On June 22, 2025, following US airstrikes on three Iranian nuclear facilities, Iran’s parliament approved a proposal to block the Strait as retaliation, instantly escalating regional risks. The US responded with a firm warning, pointing out that Iran’s own oil exports rely heavily on this passage—and that any move to close it would be self-destructive.

How likely is a blockade?

The Strait of Hormuz is an important shipping lane for global oil and raw materials trade, with approximately 20% of the world's oil supply passing through it on its way to destinations around the world. While threats to close the strait have surfaced repeatedly over the past four decades—most notably during the Iran-Iraq War in the 1980s, island disputes in the 1990s, and periods of heightened tension in 2008, 2012, 2018, and 2019—Iran has never actually carried out a full closure, even under severe external pressure or sanctions. This pattern highlights that Iran’s blockade threats are often used as a bargaining chip during episodes of economic or geopolitical confrontation, but rarely translate into action.

Most analysts believe a full and prolonged blockade remains less than a 50% probability. More probable are targeted disruptions, such as laying mines or ship inspections, which could slow shipping and drive up freight costs to some extent. With the US Fifth Fleet based in Bahrain, any drastic move by Iran would almost certainly provoke a military response. As a result, markets see a full closure as a “last resort,” but the risk alone has clearly heightened uncertainty.

In short, while the aluminium sector is far less exposed than oil, the primary risk lies in short-term market volatility and potential supply chain disruptions, not in a prolonged, systemic crisis.

If it happened, what would it mean for global aluminium trade flows?

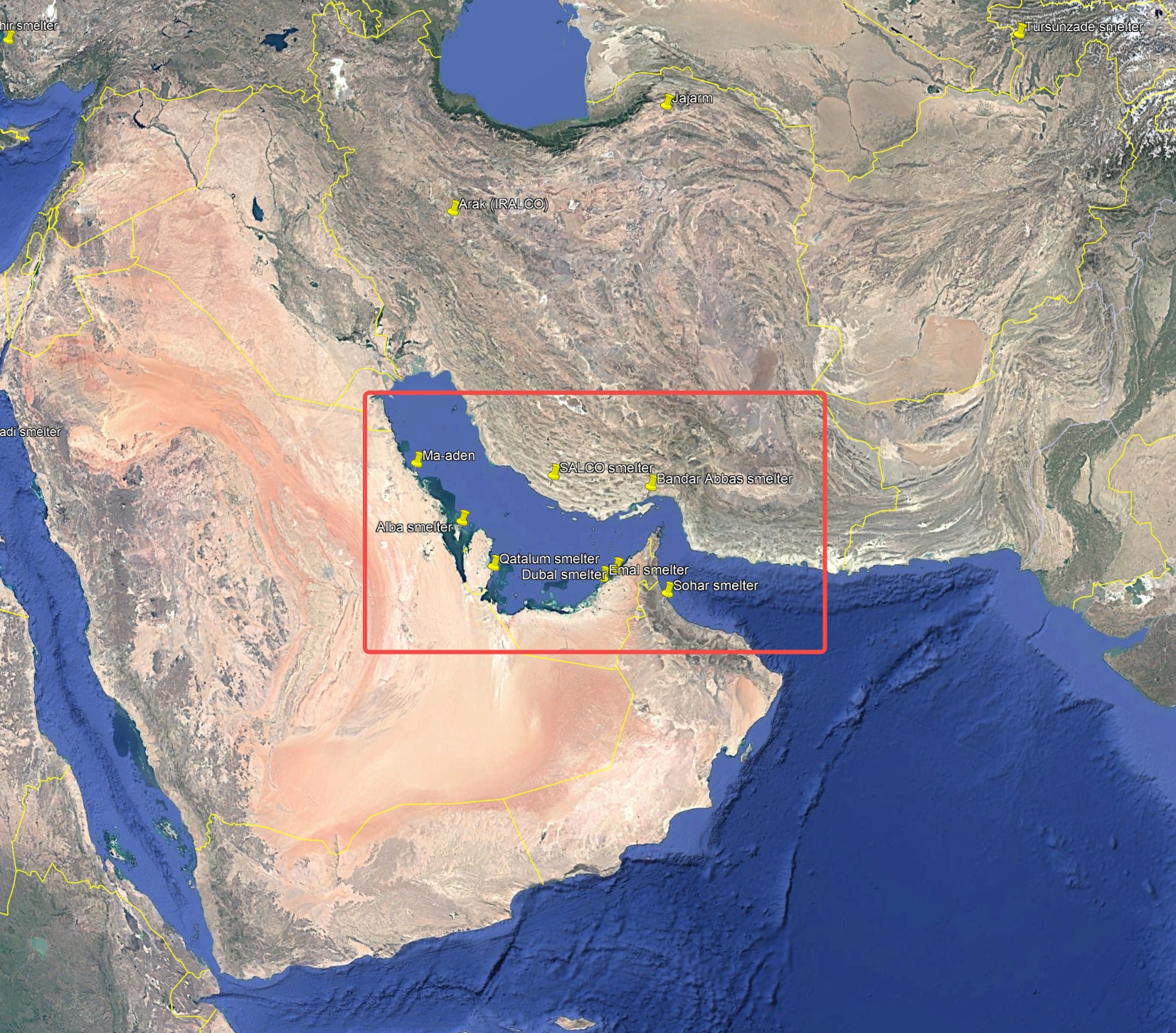

Countries in the Middle East (the GCC, Iran, etc.) collectively account for around 23% of global primary aluminium production (with an annual capacity of approximately 6.92 million tonnes). Most of the region's smelters are located near the Persian Gulf and depend on the Strait of Hormuz for export routes (Fig. 1). In 2024, these countries exported 5.14 million tonnes of primary aluminium, accounting for nearly 75.2% of total production. If the Strait of Hormuz were to be blocked, these countries' aluminium exports would be cut off immediately as there are almost no alternative shipping routes with equivalent capacity. Inventories would build up, forcing smelters to cut production and disrupting raw material imports — putting a double squeeze on output.

Fig.1 Most of smelters in Middle East concentrated near the Persian Gulf

Asian Countries like Japan, South Korea, and other major Asian economies rely partly on aluminium shipments from the Middle East. If supply is interrupted, they’ll need to scramble for replacements, such as from Russia , India or SEA, or even source aluminium semis from China. But logistical bottlenecks and short-term shortages will likely push regional premiums higher.

China produces nearly 60% of the world’s primary aluminium and is largely self-sufficient, exporting semi-finished products in recent years. China’s direct reliance on Middle Eastern aluminium is minimal. The main impact would come via global price transmission—any rally in international prices would be quickly felt on the SHFE, but domestic supply would remain stable.

The main risk occurred in Europe. Europe is highly dependent on aluminium imports, with the Middle East supplying about 1.2 million tonnes in 2023 (18.8% of total EU imports). If Middle Eastern metal is cut off—especially with the Russian supply already restricted—Europe would face a notable supply gap. The region would have to seek more shipments from India, Africa, or Canada, increasing both significant transport costs and logistical risk for local processors and manufacturers.

While the US mainly imports aluminium from Canada, the Middle East still accounted for about 16.3% of US primary aluminium imports—nearly 640,000 tonnes in 2024. Any disruption, especially when combined with tariff pressures, would force US buyers to draw down inventories and increase purchases from Canada and Latin America, raising costs and causing short-term volatility in the US market.

How could a blockade impact bauxite and alumina supply chains?

Once the Strait is blocked, the impact on aluminium ingot exports is immediate. However, for raw materials, smelters generally maintain inventory reserves of around 1-2 months, so if the disruption is only short-term, which is highly likely, the trade flow risk for bauxite and alumina is lower than that for aluminium ingots.

Middle Eastern smelters are highly dependent on imported bauxite and alumina. The region’s annual alumina capacity (4.95 million tonnes) falls far short of its aluminium output, and there are virtually no local bauxite resources. Raw materials are mostly sourced from Guinea, Australia, and Brazil. If the strait is blocked, imports would stall, and some refineries could face forced shutdowns. If West African bauxite vessels are forced to detour around the Cape of Good Hope, transport times and costs will rise sharply.

By contrast, China and the rest of Asia are less directly exposed. China’s bauxite import routes run through the Pacific and Indian Oceans, not the Strait of Hormuz, and sources are diverse. China is also largely self-sufficient in alumina and is a small net exporter. Globally, most bauxite shipped from Guinea to Asia takes the southern route, which would remain open. While oil price spikes and higher freight insurance could raise costs, most bulk carriers operate on long-term contracts, making the impact manageable. If Middle Eastern demand drops, other regions could even see easier supply, partially hedging cost increases.

How will aluminium prices react according to the scenarios?

On June 23, aluminium prices on the London Metal Exchange jumped sharply, with the three-month contract reaching a three-month high of $2,636 per tonne—an intraday surge of nearly 4%. In the near term, heightened geopolitical risks are fueling risk premiums and increased volatility, leading to pronounced swings in aluminium prices.

Looking ahead, much will depend on how the situation in the Strait of Hormuz evolves. In a worst-case scenario, a prolonged blockade could remove around 23% of global aluminium supply, likely pushing prices significantly. However, most analysts consider this outcome unlikely, as both the US and Iran are incentivised to avoid a full-scale escalation.

More likely is a scenario where the crisis falls short of a full blockade and trade flows recover after temporary disruption, allowing prices to gradually realign with fundamentals. Although visible inventories are still low, global supply remains generally sufficient, and soft demand amid macroeconomic headwinds should continue to weigh on the market. If geopolitical tensions ease, prices could correct or even turn lower.

It’s also important to note that the impact on regional aluminium premiums will vary. European premiums are expected to rise faster and further than those in Asia, given Europe’s heavy reliance on Middle Eastern supply and limited alternatives, whereas Asian markets benefit from more diversified sources. In the US, despite the loss of Middle Eastern shipments, the existing 50% import tariff on aluminium already supports historically high Midwest premiums, leaving less room for additional increases. According to SMM estimates last week, Rotterdam duty-paid premiums stood around $195–215 per tonne, while US Midwest premiums surged past $1,220 per tonne after the tariff hike.

Another factor to watch is the movement of oil prices. Higher energy costs would raise both production and transport expenses for aluminium smelters worldwide, further pressuring margins and potentially lifting delivered aluminium prices over the medium term.

In summary, the Strait of Hormuz crisis is acting as a geopolitical catalyst for aluminium prices, driving short-term volatility and trade flow disruptions. The global aluminium supply chain—outside the Middle East—is highly adaptable and resilient. Unless the crisis spirals out of control, the industry is unlikely to see a systemic supply shock on par with oil. Industry players should closely monitor Middle East developments but avoid overestimating the risk to long-term price trends. While an extreme scenario could send prices soaring, the most likely outcome is a period of elevated volatility, followed by a return to more stable, fundamentals-driven trading.

Author: Cathy Liu, Aluminium market analyst | SMM UK Office | cathyliu@smm.cn