Main points of the report:

Since the end of February, the continuous warming of the geopolitical situation has led to increased concerns about the reduction of global crude oil supply, and crude oil prices have risen sharply in the short term, triggering market concerns about a new round of oil crisis. Oil crisis refers to the economic crisis caused by changes in oil prices. so far, there have been three recognized oil crises, which occurred in the 1970s (twice) and the 1990s (once).

The oil crisis directly affects the operating costs of various industries and has an important impact on the global economy. For copper, fuel and electricity costs account for 15% and 25% in upstream copper mining, and changes in oil prices determine upstream costs and profits to a certain extent; in addition, copper is more sensitive to economic changes. Economic changes before and after the oil crisis usually lead to major changes in the copper market. In view of this, this paper will analyze the impact of the three oil crises on the copper market.

Through the full-text analysis, it is concluded that the oil crisis has the following effects on the copper market: 1. During the oil crisis, copper prices will rise and fall to a certain extent with the rise and fall of oil prices, and the performance of copper prices is relatively stagnant in the early stage of oil price rise, and copper prices tend to be stronger in the later stage of oil price rise. 2. During the oil crisis, both the macro-economy and the supply and demand of the copper market experienced a process of changing from strong to weak, and the change of supply and demand was mainly reflected in following the change of macro-economic demand. 3. During the oil crisis, the market risk sentiment was impacted to varying degrees, and the impact weakened one by one.

Since the end of February, the continuous warming of the geopolitical situation has led to increased concerns about the reduction of global crude oil supply, and crude oil prices have risen sharply in the short term, triggering market concerns about a new round of oil crisis. Oil crisis refers to the economic crisis caused by changes in oil prices. so far, there have been three recognized oil crises, which occurred in the 1970s (twice) and the 1990s (once).

The oil crisis directly affects the operating costs of various industries and has an important impact on the global economy. For copper, fuel and electricity costs account for 15% and 25% in upstream copper mining, and changes in oil prices determine upstream costs and profits to a certain extent; in addition, copper is more sensitive to economic changes. Economic changes before and after the oil crisis usually lead to major changes in the copper market. In view of this, this paper will analyze the impact of the three oil crises on the copper market.

Review of the three oil crises

The three worldwide oil crises occurred in 1973, 1978 and 1990, respectively. The factors and results are as follows:

(1) the first oil crisis: the trigger was the fourth Middle East War in October 1973, when oil exporting countries decided to reduce oil production in order to attack Israel and its supporters, and imposed an oil embargo on Western countries. In December, the Arab members of OPEC raised the price of benchmark crude oil from $3.011 to $10.651 per barrel. As a result, from October 1, 1973 to January 1, 1974, the international oil price rose from US $3.11 to US $11.65 per barrel, which seriously impacted the economic growth of industrialized countries.

(2) the second oil crisis: caused by the change of political situation in Iran and the outbreak of the Iran-Iraq war at the end of 1978, global oil production plummeted from 5.8 million barrels per day to less than 1 million barrels per day. As a result, from 1979 to 1980, the international oil price soared from US $13 to US $34 per barrel, which became an important reason for the overall economic recession in the West.

(3) the third oil crisis: the triggering factor was Iraq's occupation of Kuwait in August 1990 and the disruption of crude oil supply due to Western economic sanctions. As a result, in the third quarter of 1990, the international oil price rose sharply from around US $20 to US $41 per barrel, resulting in a significant decline in the global GDP growth rate.

Changes in copper prices before and after the oil crisis

Based on the monthly average price data of copper and crude oil released by the World Bank, comparing their trends before and after the oil crisis, it is found that copper prices have also risen significantly during the oil price rise phase of the three oil crises. Among them, during the oil price rise phase of the first oil crisis, crude oil prices rose by 3.8 times and copper prices by 56%; during the second oil crisis, crude oil prices rose by 1.8 times and copper prices by 90%. During the oil price rise phase of the third oil crisis, crude oil prices rose by 1.25 times and copper prices by 17%. From the point of view of the increase, there is no relatively definite proportional relationship between oil prices and copper prices.

At the same time, during the oil price decline phase of the three oil crises, copper prices also recorded a large decline, and in the process of decline, copper prices fell more steeply than crude oil.

Further observation can also find that before the three oil crises, copper prices are in an upward trend, and in the oil crisis, copper prices are relatively stagnant in the early stage of oil price rise, and copper prices tend to be stronger in the later stage of oil price rise.

Next, the following will continue to explore the impact of the oil crisis on several other important variables in the copper market (macroeconomic, supply and demand, and market risk sentiment).

Macroeconomic changes before and after the oil crisis

The macro economy is measured by manufacturing PMI, year-on-year industrial production index, unemployment rate and 10-year Treasury yield.

Before the first oil crisis, the US manufacturing PMI remained above 60, the industrial production index grew by more than 7 per cent, the unemployment rate gradually declined, the yield on 10-year Treasury bonds rose moderately, and the overall economy grew rapidly. After the beginning of the oil crisis, the US unemployment rate soon bottomed out and rebounded. The manufacturing PMI and industrial production index fell below the boom-bust line and the growth rate turned negative three quarters after the oil supply shock, while the 10-year Treasury yield rose at a moderate pace, reflecting the slow pace of monetary policy tightening during the crisis and the gradual weakening of the macro-economy.

Before the second oil crisis, the US manufacturing PMI also remained above 60, the industrial production index grew at a moderate rate, the unemployment rate and 10-year Treasury yields were stable, and the overall economy grew moderately and expected to be better. After the start of the oil crisis, the US industrial production index first entered negative growth, the manufacturing PMI gradually weakened, while the unemployment rate and the yield on the 10-year Treasury note remained stable for some time. After the third quarter of the supply shock, the yield on the 10-year Treasury note accelerated, then the unemployment rate gradually rose, and the main economic indicators Synchronize weakened. Compared with the first oil crisis, the US economy is weakening at a slower pace.

Before the third oil crisis, the US manufacturing PMI rose moderately, the industrial production index grew slightly negative, the unemployment rate and 10-year Treasury yields were stable, and the overall economy gradually recovered. After the start of the oil crisis, the decline in the US industrial production index expanded, the manufacturing PMI fell below the rise and fall line within a few months, the unemployment rate continued to rise, while the yield on the 10-year Treasury note rebounded slightly and then fell, reflecting the stronger short-term macroeconomic impact of the oil crisis.

Summary: before and after the oil crisis, the macro-economy is basically a process from strong to weak, and the impact of the oil crisis on the economy depends on the strength of the economy itself before the crisis. The stronger the economy before the crisis, the longer the negative feedback time of oil supply shock.

Changes in supply and demand of copper before and after the oil crisis

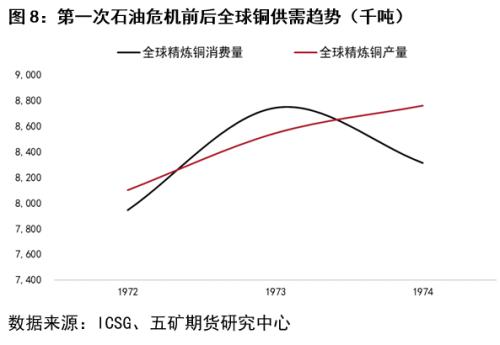

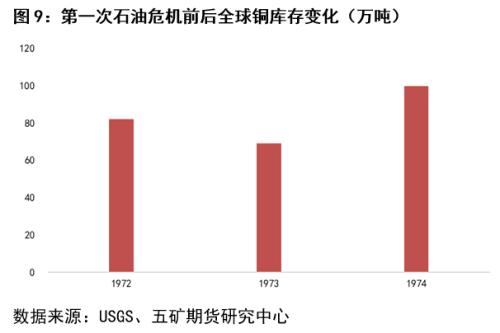

Before the first oil crisis, thanks to the faster growth of copper demand, the global copper market changed from a supply glut in 1972 to a supply shortfall in 1973, and copper inventories were eliminated more quickly. However, with the impact of oil supply and rising copper prices, copper demand weakened rapidly after peaking in 1974. In 1974, market supply and demand turned to oversupply, and global copper inventories increased.

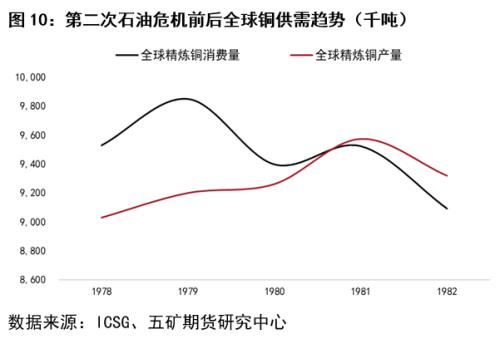

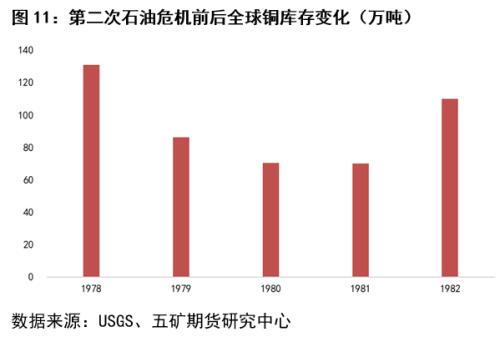

Before the second oil crisis, the slow growth of copper supply and faster growth of demand prompted the global copper market to be in a state of supply less than demand for three consecutive years, and copper stocks were continuously eliminated. After the oil supply shock, despite the decline in demand, the frequent growth of supply due to disturbance factors is not obvious, and global copper stocks continued to disappear in 1979. Copper demand declined rapidly in the first half of 1980 as the economy weakened, but the rapid decline in copper prices in the second half of the year and the strike at copper mines in the United States led to a strengthening of supply and demand again. There was no surplus of supply and demand in the market for the whole year, and copper stocks remained de-stocked. Over the next two years, global copper supply and demand turned to oversupply.

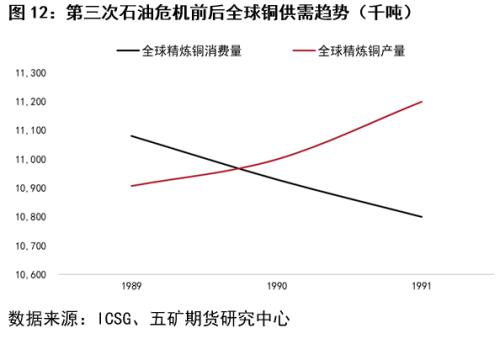

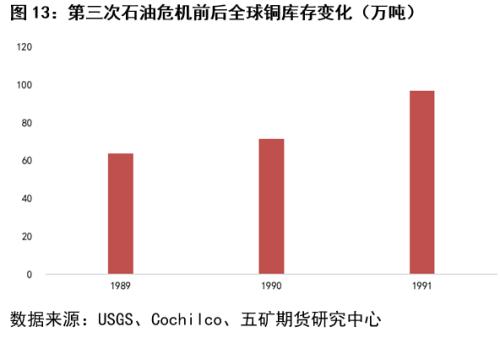

Before the third oil crisis, the supply and demand of the global copper market was relatively balanced, and copper stocks were eliminated slightly in 1989. After the oil crisis, the global copper demand declined in 1990, while the supply maintained a small growth trend, copper supply and demand changed to oversupply, and the global copper market maintained a supply glut in 1991.

Summary: before the oil crisis, the global copper supply and demand was basically in a state of supply less than demand. After the crisis, the global copper supply and demand have weakened, and mainly reflected in the demand side following the downward trend of the macro-economy.

Changes in market risk sentiment before and after the oil crisis

Measure market risk sentiment by the Dow Jones index and the dollar index. Before the first oil crisis, the Dow Jones Industrial average was stable, the dollar index weakened, and the market risk sentiment was more positive. after the oil supply shock, the Dow Jones Industrial average fell, the dollar index significantly strengthened, and the market risk sentiment weakened significantly.

Before the second oil crisis, the Dow Jones Industrial average rose slightly, the dollar index weakened, and the market risk sentiment was also positive. after the oil supply shock, the Dow Jones Industrial average did not go down unilaterally, and the dollar index fell first and then rose. Market risk market sentiment is less affected.

Before the third oil crisis, the Dow Jones Industrial average rose slightly, the dollar index weakened, and the market risk sentiment was more positive. after the oil supply shock, both the Dow Jones Industrial average and the dollar index first suppressed and then rose. Market risk field sentiment has been hit to a certain extent.

Summary: the three oil crises all led to the weakening of market risk sentiment, of which the first crisis risk sentiment was the most affected, and the impact time of the second and third crisis on risk sentiment became shorter and weaker.

Conclusion: through the above analysis, it is concluded that the oil crisis has the following effects on the copper market: 1. Copper prices will rise and fall to a certain extent along with the rise and fall of oil prices during the oil crisis, and the performance of copper prices is relatively stagnant in the early stage of oil price rise, and the performance of copper price is often stronger in the later stage of oil price rise. 2. During the oil crisis, both the macro-economy and the supply and demand of the copper market experienced a process of changing from strong to weak, and the change of supply and demand was mainly reflected in following the change of macro-economic demand. 3. During the oil crisis, the market risk sentiment was impacted to varying degrees, and the impact weakened one by one.

Author: Wu Kunjin, Minmetals Futures

![ยอดรวมสต๊อกทองแดงในสังคมช่วงสุดสัปดาห์เพิ่มขึ้น แนวโน้มตามภูมิภาคแตกต่างกัน [ข้อมูลรายสัปดาห์ของ SMM]](https://imgqn.smm.cn/usercenter/TlzAr20251217171709.jpg)