SHANGHAI, Apr 1 (SMM) - From July 20, 2021 to March 29, 2022, battery-grade lithium carbonate prices have achieved nearly nine months of continuous gains. On March 30, the average price of battery-grade lithium carbonate dropped for the first time this year, down 1,000 yuan/mt compared to the low on March 29, and stood high as a whole. And the overall average price fell 500 yuan/mt. The reasons behind the decline include more uncertainties at the terminal end, easing supply tightness, and sentiment to sell off. The tug-of-war across the entire industry chain has kept fulling down the bottom line, and the transaction range has expanded.

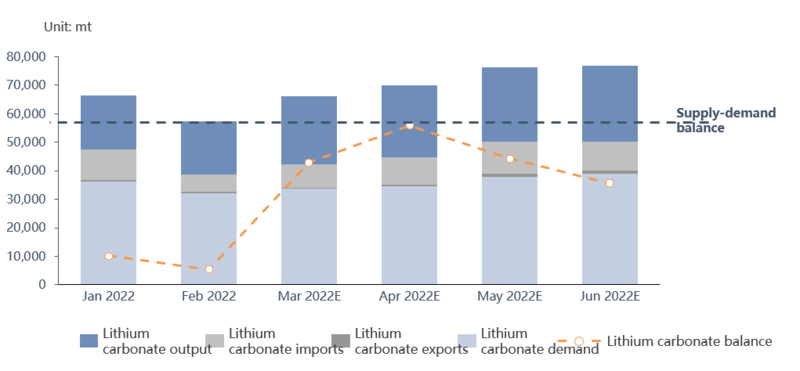

At this stage, the overall production of lithium salt plants has been normal entering March. And coupled with a rebound in brine lake output, the overall output in March rose significantly compared to February. At the same time, considering additional supply from imports, lithium carbonate supply climbed palpably. On the demand side, the second quarter is the traditional seasonal low for car sales, and the sales of some models has been halted due to cost pressure. What’s more, the broad price adjustment of the models has brought great uncertainties to future car sales. Although the car companies are currently making no significant changes to the battery orders, but it is still accompanied by a certain downside risk.

When it comes to the upstream battery sector, the in-plant battery stocks of battery manufacturers have already been high in January and February. And taking into account the possibility of falling battery orders from car companies, some battery companies choose to reduce their finished products and raw material inventories, as well as cathode material outsourcing, and stand wait-and-see. And when it goes even upward to cathode active materials (CAMs) sector, as the orders for April have basically been settled, the CAM orders may be flat or drop slightly. And as more and more material factories receive toll manufacturing orders, their demand for lithium salt will decrease.

In terms of supply and demand, the overall lithium salt supply and demand gap has been gradually narrowing since February, and the gas will be around 70 mt in April. As procurement urgency declines, and the downstream will have a say in pricing. However, the mainstream large plants still hold firm to their offers at 500,000-510,000 yuan/mt, while small ones may be willing to lower the quotations slightly. Nonetheless, the traders continue to force down the prices, and some materials factories are also selling off. As the price bottom line drops even lower, the overall market price range expands. The prices are expected to remain stable in the near future, accompanied by the risk of a small correction.

Looking forward, from the supply and demand side, the supply from spodumene will be limited for lack of ore, while that from mica will stabilise. As such, supplies from brine lake and imports will become the core driver of growth, but with limited upside potential. On the demand side, after the nickel price storm and terminal price hike, the outlook of car sales have turned promising again. And the material side will see rising orders. The supply shortage is expected to re-appear in May and June, which will offer momentum for lithium carbonate prices.