SMM News on August 8:

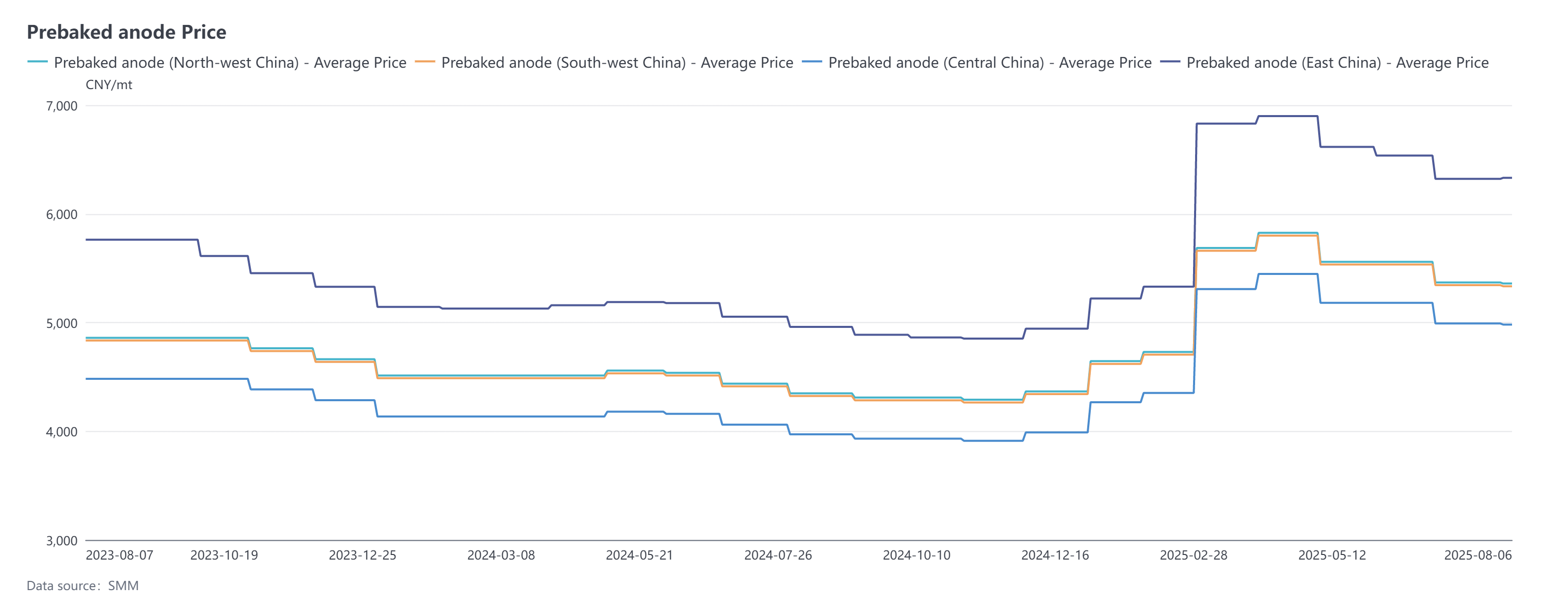

During the period from July 7 to August 6, SMM prebaked anode prices showed slight divergence but overall remained relatively stable. The benchmark procurement price for August 2025 at an aluminum plant in Shandong was 4,739 yuan/mt, down 0.21% MoM. According to SMM, export order prices for prebaked anode in August remained stable with minor fluctuations, with adjustments concentrated within $10/mt. As of now, SMM anode prices in east China closed at 4,739-7,924 yuan/mt.

Raw material side: Both petroleum coke and coal tar pitch markets performed moderately during this period. In the petroleum coke market, low-sulphur petroleum coke stood out notably: driven by active purchases from the anode material sector, refinery shipments maintained a favorable trend. More crucially, some refineries in north-east China have confirmed maintenance plans, fueling market expectations of supply contraction. Multiple positive factors combined to drive continuous price increases for low-sulphur petroleum coke. SMM data shows that as of now, the average price of low-sulphur coke in north-east China reached approximately 3,877 yuan/mt, up 5.72% from July 7. The sustained rise in low-sulphur coke prices transmitted to local refinery petroleum coke, which also strengthened: downstream enterprises showed heightened purchasing enthusiasm during the period, improving refinery shipments and pushing petroleum coke prices upward. Entering August, trading activity in the petroleum coke market remained robust, with downstream procurement enthusiasm staying at moderate levels, providing some price support from the demand side. Data indicates that as of August 6, the average price of local refinery petroleum coke stood at 2,428 yuan/mt, up about 8.39% from July 7. In the coal tar pitch market, rising coal tar prices during this period provided strong support for coal tar pitch price increases, driving its upward trend. SMM data shows that as of August 6, the average coal tar pitch price reached 3,987 yuan/mt, up 13.36% from July 7. Overall, cost support for prebaked anode persists.

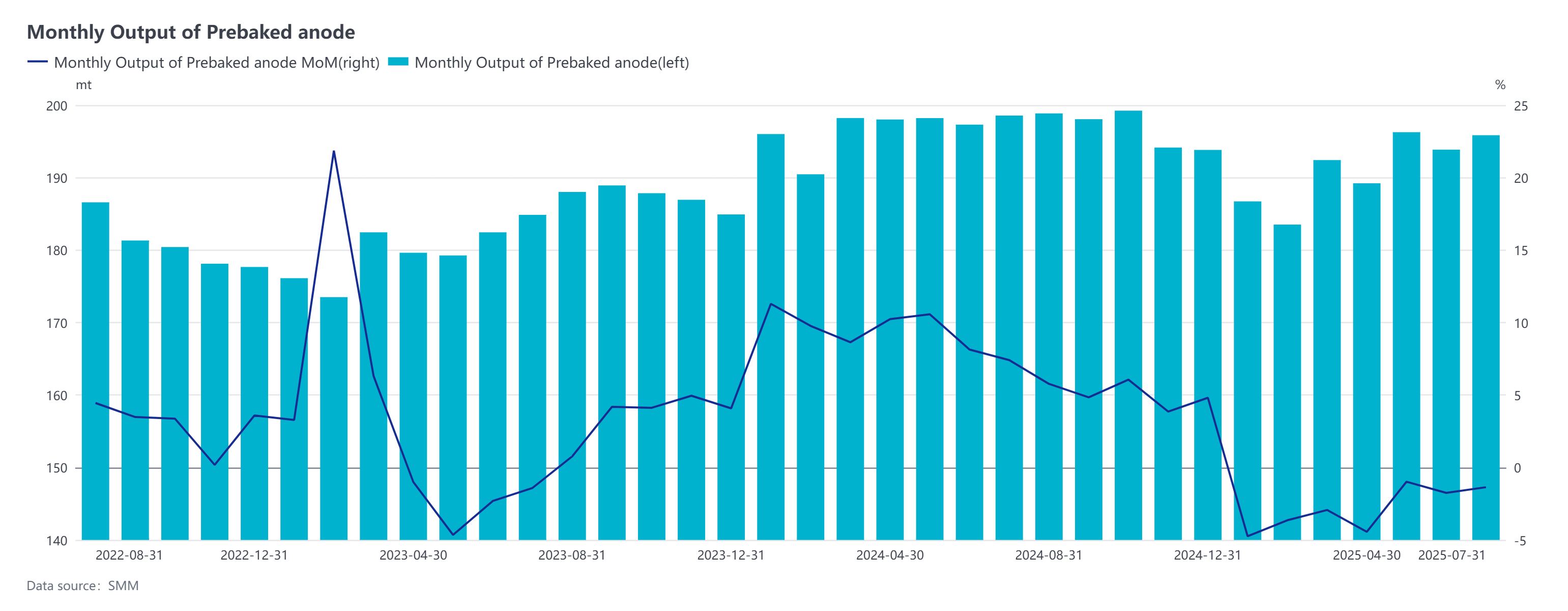

Supply side: Prebaked anode enterprises produced according to orders. In July 2025, most domestic prebaked anode enterprises maintained stable operations. Capacity release showed multiple positive trends: some enterprises resumed normal production after maintenance, with output gradually rebounding; select enterprises enhanced production efficiency through technical upgrades, further boosting output growth; new projects in south-west China commenced smooth operations, strengthening supply capability. Additionally, July had one more production day than June, providing some support to overall industry output. However, certain constraints existed on the supply side: due to the relocation of aluminum capacity from Shandong to Yunnan, some local prebaked anode enterprises saw minor output declines as supporting orders decreased. Meanwhile, strategic adjustments led to slight production reductions at some enterprises in north-west China. Overall, SMM data shows July prebaked anode production reached 1.9585 million mt, up 1.03% MoM, with industry operating rates remaining above 75%. This high operating level primarily benefited from strong domestic and international order performance.

From the demand perspective, influenced by the successful start-up of the Phase II replacement project for electrolytic aluminum in Shandong-Yunnan and the resumption of production from small-scale technological transformation capacities in Chongqing in the earlier period, the operating aluminum capacity in China increased slightly MoM in July, with production showing a dual increase of 1.05% YoY and 3.11% MoM. Entering August, the operating aluminum capacity in China continued to maintain a high level. The second batch of replacement projects in Yunnan has been completed and put into operation, achieving stable output, driving a further rebound in the industry's operating rate. The domestic demand side for prebaked anodes performed well. In terms of export orders, the overall performance of prebaked anode export orders in 2025 was good. This was mainly due to the continuous release of new capacities in the overseas electrolytic aluminum market, coupled with the gradual recovery of capacities in some enterprises, driving an increase in overseas demand for prebaked anodes. From the export data in the first half of 2025, exports have shown an increase compared to the same period last year. According to customs data compiled by SMM, as of now, the cumulative export volume of prebaked anodes in China in 2025 has reached 1.056 million mt, up 6.78% YoY. It is noteworthy that negotiations for export orders in 2026 have already commenced. From the current order negotiation situation, the overall order performance for 2026 is positive, with an expected increase in total export volume, mainly concentrated in the South Asian and Southeast Asian markets. Overall, the prebaked anode market in 2025 has demonstrated strong growth resilience under the dual demand support from domestic and overseas markets.

Brief Commentary: A certain aluminum enterprise in Shandong has adjusted the benchmark tender price for prebaked anodes in August 2025, decreasing it by 10 yuan/mt MoM. Meanwhile, a large domestic prebaked anode sales company has raised its sales pricing, with a MoM increase of 34 yuan/mt. The price center of raw materials has generally shifted upwards during this period, and the cost support for prebaked anodes remains relatively strong. According to SMM data, as of August 6, the comprehensive cost of prebaked anodes in China has risen to 4,921 yuan/mt, an increase of 3.65% compared to July 7. If calculated based on a one-month production cycle, the profitability of the prebaked anode industry is slightly under pressure, with a theoretical profit decrease of approximately 125 yuan/mt MoM, and most prebaked anode enterprises have experienced a contraction in their profitability status. The current operation trend of the raw material market is good, providing certain support for prebaked anode prices. Especially for petroleum coke, its downstream demand side is generally moderate, with the carbon industry maintaining a just-in-time procurement rhythm, while the demand for petroleum coke in the anode material market also continues to exist. Based on a comprehensive assessment of multiple factors, there is an expectation for an upward shift in the price center of petroleum coke in August. Under this background, directly supported by the increase in raw material prices, the price trend of prebaked anodes is expected to stabilize and rise.