in Central China restarted after scheduled maintenance.

An East-China crude-lead plant that had recently resumed operations continued to run erratically, adding only marginal tonnes.

Refined-lead production, however, lost ground because closures outweighed restarts:

• Closures & cutbacks – Tight scrap-battery supply and heavy losses forced most smelters in East and North China to slash or suspend operations; a Southwest-China plant stopped mid-month after equipment failure. Total loss > 40 000 t.

• Restarts & ramp-ups – A large smelter in Inner Mongolia and a mid-tier plant in Anhui came back on line in late July and reached steady rates in August. A new secondary-lead project in Southwest China also released first tonnes, and a major Jiangxi producer restored full output as scrap arrivals improved. Combined gain ≈ 30 000 t.

September outlook

Several large East- and North-China smelters still plan to cut September output, citing weak end-demand and a bearish lead-price outlook. Scrap flows may tighten further during the 3 September military parade in North China, delaying raw-material restocking until mid-month. SMM expects refined secondary-lead output to drop by roughly 40 000 t MoM.