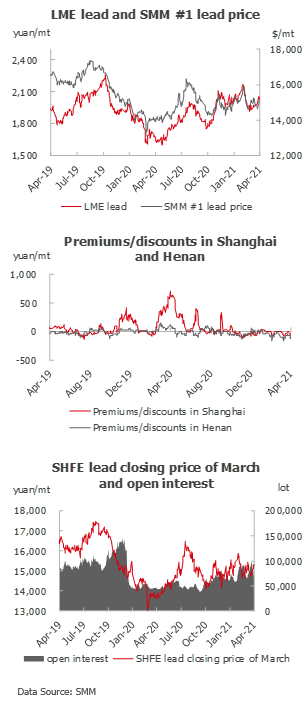

SHANGHAI, Apr 27 (SMM)—As downstream battery factories started deliver goods, the social inventory of lead ingots decreased from the high level on the month. However, the market quotations of primary lead was still offered at a wide discount, and the price difference between refined and scrapped lead expanded to above 250 yuan/mt, leading to the weak fundamental performance of the industrial line from lead ingot to downstream consumption. Focus this week will be whether the lead ingot inventory will continue to drop, and whether the spot discounts will narrow and drive up the lead prices.

In addition, the tight domestic lead concentrate supply was intensified, and the quotations of TCs for imported lead concentrate fell to $40-50/dmt, while the quotations of TCs for domestic concentrate was more complicated. In Henan, the TCs for the concentrate with high content of lead and silver were between 1,400-1,700 yuan/mt in metal content, and that for ordinary lead concentrate were between 1,700-1,800 yuan/mt (Pb content). The market will pay attention to whether consumption can resonate with the shortage of concentrate. It is not recommended to go short in the market. The price of most traded lead futures contract will stand between 15,150-15,500 yuan/mt.

LME lead inventory decreased by 2,875 mt last week, but the spot discount gradually expanded to $24.25/mt, indicating that overseas consumption was recovering steadily with sufficient spot supply. As the domestic supply of lead concentrate was tight, the market may rely more on imported concentrate, and the SHFE/LME price ratio may gradually move up. LME lead is expected to move between $2,105-2,070/mt.

Spot prices are expected to move between 15,100-15,400 yuan/mt this week. The primary lead supply will decline due to the maintenance in Henan, and downstream plants are purchasing for rigid demand with lower willingness to restock amid the high prices. The overall spot trade is expected to weaken from the previous week, and smelters may deliver cargoes at high prices. The secondary lead production in Anhui and Jiangxi was still under the impact of environmental protection inspections, but a few plants finished the maintenance. If lead prices further go up, the smelters may be more active to ship cargoes, and the price difference between refined and scrapped lead is expected to further expand.