SHANGHAI, Sep 26 (SMM) - As an important supplement to the raw materials for lithium battery, lithium battery scrap has become a "sweet pastry" in the market in recent years under the background of the increasingly prominent contradiction between raw material supply and demand. Especially since entering the third quarter, both the discount rates and prices have been moving all the way up.

For the frenzying increase in discount rates and prices in recent months, SMM believes that it is the combined effect of the imbalance between supply and demand as well as the outdated pricing scheme:

- Supply and demand imbalance: Lithium battery recycling has not reached scale production yet, hence the supply growth is limited despite great attention from industrial players. New and existing players have been ramping up the production capacity, and the shortage of scrap has greatly driven up the prices;

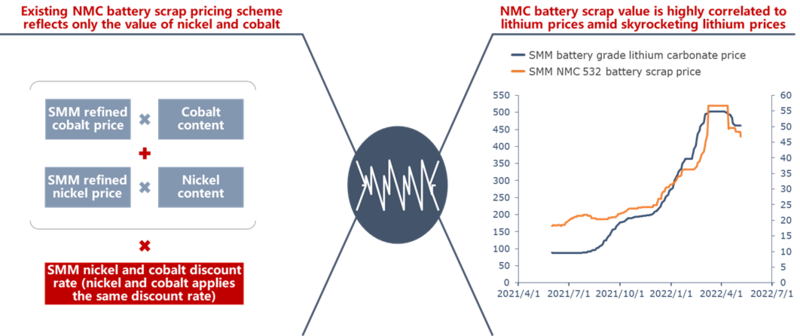

- Outdated pricing scheme: Lithium has become the most important metal to be recovered from the scrap, but it is not priced separately, creating a "grey zone" for value accounting in addition to the fact that the pricing of nickel and cobalt is based on metals prices (refined nickel and refined cobalt), while the final product is salt, resulting in miss-valued recovered products.

The imbalance between supply and demand is the main driving force behind the increase in scrap discount rates and prices:

1.1 In terms of supply, the shortage is mainly caused by “in-plant circulation” of scrap, the lack of significant increase among recycling channels, and the repurposing of some battery scraps.

- "In-plant circulation" of scrap in battery factories: In the context of guaranteed supply of raw materials, in addition to strategic procurement of primary metals, battery recycling has also become a source of raw material supply that cannot be ignored. It is now common that top-tier battery companies are deeply bound with recycling companies through "subsidiary or joint venture", so as to create an "internal circulation model" of in-plant scrap, like CATL and Brunp Recycling (parent company and subsidiary), LG Energy Solution and Huayou Recycling (joint venture), BYD in-plant recycling system, etc. Based on this business model, the amount of scrap that actually circulates in the market has been reduced. And considering the scale of these leading battery companies, the supply reduction in terms of market circulation is quite significant.

- Lack of significant increase among recycling channels: The mainstream recycling channels can be divided into inter-production scrap (mainly contributed by battery companies) and end-of-life battery scrap (mainly contributed by end consumers). However, the inter-production scrap is basically recycled in-house, while the tide of end-of-life battery scrap has not yet come, so there is no obvious increase from the recycling channels. Although the Ministry of Industry and Information Technology issued a document in April this year to add crude nickel-cobalt hydroxide made from scrap as the industry standard, the actual import of scrap still encounters considerable obstructions, according to SMM research, so the expected increase in overseas imports is unlikely to pay off in the near term.

- Repurposing of some battery scraps: End-of-life batteries are still with use values, and under the policy of "prioritising repurposing before recycling", some battery scraps are applied to street lights, two and three-wheeled electric vehicles, energy storage and other terminals fields. Affected by the repurposing, the amount of scrap that can be recycled is relatively limited.

1.2 Secondly, on the demand side, new and existing lithium battery recyclers are actively expanding the production, resulting in a substantial increase in the overall demand for scrap.

- Existing lithium battery recyclers are significantly expanding their production: Based on the expectation of high growth in scrapping and recycling in the future on top of raw materials supply shortage (limited supply of raw materials at the mine end), existing lithium battery recyclers are actively expanding their recycling capacity. At the same time, high lithium prices have accelerated the commissioning of new LFP projects.

- Engagement of new players: As a "blue ocean market" favoured by the capital market, the lithium battery recycling market has attracted many new players. New players mainly consist of upstream and downstream players in the industry chain as well as cross-industry players. Upstream and downstream players in the industry chain (such as smelters, battery companies, and car companies) are more likely to take lithium battery recycling as an important measure to ensure their supply chain. The cross-industry players are aiming at the "high growth" expectation concerning lithium battery recycling, thus secure a better positioning in advance in order to obtain higher profits in the future.

The outdated pricing method fuels the current round of irrational rise in scrap prices

2.1 In the context of the "frenzy" lithium prices, lithium is becoming the metal with highest value among all recycled materials. However, in the current pricing scheme, lithium metal, which takes up the largest proportion, is not separately priced, resulting in a "grey zone" in the pricing process, and the pricing of lithium battery scrap becomes more and more confusing.

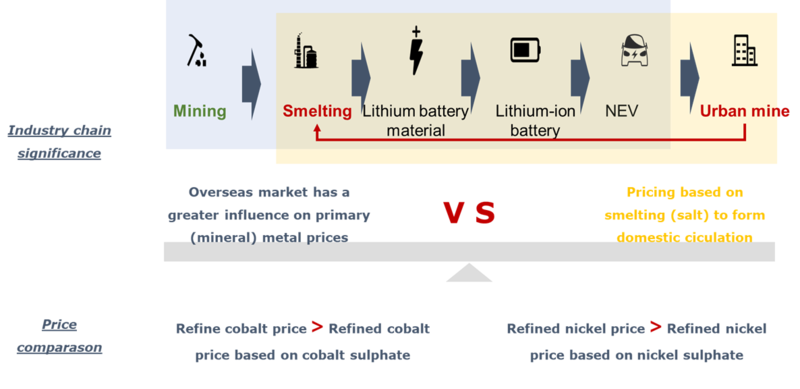

2.2 The improper benchmarking is also one of the driving factors for the irrational rise of scrap prices: The traditional lithium battery recycling pricing scheme is based on the price of primary metals (such as refined nickel and refined cobalt), but primary metal prices are set based on the supply and demand of traditional industries, and there is a difference with the supply and demand situation in the lithium battery industry. On the other hand, overseas market situation exerts strong influences on primary metals prices, which is contrary to the idea of "domestic circulation" in the lithium battery recycling industry.

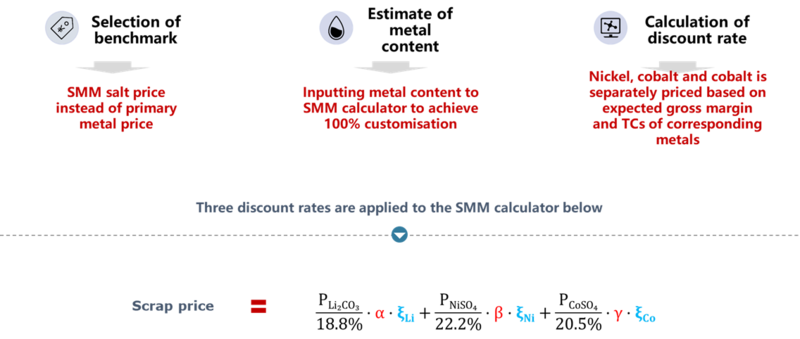

As a third party in the industry, SMM has always undertaken the responsibility and mission of mitigating the risk of price fluctuations and reducing transaction costs for the industry players. Therefore, SMM will launch a lithium battery scrap price calculator in the near future to solve above-mentions problems, in an effort to fundamentally address the dilemma of different metal content in different batches of battery scrap, and realise 100% customised pricing.

So, how to use SMM lithium battery scrap rice calculator in real scenarios?

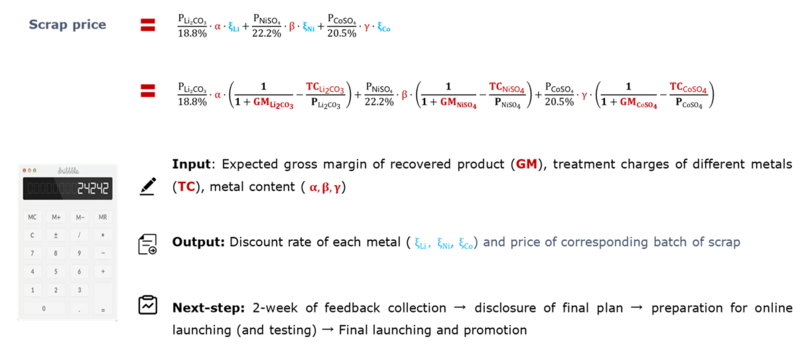

You need to input: the expected gross margin (GM) of the recovered product, the treatment charge for each metal recovered (TC), and the content of each metal in the corresponding batch of scrap (α, β, γ )

The calculator will output: discount rate of each metal (ξLi, ξNi, ξCo) and the prices of corresponding batch of scrap

SMM will conduct research and collect feedback with colleagues in the lithium battery recycling industry in the next 2 weeks, and finalise the calculation formula, and then prepare for online launching, which will be eventually released on the SMM website. So stay tuned.

![[Galan Lithium Announces Completion of Phase 1 Construction at HMW Project]](https://imgqn.smm.cn/usercenter/tKgKv20251217171725.png)