SHANGHAI, Jan 28 (SMM) - This is a roundup of China's metals weekly inventory as of January 28.

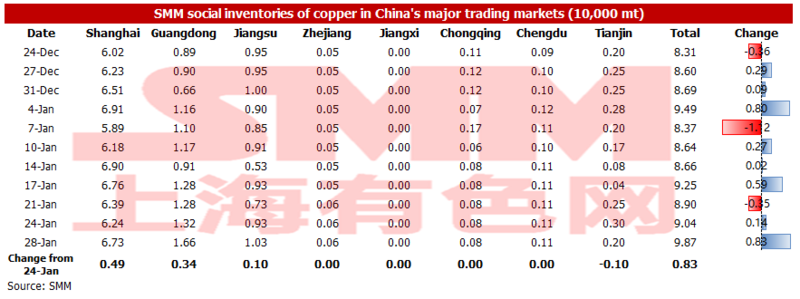

Copper Inventory in Major Chinese markets Added 8,300 mt This Week

As of Friday, January 28, the copper inventories in major domestic markets increased 8,300 mt from Monday to 98,700 mt, and added 9,700 mt from a week earlier, growing for the third straight week.

The domestic inventories began to accumulate but the growth was less than the same period last year. The stock accumulation in the last week before the CNY holidays of 2021 stood at 16,000 mt. Compared with Monday, only the inventory in Tianjin dipped slightly, while the inventory grew across Shanghai, Guangdong and Jiangsu. The inventory in other areas changed little.

The stocks in Shanghai increased by 4,900 mt to 67,300 mt; stocks in Guangdong increased by 3,400 mt to 16,600 mt; stocks in Jiangsu increased by 1,000 mt to 10,300 mt; stocks in Tianjin decreased by 1,000 mt to 2,000 mt mt.

As Tianjin is still affected by the COVID and consumption is still poor, smelters in the north turned to ship cargoes to the south, causing the local inventories to decline this week. The increased arriving shipments and weaker consumption in east China and Guangdong drove the inventories to grow.

There will be fewer workers stay put during CNY holidays this year compared with last year, and the consumption will unlikely return to normal levels in the first week following CNY holidays. Therefore, the stock accumulation in the first week following CNY holidays may exceed that in the same period last year.

Copper Inventory in Domestic Bonded Zone Grew 18,600 mt on Week

The copper inventories in domestic bonded zones increased 18,600 mt from January 21 to 243,100 mt as of January 28, growing for five consecutive weeks, according to SMM survey.

The inventory in the Shanghai bonded zone increased 16,600 mt to 213,600 mt, and the inventory in the Guangdong bonded zone added 2,000 mt to 29,500 mt.

With the approaching of CNY holidays, the copper import market is extremely quiet. The high import losses depressed the customs declaration and imports. Meanwhile, the transportation efficiency of warehouses decreased, hence slowing down the shipments from bonded warehouses.

In terms of arriving shipments, the inflows of shipments arrivals under B/L and the exports by the domestic smelters accelerated the growth in the bonded zone inventories.

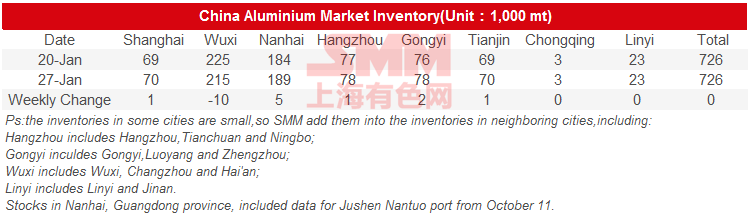

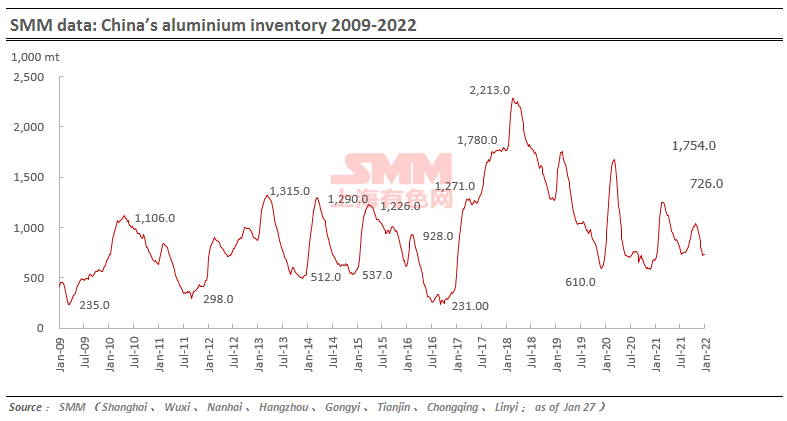

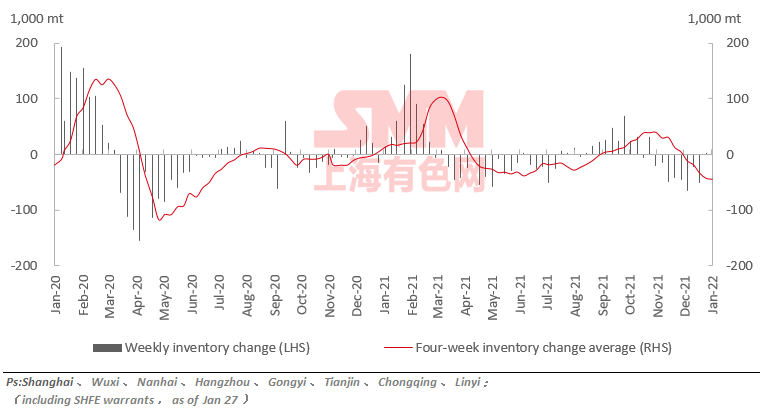

Aluminium Social Inventories Flat on Week

SMM data showed that China's social inventories of aluminium across eight consumption areas were flat on the week at 726,000 mt as of January 27, with Nanhai, Gongyi, Shanghai and Hangzhou contributing most of the increase. The inventory in Wuxi dropped amid less arrivals and moderate shipments.

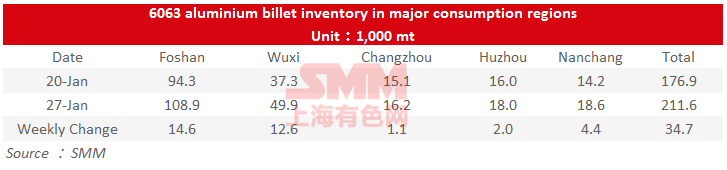

Aluminium Billet Inventories Up 34,700 mt on Week

The stocks of aluminium billet in five major consumption areas added 34,700 mt to 211,600 mt as of January 27 from a week ago, a significant increase of 19.62%. The inventory has been rising for five straight weeks.

The inventories across the five major market all recorded gains. Among them, the inventory in Foshan and Wuxi contributed most of the increase, which rose by 14,600 mt and 12,600 mt respectively, an increase of 15.48% and 33.78% week-on-week. The downstream almost stagnated in the past week on the imminent Chinese New Year, resulting in sluggish transactions.

Looking into next week, the domestic aluminium billet inventory is expected to rise further during the CNY holiday.

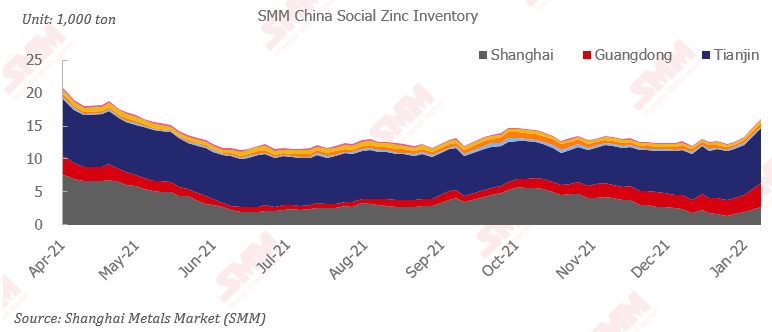

Zinc Ingot Social Inventory in Seven Major Regions in China Rose 26,900 mt

As of January 28, the zinc ingot inventory across the seven major regions in China totalled 160,500 mt, up 15,200 mt from January 24 and up 26,900 mt from January 21, according to SMM data. The accumulation of domestic inventories accelerated this week. The inventory in Shanghai increased significantly as higher zinc prices suppressed downstream demand and more cargoes arrived. The inventory in Guangdong also grew amid stable arrivals and sharp decline in demand after the downstream producers took the CNY holiday. The inventory in Tianjin continued to increase as most of the downstream producers have shut down for the CNY. The total inventories across Shanghai, Guangdong, and Tianjin rose by 25,100 mt from January 21.

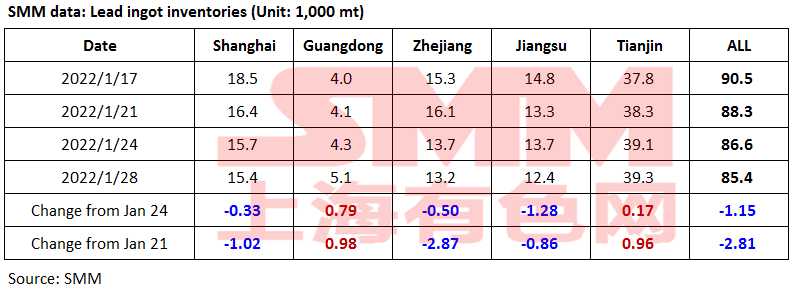

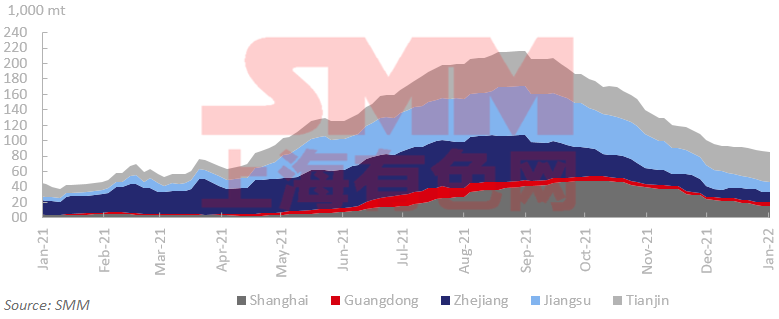

Lead Ingot Social Inventory Fell 2,800 mt on Week

The social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin decreased 2,800 mt from January 21 and 1,100 mt from January 24 to 85,400 mt as of January 28.

The logistics services have basically stopped on account of imminent Chinese New Year holiday and strict COVID-19 pandemic control, hence long-distance lead ingot transport was unavailable in the past week, according to SMM research. Some downstream participants that were still in production, mainly in Zhejiang and Jiangsu, have completed taking the last batch of orders. The local inventory in places like Guangdong and Tianjin have been rising for two straight weeks amid shrinking demand.

Looking into next week, there are both primary and secondary lead smelters producing in shifts, while the downstream lead-acid battery manufacturers have basically closed for CNY holiday. The market shall keep an eye on the possibilities of inventory accumulation post the holiday.

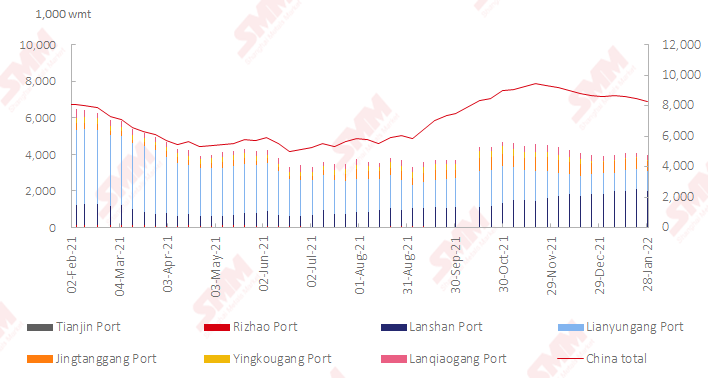

Nickel Ore Inventories at Chinese Ports Fell 175,000 wmt

The nickel ore inventory at Chinese ports dipped 175,000 wmt from a week earlier to 8.28 million wmt as of January 28. Total Ni content stood at 65,000 mt. The total inventory at seven major ports stood at around 3.96 million wmt, 135,000 wmt lower than a week earlier.

The arriving shipments and shipping slowed down as the CNY holidays are approaching. The wet season in the Philippines also limited the shipments arrivals.

The port inventory will maintain a downward trend in the short term in the absence of supplement by other resources.

Import Premiums to Remain High on Low Shipments Arrivals in China Boned Zone

Imports remained loss-making this week. Imports of pure nickel are still insufficient to meet the domestic demand, while the spot supply of domestic nickel plates and nickel briquette remains tight. The import premiums thus continued to rise.

The import premiums can hardly fall as the arriving shipments in the bonded zones are expected to be limited post-CNY holidays.

The SHFE/LME nickel price ratio is likely to improve given the current demand and limited customs clearance.

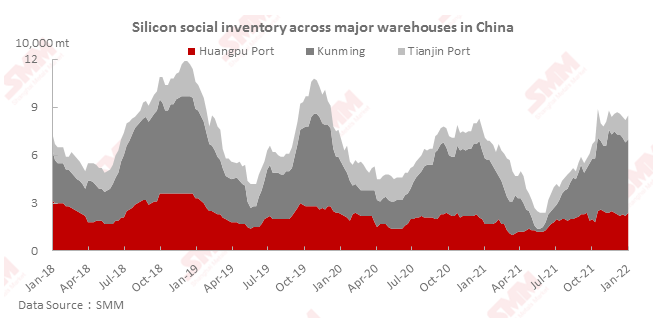

Silicon Metal Social Inventory Added 3,000 mt on Week

The social inventory of silicon metal across Huangpu port, Kunming city and Tianjin port rose 3,000 mt from the previous week to 85,000 mt as of Friday January 28.

The inventory in Kunming was largely unchanged, and some of the stocks were scheduled to be shipped to other places through railway next week. The inventories in Huangpu port and Tianjin port rose slightly, as the silicon metal manufacturers and traders shipped to goods to the ports in advance for post-CNY holiday transactions amid concerns over slow recovery of logistics services post the holiday amid potential risks of resurging COVID-19 pandemic and influences from Beijing Winter Olympics.

![[SMM Analysis] Futures Lack Momentum to Rise Further, Pre-Holiday Demand Stalls, and Stainless Steel Social Inventory Accumulation Intensifies](https://imgqn.smm.cn/usercenter/HBsPu20251217171723.jpeg)