SHANGHAI, Jul 23 (SMM) – This is a roundup of China's metals weekly inventory as of July 23.

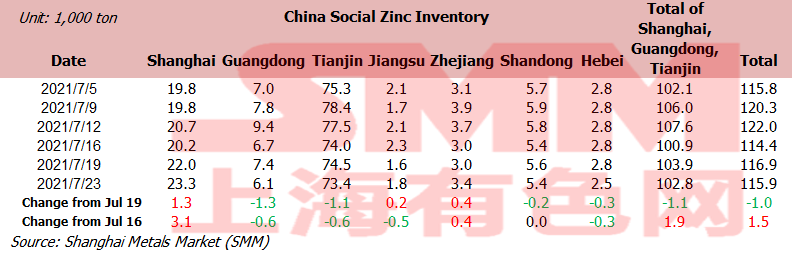

Zinc social inventories expanded 1,000 mt on week

SMM data showed that social inventories of refined zinc ingots across Shanghai, Tianjin, Guangdong, Jiangsu, Zhejiang, Shandong and Hebei increased 1,500 mt in the week ended July 23 to 115,900 mt. The stocks fell 1,000 mt from Monday June 19.

Stocks in Shanghai rebounded on week as arrivals of imported zinc increased and downstream purchase for rigid demand. In south China's Guangdong, market arrivals declined affected by power curtailments and limited production of smelters, and the downstream still had rigid demand, with stocks reaching a new low. Stocks in Tianjin fell as rebounded steel prices led to the improvement of downstream orders.

Stocks across the three major trading hubs (Shanghai, Tianjin and Guangdong) rose 1,900 mt this week, after a 5,100 mt increase last week.

Shanghai bonded copper stocks fell 6,900 mt on week

Stocks of copper in Shanghai bonded areas decreased on smaller arrivals for two consecutive weeks.

SMM data showed that the stocks fell 6,900 mt from the prior week to 428,600 mt as of Friday July 23.

Domestic copper supply is tight amid moderate consumption, social inventories are still in a state of continuous decline, and spot premium remains high. The profit from spot imports has continuously stimulated the demand for imported copper since last week, and the increase in market declaration imports has driven the stocks in bonded areas to continue to decline.

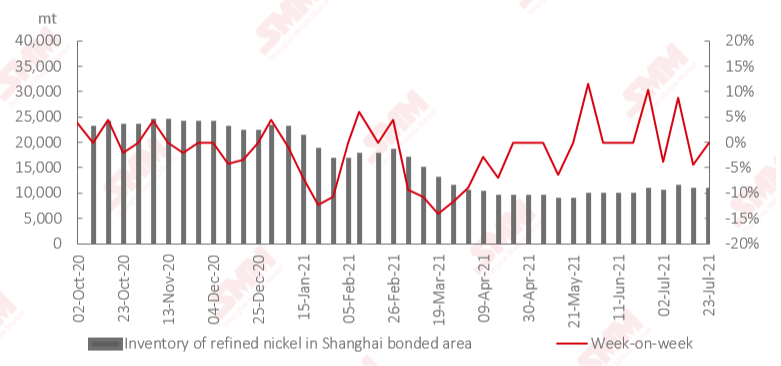

Shanghai bonded refined nickel stocks remained unchanged on week

Inventories of refined nickel in the Shanghai bonded areas emained unchanged from a week ago and stood at 10,700 mt as of July 23, showed SMM data.

The ratio of SHFE nickel to LME nickel fluctuated and fell this week, and the import profit of nickel plates narrowed. At present, warehouse receipt transactions in bonded areas are sluggish, and bill of lading transactions dominate the market. The quotation of Russian nickel warehouse receipts still stood at around $200/mt, Sumitomo nickel warehouse receipts came in at around $210/mt, and the original nickel briquettes in the bonded area were quoted at $300/mt.

Nickel ore inventories at Chinese ports rose 325,000 wmt to 5.66 million wmt

Nickel ore inventories across all Chinese ports increased 325,000 wmt from July 16 to 5.66 million wmt as of July 23, showed SMM data.

In Ni content, the stocks stood at 44,600 mt.

SMM data also showed that nickel ore stocks across seven major Chinese ports increased 85,000 wmt during the same period to 3.5 million wmt.

Nickel ore inventories increased sharply this week. Customs imports fell short of expectations in June due to some cargoes held in port and the short-term shutdown of the northern ports in response to the environmental protection needs. The problem of holding in port eased in July, and the arrivals increased. Nickel ore inventories at Chinese ports may still maintain an upward trend in the near term amid peak season of delivery.

Silicon social inventories rose 4,000 mt on week

Social inventories of silicon metal across Huangpu port, Kunming city and Tianjin port rose 4,000 mt from the previous week to 40,000 mt as of Friday July 23.

The inventories increased in all three social warehouses. However, the market trade is improving, and the growth of social inventories is expected to slow down recently.

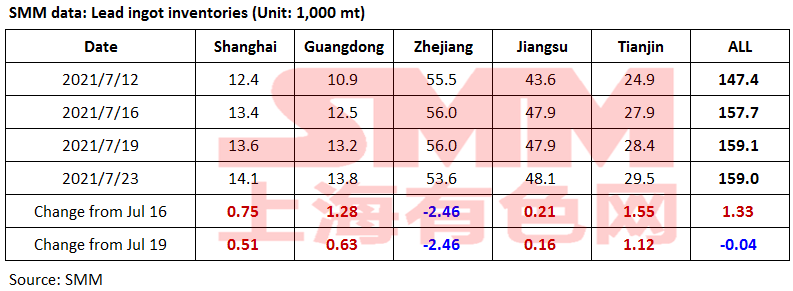

Lead ingot social inventories up 1,300 mt on week

Social inventories of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin expanded 1,300 mt from last Friday July 16 to 159,000 mt as of July 23. This was down 40 mt from Monday July 19.

The output of the deliverable primary lead declined slightly on the week due to the power curtailment and maintenance in some smelters. The heavy rains in Henan impeded the local transportation, which slowed down the transfer of lead ingot stocks from plants to social warehouses.

Lead futures rose over 16,000 yuan/mt, discouraging downstream purchase. If the prices stand high next week, the consumption will stay weak, and the social inventories of lead ingots will increase.

Attention needs to be paid to the impact of the heavy rains in Henan and the typhoon in Jiangsu and Zhejiang on the transportation and stocks of lead ingots.

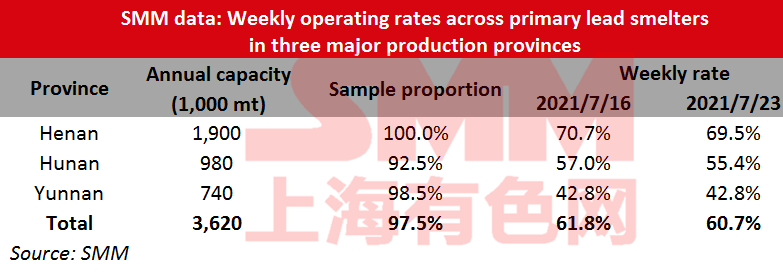

Operating rates of primary lead smelters down 1.09 percentage points on week

Operating rates across primary lead smelters in Henan, Hunan and Yunnan provinces lost 1.09 percentage points from the previous week to 60.7% in the week ended July 23, showed an SMM survey.

In Henan, Minshan maintained the slight production. Jinli and Xinling reduced production slightly last weekend due to the production, but resumed normal production early this week.

Hunan Yuteng started maintenance this Thursday, and the production is expected to resume in early August.

Anhui Tongguan cut production this week due to equipment failure, and is expected to resume operation in early August.

Production in Yunnan remained normal.

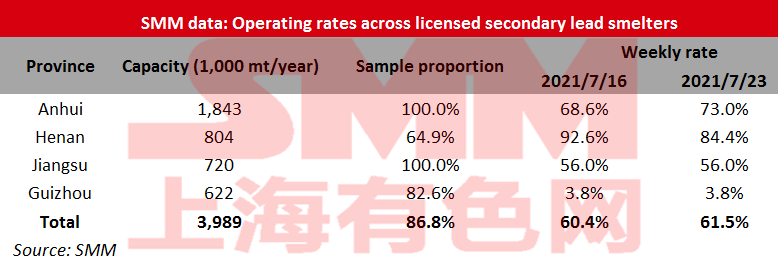

Operating rates of secondary lead smelters up 1.06 percentage points on week

Operating rates across licensed smelters of secondary lead in Jiangsu, Anhui, Henan and Guizhou averaged 61.47% in the week ended July 23, up 1.06 percentage points from the previous week, showed an SMM survey.

In Anhui, Tianchang further resumed production this week after the maintenance, and Dadao suspended production for maintenance due to equipment failures. Henan Jinli halted production for one day amid power curtailment. The overall operating rate was recovering.

Besides the sample companies, Tongliao Taiding in Inner Mongolia resumed production early this week, Xincheng Power in Henan started maintenance in the mid-week due to equipment problems, Anhui Dadao finished maintenance, and Henan Jinli resumed normal production. Operating rates are expected to further rise next week.

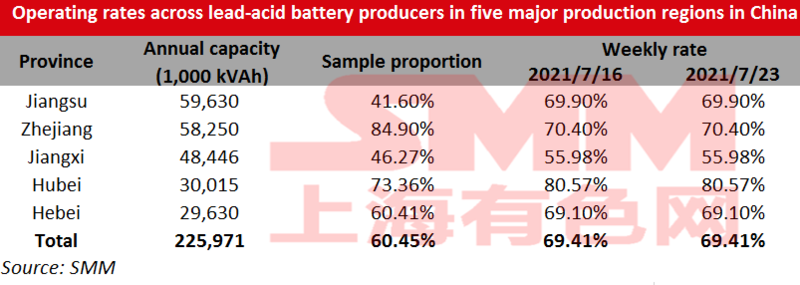

Operating rates of lead-acid battery plants flat on week

Operating rates across lead-acid battery producers in Jiangsu, Zhejiang, Jiangxi, Hubei and Hebei provinces stood largely flat at 69.41% on the week as of Friday July 23.

The off-peak season market improved slightly this week. The orders for the electric bicycle battery increased steadily, and the inventory pressure of battery declined. The production enthusiasm was relatively high.

However, the consumption in the car battery market was less changed, and the prices of batteriesare difficult to increase. Most companies maintained the operating rates at 70-90%.In addition, the battery production in Henan needs attention as the heavy rains continue there.

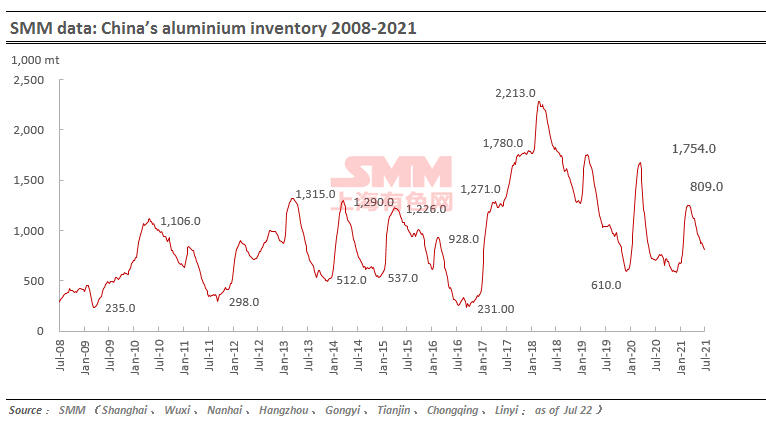

Primary aluminium inventories shrank 23,000 mt on week

Social inventories of primary aluminium ingots across eight consumption areas in China, including SHFE warrants, decreased 23,000 mt from last Thursday to 809,000 mt as of July 22. Stocks in Shanghai, Wuxi and Nanhai continued to contribute to the decrease. Stocks in Gongyi didn't increase sharply as the transportation of local warehouses were restricted. Stocks of aluminium ingots fluctuated little on week.

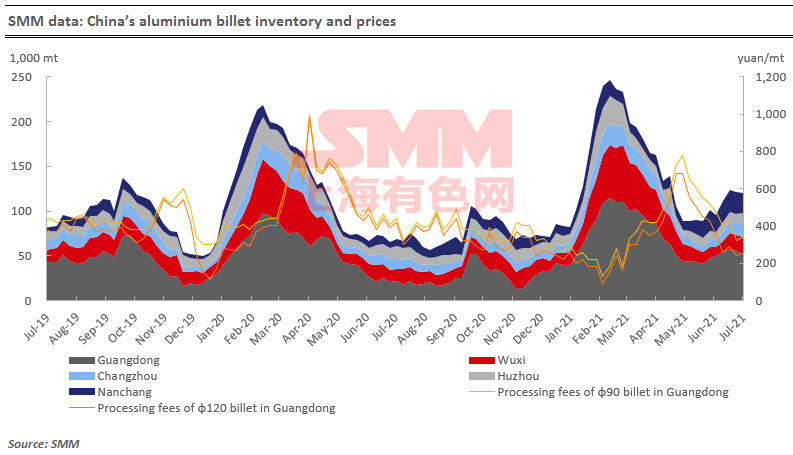

Aluminium billet inventories fell 1,200 mt on week

The outbound quantity of aluminium billet decreased 1,800 mt or 3.7% to 46,500 mt last week. The downstream was less willingness to restock under the continuous fluctuation of aluminium prices at high.

SMM data showed that aluminium billet stocks across the five major consumption areas — Foshan, Wuxi, Huzhou, Changzhou and Nanchang — in China decreased 0.9% or 1,200 mt from a week ago to 119,600 mt as of Thursday July 22. Stocks in Wuxi and Huzhou rose. Among them, Huzhou area increased the most, with inventories increasing by 3,000 mt or 33%. Stocks in Foshan, Changzhou and Nanchang fell, with Foshan and Nanchang decreasing more.

The overall market trading atmosphere was moderate this week. Due to the heavy rain disaster in Henan, some aluminium plants stopped production, which caused aluminium prices to fluctuate greatly amid improved downstream wait-and-see sentiment, poor receiving mood and tepid market turnover. SMM survey showed that the liquidity of the spot market of aluminium billets is loose at present, and the downstream aluminium profile enterprises purchase mainly for rigid demand, and the daily turnover of the overall market is average. However, due to the blockage of Longhai Line caused by the rainstorm disaster in Henan, there will be less arrivals in Wuxi warehouses, and it is expected that inventories will not pile up next week.

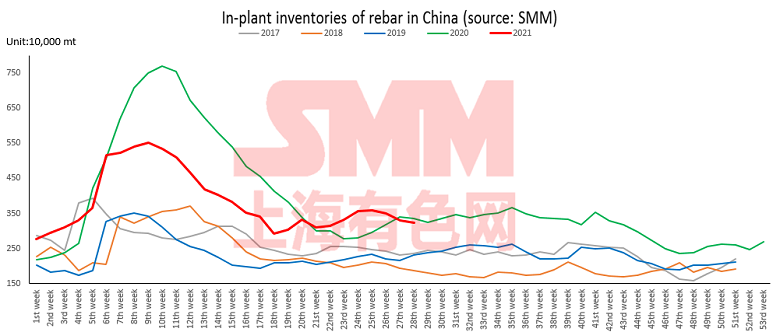

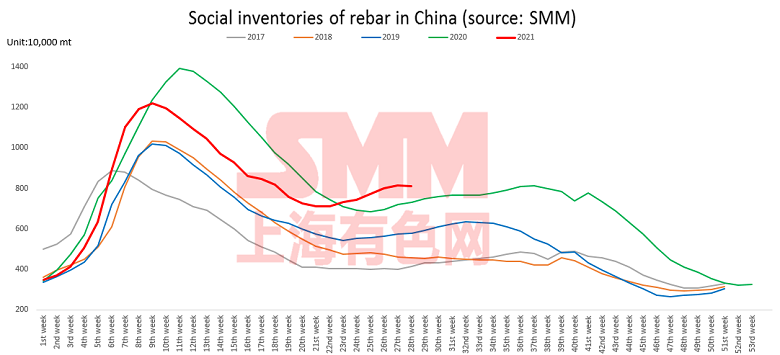

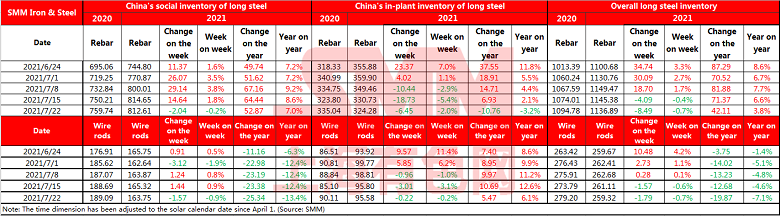

China steel rebar inventory down 0.7% on week

Inventories of rebar across Chinese steelmakers and social warehouses stood at 11.37 million mt as of July 22, down 0.7% from a week ago. Stocks are up 3.8% from a year earlier.

Inventories at Chinese steelmakers fell 64,500 mt on the week and stood at 3.24 million mt. Stocks are down 2% from a week ago and up 3.2% from a year earlier.

Inventories at social warehouses fell 20,400 mt on the week and stood at 8.13 million mt, down 0.2% from a week ago and 7% higher from a year ago.

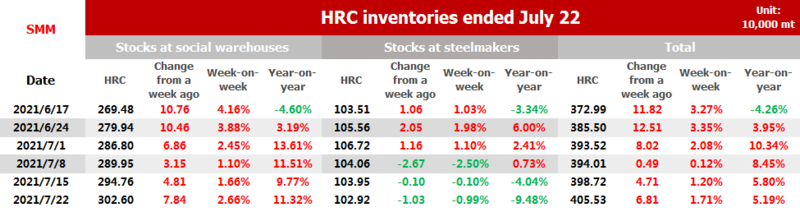

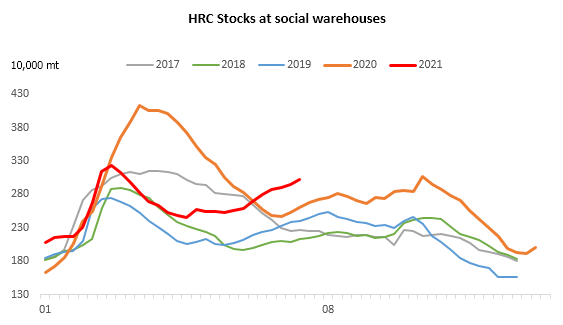

China HRC inventory up 68,100 mt on week

SMM data showed that HRC stocks across social warehouses and steel makers rose 68,100 mt or 1.71% on the week, an increase of 5.19% than a year ago, to 4.06 million mt in the week ended July 22.

Inventories across social warehouses increased 78,400 mt or 2.66% week on week to 3.03 million mt. This was 11.32% higher than the same period last year.

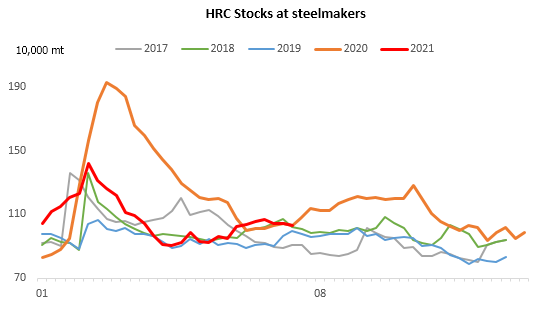

Stocks at Chinese steel makers came in at 1.03 million mt, down 10,300 mt or 0.99% week on week and a decrease of 9.48% year on year.

Operating rates of blast furnaces across Chinese steelmakers fell 0.2 percentage point on week

Operating rates of blast furnaces at steel mills fell 0.2 percentage point from a week ago and decreased 3.7 percentage points from a month ago to 81.2% as of July 22, SMM survey showed.

![The Most-Traded BC Copper Contract Closed Up 0.09%, with Macro Uncertainty Keeping Copper Prices on a Fluctuating Trend [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/Bwtty20251217171714.jpeg)