SHANGHAI, May 21 (SMM) — Rebar prices fell broadly this week. The main reason was the intensive voices of relevant departments to suppress the rapid rise of bulk commodities. The shift in policy focus made the market less confident in this year's crude steel reduction policy, and the expected output shrinkage collapsed. The panic in the market intensified and the spot selling pressure released. The national average rebar prices stood at 5,234 yuan/mt as of May 20, down 811 yuan/mt week on week.

The market will gradually return to the fundamentals of the industry after experiencing the stimulus of the news and soaring and plummeting.

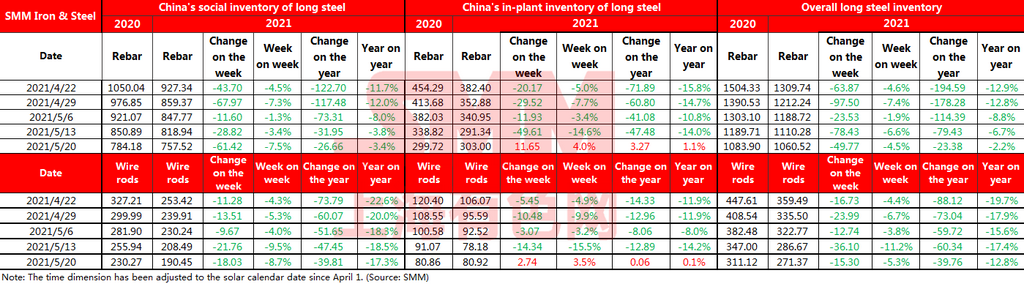

Inventories of rebar across Chinese steelmakers and social warehouses stood at 10.61 million mt as of May 20, down 4.5% from a week ago. Stocks are down 2.2% from a year earlier.

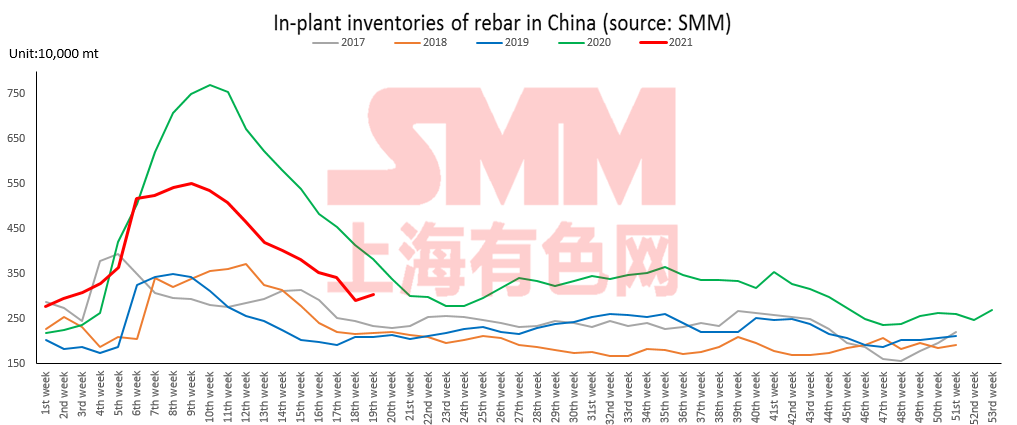

Due to the wide drop in steel prices, market panic intensified. Merchants were actively lowering inventories to settle the situation. The market was more bearish, and traders were less willing to receive goods. In-plant stocks piled up slightly on week. Inventories at Chinese steelmakers rose 116,500 mt on the week and stood at 3.03 million mt. Stocks are up 4% from a week ago and up 1.1% from a year earlier.

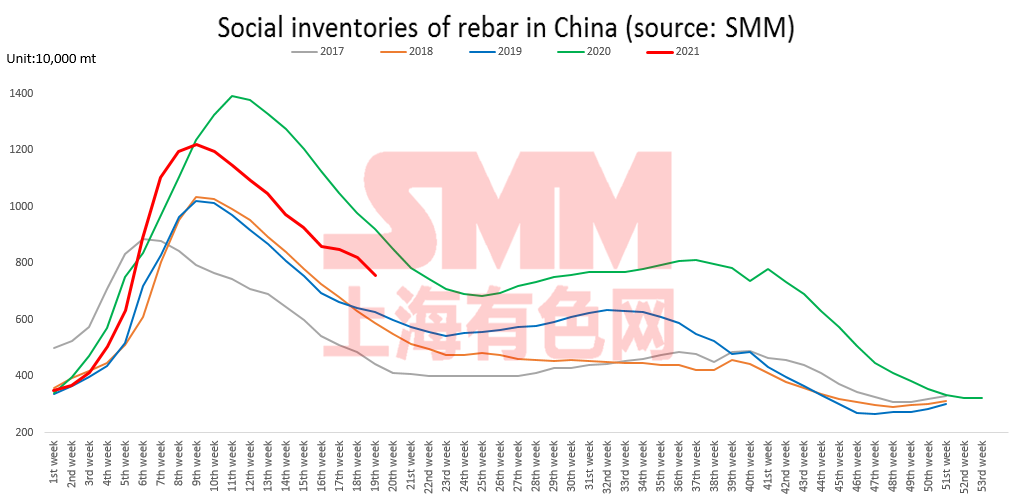

Speculative demand for sharp price increases in the early period accumulated a part of speculative inventories. In the process of this round of price plummets, spot selling pressure is greater, and speculative inventory is the main force behind low prices. In addition, although end-users have no signs of substantial restocking, the purchase enthusiasm has picked up at high prices, so social stocks posted slightly faster increase. Inventories at social warehouses fell 614,200 mt on the week and stood at 7.58 million mt, down 7.5% from a week ago and 3.4% lower from a year ago. The week-on-week decrease expanded 4.1 percentage points from the previous week. The year-on-year decrease fell 0.4 percentage point from the previous week.

On the supply side, the current policy is more inclined to balance between controlling output and alleviating downstream cost pressures, so the expected production restriction news and policy implementation may be delayed. When steel prices are adjusted significantly, the possibility of returning to control output is also relatively high. In addition, after prices plunged, the profit margin of steel mills greatly shrank and was close to the production cost line. It is expected that the production rhythm may slow down, such as the increase in monthly maintenance after the previous delay, so the pressure on the supply side can be eased.

On the demand side, it is currently the off-season of seasonal consumption, while the resilience of domestic demand has not changed significantly. After the first batch of land auctions in the "two-concentration" cities in May, as land transactions rebounded, new construction projects are likely to exceed expectations in the second half of the year.

The suppression of steel supply by the "carbon peak" will continue. The resilience of demand for real estate and infrastructure, and the resonant recovery of global demand after the pandemic is under control. These three upper-level logics supporting the rise of commodities remain unchanged. Therefore, this round of correction is not a turning point in the overall trend.