SMM7 March 31: the novel coronavirus epidemic has dragged down the pace of the global economy. China is one of the few countries expected to achieve positive GDP growth in 2020. According to the latest world economic outlook released by the International Monetary Fund in June, global GDP growth is expected to be-4.9 per cent in 2020, compared with-3 per cent previously expected; US GDP growth is expected to be-8.0 per cent in 2020, compared with-5.9 per cent; and eurozone GDP growth is expected to be-10.2 per cent in 2020, compared with-7.5 per cent previously expected.

IMF said the downgrade in global economic forecasts for 2020 was due to novel coronavirus's greater impact on consumption than initially expected. Gopinath, chief economist of IMF, said the virus would cause 1200 trillion dollars in cumulative damage to the global economy.

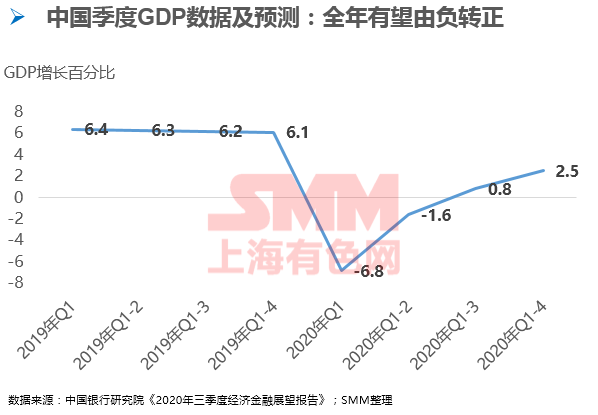

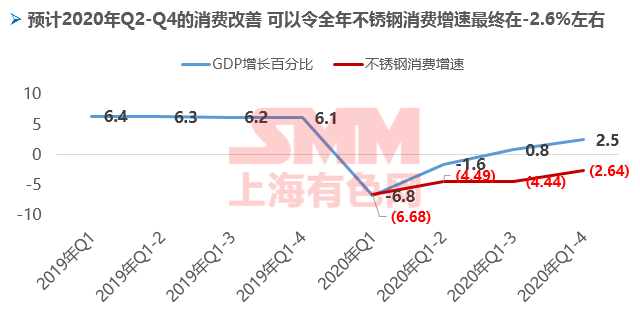

On June 30, 2020, the Bank of China Research Institute released the Economic and Financial Outlook report for the third quarter of 2020 (hereinafter referred to as "the report") in Beijing. Looking forward to the second half of the year, China's economy will continue to recover and improve. However, there are also hidden dangers such as the rebound of the epidemic situation, the increasing difficulties in production and operation of enterprises, and the increased risk of local debt. GDP is expected to grow by about 5.2 per cent in the third quarter and about 2.5 per cent for the whole year. In the future, China should speed up the construction of a new pattern of "double cycles" at home and abroad to promote each other's development, give greater play to the role of internal circulation, speed up the realization of "two-wheel drive" of both internal and external cycles, and jointly promote the stability and development of China's economy.

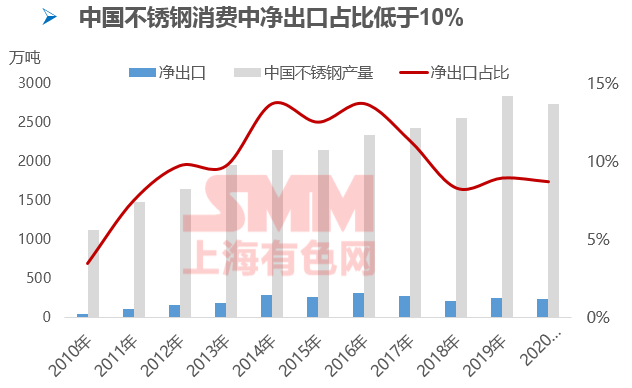

Due to the numerous anti-dumping policies, China's stainless steel consumption is not highly dependent on exports and focuses on domestic consumption.

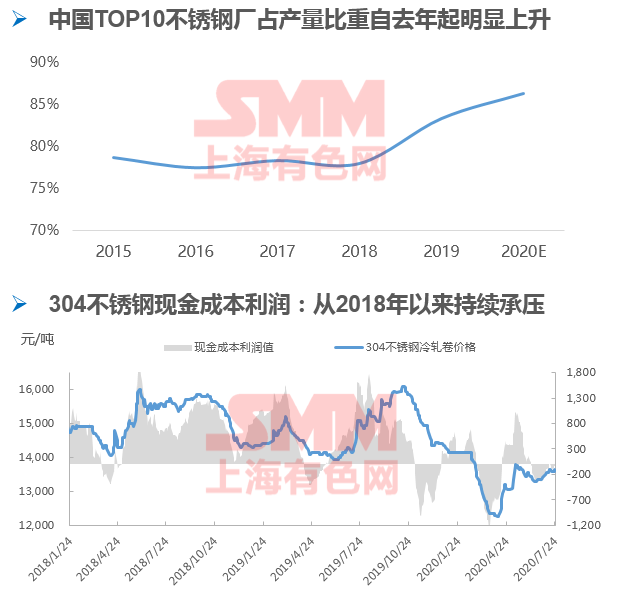

The development characteristics of China's stainless steel industry in recent years: the output continues to expand, the industry competition is fierce, the enterprise concentration increases and the profit pressure is great.

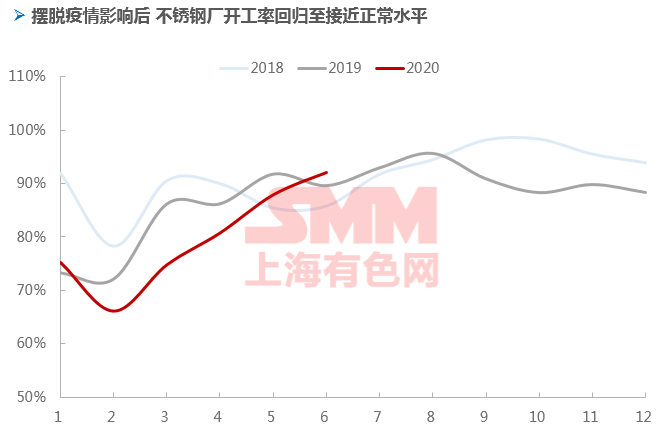

The supply side of stainless steel in China in 2020: stainless steel plants returned to the normal operating rate early to get rid of the impact of the epidemic.

The above picture shows the operating rate of domestic stainless steel plants, we can see that during the epidemic, the operating rate of the stainless steel industry decreased significantly compared with previous years, while the operating rate of the stainless steel industry has gradually returned to the normal level from April to May.

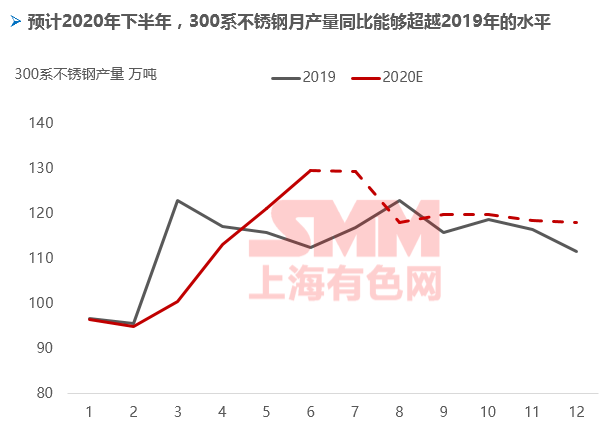

The following picture shows the output of 300 series stainless steel plants in China, which directly affects the domestic consumption of primary nickel. It can be seen that from April to May, the output of 300 series has hit a new high again, and then stabilized at a high level. It is also expected that the year-on-year output in the second half of the year will be higher than that in the same period last year. This will provide some support to the demand for primary nickel. However, in the specific nickel raw material procurement decision, due to the obvious economy of nickel pig iron, the demand for nickel pig iron will be higher than in previous years, while the purchase of pure nickel has shrunk to the minimum compared with last year.

As mentioned earlier, due to the impact of the epidemic, the consumption of stainless steel is slightly weak this year, which is a major negative factor, but in the range where nickel prices are already low, the supply of raw material nickel pig iron is also sufficient, and mainstream stainless steel manufacturers may not significantly reduce production. Instead, it suppresses prices on raw materials, putting pressure on nickel prices.

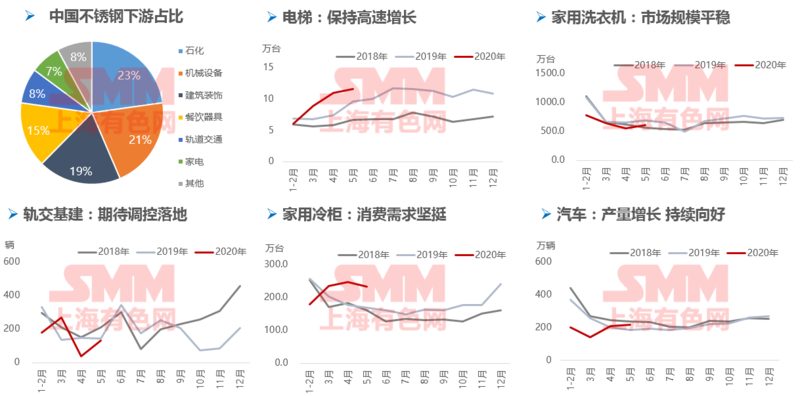

The downstream consumption structure of stainless steel is scattered and widely distributed in public and civil fields.

China's stainless steel consumption side in 2020: month-on-month improvement is still lower than that of last year due to the drag in the first quarter.

The torrential rain in the south has become a periodic factor in the lack of goods in the market since July:

According to data released by the government, in the first half of 2020, the national average precipitation (275.9 mm) was 7% higher than that in the same period of the normal year, and the first flood season in South China (March 25) and the Jiangnan Meiyu season (June 1) were 12 days and 7 days earlier than usual. A total of 14 regional torrential rains occurred.

The rainstorm weather in the south has become a phased factor for the lack of delivery in the stainless steel market recently.

According to traders' response, rainy days will have some impact on stainless steel transportation, spots will be formed on the surface drenched by rain, and delivery of goods with higher requirements on the surface will be restricted.

The plates with better consumption of stainless steel are scattered in many fields, such as urban construction, environmental protection, smart home and so on.

According to the survey, in 2020, the areas supporting the recovery of China's stainless steel consumption are also scattered, including urban construction, environmental protection, smart home and other areas.

1. Urban construction: the total output value of China's construction industry in the first half of 2020 was 10.084 trillion yuan, an increase of 0.77% over the same period last year, while stainless steel is the application of consumption upgrading in architectural decoration, elevators, water supply systems, public facilities, roofs, bridges and so on. With the development of the city, its consumption is relatively good.

2. Environmental protection: mechanical equipment is also the main application field of stainless steel, among which environmental protection-related equipment still has a good growth rate.

3. High-end home appliances: although the home appliance industry is a traditional industry with stable scale, part of the high-end smart home market is still booming. During the epidemic, the growth of refrigerators and freezers is the smallest in the whole industry during the horizontal comparison of white electricity. after the impact of the epidemic, the scale of the cold industry is still relatively stable. The centralized purchasing and hoarding behavior of the whole people during the epidemic has made consumers more eager for large capacity than ever before.

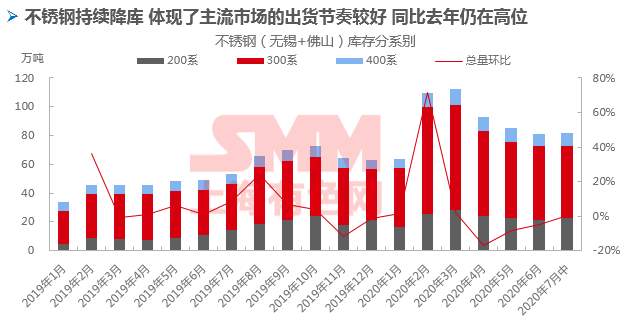

The decrease of stainless steel social circulation and the change of inventory data are the result of the increase of industrial chain concentration and the thinning of profit link.

Stainless steel factory increases shop area Wuxi Foshan market trader standing inventory decreases:

According to SMM research, this year, stainless steel giant enterprise shop mode has changed, from the original Wuxi and Foshan two major markets to shop goods all over the country, stainless steel market share in other areas is small and scattered, not easy to observe, such as Guangdong except Foshan other cities (Yangjiang, Guangzhou, Shenzhen, Jieyang), Fujian market, Zhejiang market, northern Jiangsu market, Shandong market and so on.

In addition, from the perspective of traders, the market has fluctuated greatly in recent years, bearing the risk of shipments while the profit situation is not ideal, so its standing inventory is gradually reduced, light.

Take a large stainless steel processing enterprise in Wuxi region surveyed by SMM as an example, the average monthly purchase volume is about 150000 tons, which is usually kept in stock for half a month to one month, but this year the Spring Festival reserve volume has gradually decreased and converted to on-demand procurement, with inventory only accounting for about 1/3 of the monthly usage.

Large stainless steel mills develop cold rolling end business and enter the market with fewer steel coils:

Steel mill order mode, gradually turn to the plate-based trend, the limited sale of steel coil, reduce the amount of steel coil agent.

Fujian Yongjin 304 will follow the July futures report of 13100 Mao base, and the quantity is to be approved. Terms of order: only after being processed by the agent (slicing, Kaiping) can the goods be shipped, and the whole volume shipping order will not be accepted for the time being.

Through the implementation of this operation, the source of goods is more sold by flat plates, which is closer to the links of downstream users, and the circulation links of steel coils among intermediate traders become less.

The recessive of dominant inventory exists in steel mills and processing plants in different degrees:

According to the SMM survey, in recent months, the output of domestic stainless steel plants has gradually increased, and the theoretical supply continues to be sufficient, while the market has a small supply of goods, mainly because the steel mills have increased the trade mode of direct supply channels, and the volume of circulation to the market is less.

Practitioners of mainstream warehousing enterprises in Wuxi market also said that due to the increase in the proportion of direct supply of steel mills, the business volume of warehousing companies has also been significantly affected.

SMM believes that due to the continuous pressure on stainless steel profits, steel mills tend to minimize the existence of intermediate links in order to ensure their own more profits, and the function of Wuxi market as a distribution center has been weakened. However, this phenomenon is not obvious for the Foshan market, which is located in the main place of consumption, with a large number of customers, and the actual operation of a large number of direct supply is not strong. And a lot of goods sent by water still need to rely on local private warehousing companies for transit.

Since the launch of SHFE, the number of stainless steel warehouse receipts has remained low:

The last period of deliverable stainless steel products are 304stainless steel coil, the registered brand's 304cold rolling output is around 25-300000 tons per month, accounting for about 1/4 to 1/3 of the total 300 series stainless steel; but the steel coil enters the market less, and most of the output is concentrated in individual enterprises. the number of warehouse deliverables has remained low since it was put on the market.

Quarterly balance data of stainless steel in China: the overall trend in the third and fourth quarters is mainly tight balance / small surplus.

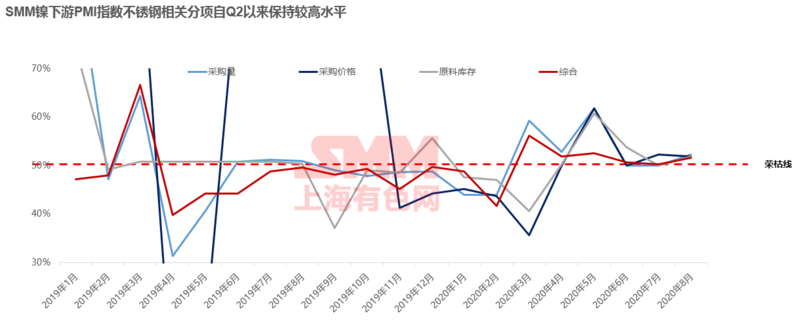

According to the stainless steel PMI purchasing index, the demand for nickel raw materials in mainstream stainless steel factories is stable.

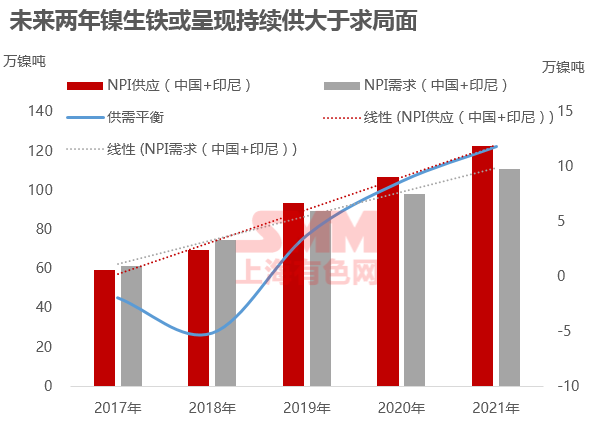

With the active production of nickel pig iron project in Indonesia, there must be more nickel pig iron surplus in the second half of the year. The actual surplus is related to the import volume.

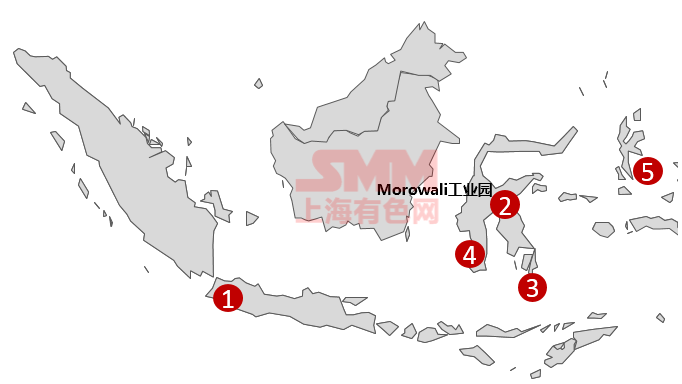

From the map, the nickel pig iron projects produced in Indonesia are mainly located in the five locations shown in the table, while the high-speed expansion projects are mainly Castle Peak morowali, Castle Peak Weda bay and Indonesia Delong.

Although the epidemic in Indonesia is also severe, the progress of nickel pig iron production has not been significantly affected, and the logistics of Indonesian nickel pig iron to China has been normal, and the production progress is slightly faster than expected; according to current estimates, the start-up of the new project makes the growth rate of supply faster than the growth rate of demand, and nickel pig iron will be in abundant supply this year and next year.

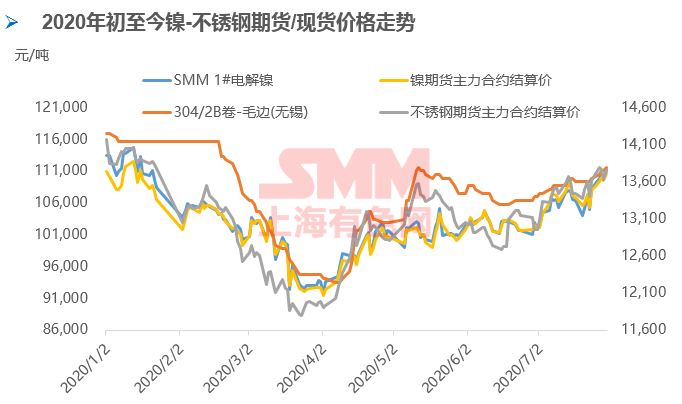

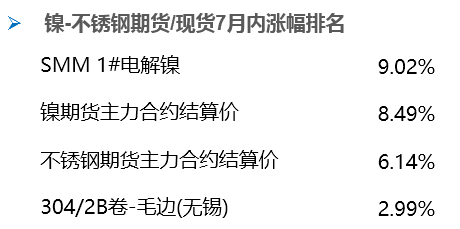

Judging from the recent price increase in the industrial chain, nickel is obviously ahead of all spot varieties and stainless steel spot is in a weak position.

SMM believes that the fundamentals of stainless steel spot are not excellent, but the marginal improvement is obvious, on the other hand, the recent strong trend is partly driven by futures (nickel and stainless steel contracts).

With the gradual abandonment of domestic monetary policy in the later period, the driving force on the capital side may not last and will also affect the mentality of the spot market.

Under the pressure of high inventory and low profit, the stable production of steel mills in the second half of the year will depend on the sustained low price of raw materials. Under the condition that the raw materials of nickel pig iron are sufficient, the steel mill is more likely to maintain normal operation.

The performance of the industrial chain will be stable in the second half of the year, and if the futures price returns to rationality in the later period, the spot price will fall limitedly. We expect the range of 304x2B stainless steel in the second half of 2020 to be 13300-14500 yuan / ton. (2mm, cold rolling coil price)

Main conclusion

The consumption performance of stainless steel in China has adapted to the latest economic situation. The overall performance of the whole year is better than expected. The rigid demand for nickel raw materials can be supported, but it is difficult to become the pillar of rising nickel prices.

From the perspective of global economic performance in the context of the epidemic, China outshines others, while China's stainless steel industry is also dominated by domestic demand, and the impact of external shocks is relatively not obvious.

In recent years, the development of China's stainless steel industry is characterized by continuous expansion of output, fierce competition, increased enterprise concentration and high profit pressure of steel mills, which has promoted the changes in the field of stainless steel circulation.

The shape of the stainless steel circulation field has changed, which avoids the potential problems caused by over-reliance on market circulation, and the inventory concentration in the circulation field is also declining, which is conducive to the improvement of industry profits.

From the perspective of real consumption, China's stainless steel consumption first suppressed and then rose in 2020, and some sectors have recovered better since the second quarter, but the consumption growth rate for the whole year is still negative, among which 300 series is relatively good.

Profits have gradually improved recently, and stainless steel plants are expected to have a strong intention to maintain stable production this year, and the rigid demand for nickel raw materials can support it. However, the recent rise in stainless steel prices, in addition to their own shipments, is also affected by the impact of nickel prices and funds, rather than stainless steel taking the initiative to lead nickel prices. For the lower reaches of nickel, the current nickel price is still on the high side. For stainless steel plants, the supply of nickel pig iron in the second half of 2020 is also very abundant, so if the later period of nickel returns to rationality according to the fundamentals, stainless steel demand for nickel will be a bottom support, but will not become a pillar of high nickel prices.

"SMM online Q & A" has come to the market, price, information if you have any questions, feel free to ask!

Scan the QR code and join the SMM metal communication group.

![[SMM Analysis]: Slower-than-Expected Progress in RKAB Approvals, Coupled with Disruptions from the Rainy Season in the Philippines and Indonesia, Drove Stronger Premiums Amid Regional Supply Uncertainty](https://imgqn.smm.cn/usercenter/CWsEw20251217171732.jpeg)

![[SMM Analysis] Weak End-User Demand but Firm Costs, High-Grade NPI Prices Rose Steadily](https://imgqn.smm.cn/usercenter/GmHLU20251217171733.jpg)