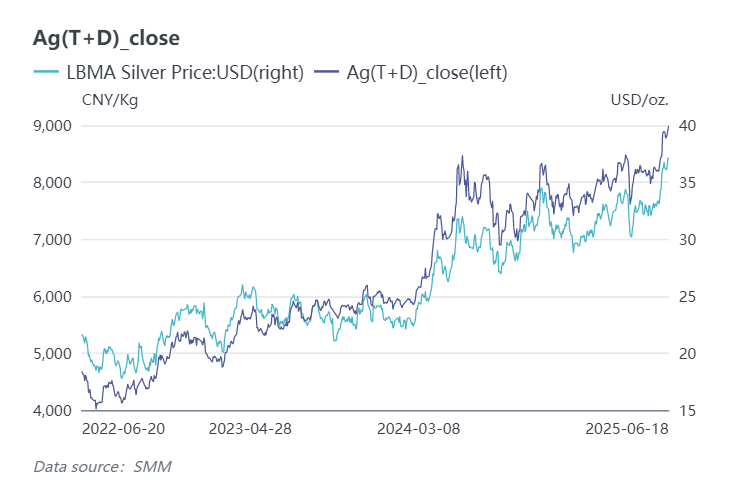

I. Silver Prices Reach New Highs, with Domestic Silver (T+D) Surpassing the 9,000 yuan/mt Target

This week, silver prices surged sharply after a pullback, contrasting with gold's fluctuating performance. Domestic and overseas silver prices strengthened in tandem, attracting significant bullish capital inflows. On Wednesday, SGE Ag (T+D) prices hit a new high of 9,040 yuan/mt, while silver prices on the London Bullion Market Association (LBMA) broke through the key target of $37/oz.

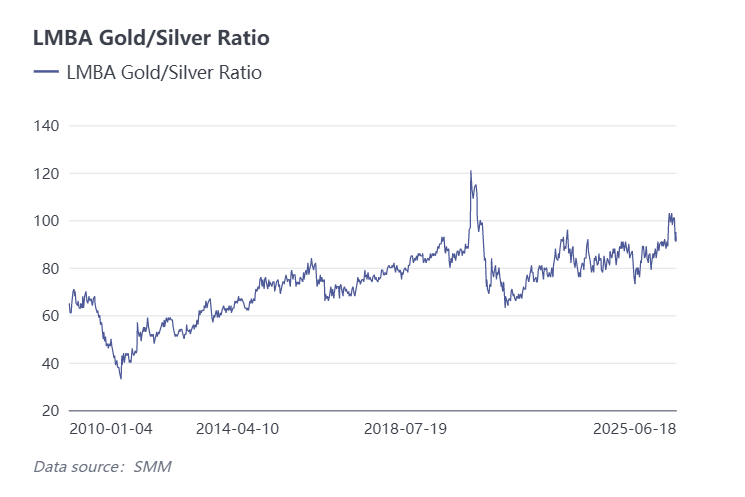

II. Gold-Silver Ratio Corrects, with Silver Emerging as a Safe-Haven Alternative

The escalation of conflicts between Israel and Iran this week heightened market risk aversion. With gold prices consolidating at high levels, undervalued silver emerged as a safe-haven alternative for capital. As silver was not simultaneously allocated during previous rounds of gold price increases, the gold-silver ratio corrected after recent stagnation in gold prices and silver's breakthrough of key resistance levels. This shift highlighted silver's speculative nature, boosting bullish sentiment.

Silver possesses triple attributes—financial, industrial, and speculative—each capable of driving price increases under specific conditions. When speculative attributes dominate, silver prices rise while the gold-silver ratio falls; when industrial demand takes precedence, silver prices rise while the gold-silver ratio continues to decline; when financial attributes prevail, both silver prices and the gold-silver ratio rise simultaneously.

Regarding economic data and interest rate cut expectations, the market generally anticipates that the US Fed will maintain its interest rate range at 4.25%-4.50%. Despite the Fed's hints of increased stagflation risks, the market still expects two interest rate cuts this year. Investors will closely monitor Fed Chairman Powell's remarks following policy decisions for signals on future monetary policy. Currently, market expectations for Fed easing in H2 have risen, with silver prices expected to maintain a medium- and long-term bullish trend in this context.

III. Spot Market Transactions and Inventory Conditions

In the consumer market, the end-use consumption market weakened in June. Rising silver prices prompted some enterprises to adopt silver-reducing formulations or alternative technologies to cut costs. Despite weakening downstream consumption demand and most suppliers transferring inventories for delivery in June, domestic spot inventory growth remained relatively limited. This was primarily due to smelters' export ratios increasing or remaining unchanged from May amid an open export window. Following silver price increases, downstream clients primarily picked up goods through long-term contracts, making only minor purchases at price lows or in response to urgent needs. In late June, the spot-futures price spread widened again, with the premium for Shanghai's national standard silver TD rising, though most purchases were made by traders. Downstream demand remained cautious, with overall spot market transactions remaining sluggish.

IV. Market Outlook

In summary, silver is expected to continue reaching new highs in June 2025, driven by safe-haven and speculative demand. Although short-term pullbacks may occur due to profit-taking, the medium- and long-term upward trend in silver prices remains intact. Bullish sentiment persists, coupled with the need for gold-silver ratio correction, suggesting that silver prices may continue to fluctuate upward in H2, challenging new highs once again.

Bulls in the silver market are restless as the gold-silver ratio recovers. Can silver prices reach new highs after a high-level correction?

This week, silver prices surged sharply after a pullback, contrasting with gold's fluctuating performance. Domestic and overseas silver prices strengthened in tandem, attracting significant bullish capital inflows. On Wednesday, SGE Ag (T+D) prices hit a new high of 9,040 yuan/mt, while silver prices on the London Bullion Market Association (LBMA) broke through the key target of $37/oz.

Data Source Statement: Except for publicly available information, all other data are processed by SMM based on publicly available information, market communication, and relying on SMM‘s internal database model. They are for reference only and do not constitute decision-making recommendations.

For any inquiries or to learn more information, please contact: lemonzhao@smm.cn

For more information on how to access our research reports, please contact:service.en@smm.cn

Related News

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

Feb 6, 2026 17:46

This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]

Read More

This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]

Feb 6, 2026 17:46

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)

Feb 6, 2026 12:00

Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]

Read More

Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]

Feb 6, 2026 12:00

Feb 6, 2026 09:27

A gold and silver reset, not a reversal

Read More

A gold and silver reset, not a reversal

Gold and silver have recovered part of their recent losses following one of the sharpest corrections seen in precious metals in over a decade

Feb 6, 2026 09:27

Related News

This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]

Feb 06, 2026 17:46

Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]

Feb 06, 2026 12:00

A gold and silver reset, not a reversal

Feb 06, 2026 09:27

Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]

Feb 05, 2026 17:36