SMM7 March 20: July 20, "2020 China Ni-Cr stainless Steel Industry Market and Application Development Forum" held by SMM in Wuxi, at which SMM senior nickel analyst Liu Yuqiao analyzed the market and market prospect of China's Ni-Cr stainless steel industry chain in 2020.

The output of stainless steel in China is supported by the rapid recovery of raw materials from the epidemic.

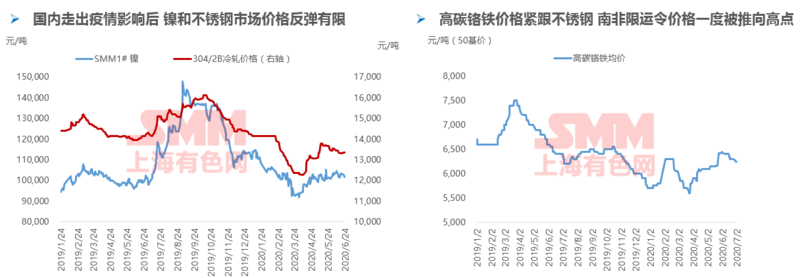

Epidemic situation and Ni-Cr stainless steel industry chain: affected by the epidemic, prices fell comprehensively in the first quarter and rebounded limited after coming out of the epidemic. Before the Spring Festival holiday, nickel prices, which have been weak since the fourth quarter of last year, once stopped falling, mainly because stainless steel production was reduced and went to the warehouse to see results. However, during the Spring Festival, the new crown epidemic broke out in China, and the prices of most metal varieties fell sharply, and nickel prices also fell.

When the supply side returns to the city after the festival, the supply side recovers quickly from the epidemic, but both the logistics link and the consumer side recover slowly, and the price of stainless steel is extremely high, and the price of stainless steel falls sharply; the price of crude oil also falls sharply, dragging down the trend of all metals, and the price of nickel is hit again, but there are signs of improvement in fundamentals, and prices are gradually bottoming out.

Domestic stainless steel production returned to normal, supporting the consumption of nickel and chromium raw materials obviously, and the fundamentals of domestic primary nickel and high-carbon ferrochromium improved in the second quarter. Despite the rebound and concussion, nickel and ferrochromium barely returned to their January positions, while stainless steel prices were weaker.

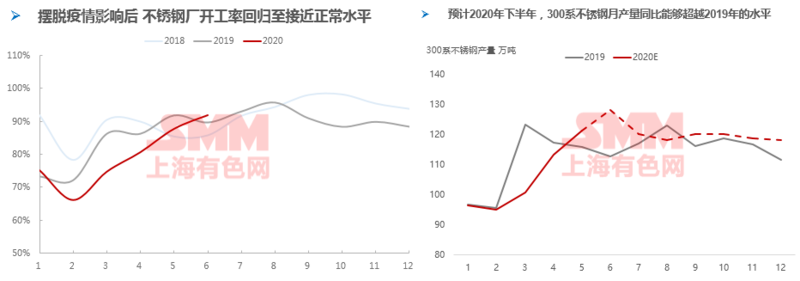

Stainless steel got rid of the influence of the epidemic earlier and returned to the normal operating rate level to provide bottom support for primary nickel demand.

The picture on the left shows the operating rate of domestic stainless steel plants. It can be seen that during the epidemic period, the operating rate of the stainless steel industry decreased significantly compared with previous years, while the operating rate of the stainless steel industry from April to May has gradually returned to the normal level.

The picture on the right shows the output of 300 series stainless steel plants in China, which directly affects the domestic consumption of primary nickel. It can be seen that from April to May, the output of 300 series has hit a new high again, and then stabilized at a high level. It is also expected that the year-on-year output in the second half of the year will be higher than that in the same period last year. This will provide some support for the demand for nickel series raw materials. As mentioned earlier, due to the impact of the epidemic, the consumption of stainless steel is slightly weak this year, which is a major negative factor, but in the range where the nickel price is already low, the supply of raw material nickel pig iron is also sufficient, and mainstream stainless steel manufacturers may not significantly reduce production. However, the price of raw materials is still depressed, putting pressure on the price of nickel.

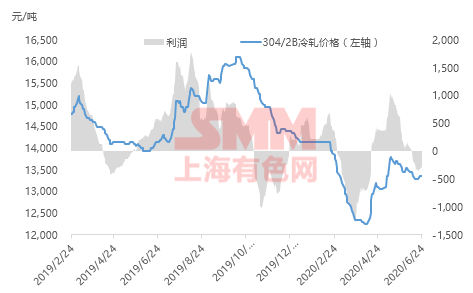

Under the situation of fierce competition, the profit situation of steel mills varies greatly, but it also ensures the demand of the raw material market.

Under the caliber of cash cost statistics, according to the inventory price accounting of raw materials, the national average profit of 304x2b cold rolled stainless steel changed from profit to small loss in June, on the one hand, due to the gradual strengthening of raw material prices, the production cost of stainless steel increased, on the other hand, stainless steel prices gradually fell after reaching a higher level in May, with a profit loss of about 200 yuan / ton at the beginning of July.

There are more projects to be put into production in the future, the competition pattern will remain fierce, profits are expected to remain low, and for nickel-chromium raw materials, while being supported by demand, prices will also be under pressure.

Average profit of Series 300 stainless steel industry: return to a small loss in the near future during the profit period from mid-April to early June

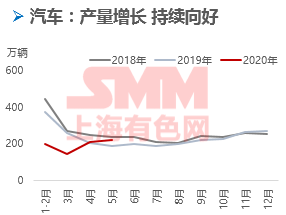

An overview of the situation downstream of stainless steel: month-on-month recovery is remarkable compared with the same period last year.

In May 2020, automobile production and sales reached 2.187 million and 2.194 million respectively, up 4.0 per cent and 5.9 per cent month-on-month, and 18.2 per cent and 14.5 per cent respectively over the same period last year. The double growth of automobile production and sales also means that the current situation of the automobile industry continues to improve.

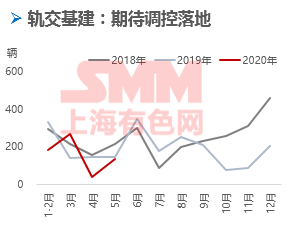

In May 2020, the national output of EMU was 131, a slight decrease of 7.7% compared with the same period last year. With the orderly progress of the resumption of work and production in the second quarter, rail transit infrastructure as one of the starting points of counter-cyclical regulation, related projects are speeding up the landing.

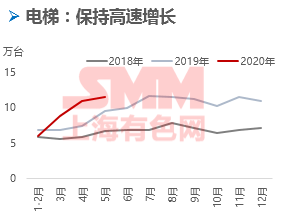

In May 2020, China produced 116000 elevators, escalators and elevators, an increase of 10.5 percent over the same period last year. Due to the rapid development of industries such as real estate and urban public infrastructure, China's newly installed elevator market has maintained rapid growth.

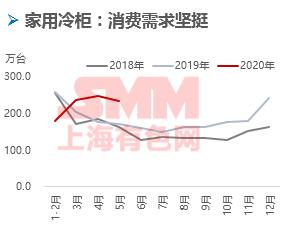

In May 2020, the national output of household freezers (household freezers) was 2.341 million, an increase of 47.5% over the same period last year. During the epidemic period, in the horizontal comparison of white electricity, the growth of refrigerators and freezers is the smallest decline in the whole industry, and the scale of the cold industry is still relatively stable after the impact of the epidemic. The centralized purchasing and hoarding behavior of the whole people during the epidemic has made consumers more eager for large capacity than ever before.

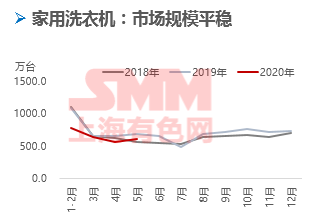

The national output of household washing machines decreased slightly in May 2020, and the national output of household washing machines in May 2020 was 6.083 million, down 8.2% from the same period last year. The overall scale of the washing machine market is relatively stable in recent years, and the main development trend in the future is the transformation of low-end products to middle and high-end products.

300 series stainless steel maintains considerable demand for nickel, but mainly benefits Indonesian nickel pig iron plant.

Review of Nickel Price trend: the rebound of Nickel Price after the epidemic is limited

Before the Spring Festival holiday, the price of nickel, which has been weak since the fourth quarter of last year, once stopped falling, mainly due to the reduction of stainless steel production. However, during the Spring Festival, the new crown epidemic broke out in China, and the prices of most metal varieties fell sharply. Nickel prices also fell.

When the supply side returns to the market after the second festival, the supply side recovers quickly from the epidemic, but both the logistics link and the consumer side recover slowly, the stainless steel stock is extremely high, and the price of stainless steel falls sharply; the price of crude oil also falls sharply, dragging down the trend of all metals, and the price of nickel is hit again, but there are signs of improvement in fundamentals, and prices are gradually bottoming out.

(3) the domestic stainless steel production returned to normal, which obviously supported the consumption of primary nickel, coupled with a large reduction in production in domestic nickel pig iron plants, the fundamentals of domestic primary nickel improved in the second quarter.

(4) the production of Indonesian nickel pig iron is accelerated at a high speed, and the follow-up consumption of the stainless steel industry is not good after consuming the replenishment dividend at the initial stage of the recovery of the epidemic, but European and American countries are committed to recovering from the epidemic, economic data are improved, and nickel prices show a volatile trend under the long-empty interweaving.

Although experienced a rebound and shock, nickel prices still failed to return to January's high, that is, Shanghai nickel 113320 yuan / ton, Lunni 14395 US dollars / ton. (spot settlement price)

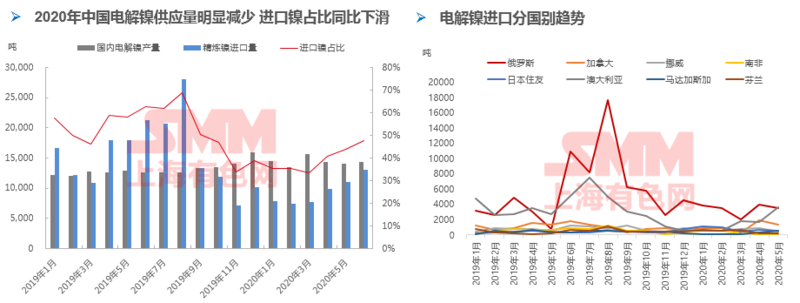

Nickel supply side: imports of pure nickel decreased compared with the same period last year.

As can be seen from the picture on the left, the supply of electrolytic nickel in China decreased significantly in 2020 compared with last year, mainly due to a reduction in the amount of imported electrolytic nickel; the output level of domestic manufacturers is relatively stable.

The import of electrolytic nickel in China has dropped from 10-20 000 tons per month to only about 4000 tons per month, reflecting a significant decline in domestic demand, which is caused by more use of nickel pig iron instead of electrolytic nickel in 300 series stainless steel plants.

As can be seen from the chart on the right, Russian nickel, which is mostly used in stainless steel, still occupies an important position in China's electrolytic nickel imports, but the quantity is much lower than before; pure nickel imported from Australia, mainly nickel beans, is used in stainless steel plants and nickel sulfate plants, with a high correlation between demand and performance-price ratio, and monthly imports fluctuate greatly, with an average of 20003,000 tons per month.

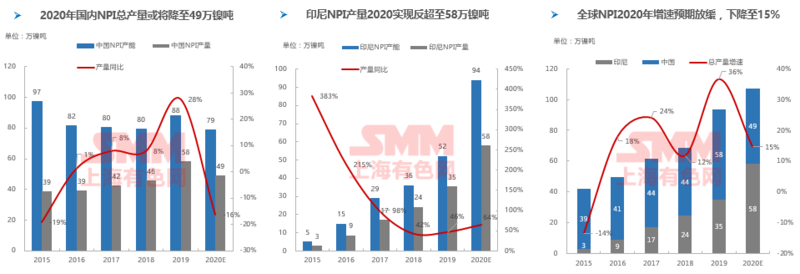

The substitution of Indonesian nickel pig iron to domestic nickel pig iron will further occur in 2020.

From the production capacity and production data and expectations of nickel pig iron, the replacement of Indonesian nickel pig iron with domestic nickel pig iron will further occur in 2020. After the increase in Indonesian nickel pig iron production makes up for the reduction in China, the total volume maintains growth, but the growth rate slows down to 15%.

SMM statistics show that from January to June 2020, the cumulative output of Ferro Nickel in Indonesia was 254200 nickel tons, while that in China was 249900 tons. Indonesia's output exceeded that of Ferro Nickel and became the largest producer of Ferro Nickel.

SMM predicts that China's Ferro Nickel will drop to 490000 Nickel tons in 2020 from 580000 Nickel tons in 19 years, while Indonesia Nickel Iron will increase from 350000 Nickel tons in 19 years to 580000 Nickel tons in 2020.

Indonesia's production lines for commissioning and reaching production are still relatively dense in the third quarter. It is estimated that by the end of the third quarter, Indonesia's cumulative annual output will reach 409200 nickel tons, while China's annual output will reach 372900 tons. The output gap will widen, and the nickel-iron supply pattern will change.

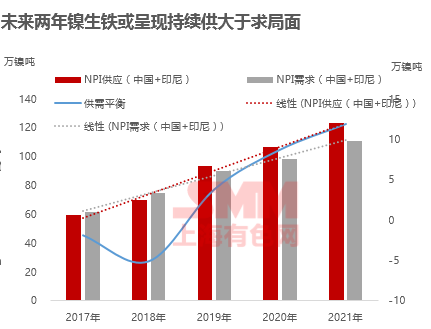

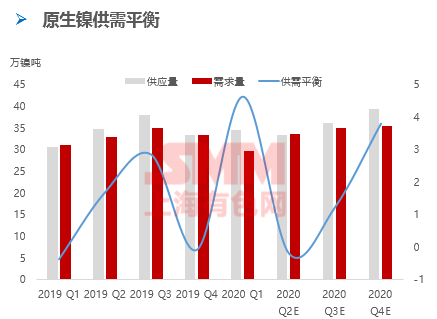

Balance sheet of supply and demand of nickel pig iron: Indonesia's rapid production surplus has increased in the third quarter and will be more surplus in the third quarter than in the second quarter.

Although the epidemic in Indonesia is also severe, the progress of nickel pig iron production has not been significantly affected, and the logistics of Indonesian nickel pig iron to China has been normal, and the production progress is slightly faster than expected; according to current estimates, the start-up of the new project makes the growth rate of supply faster than the growth rate of demand, and nickel pig iron will be in abundant supply this year and next year.

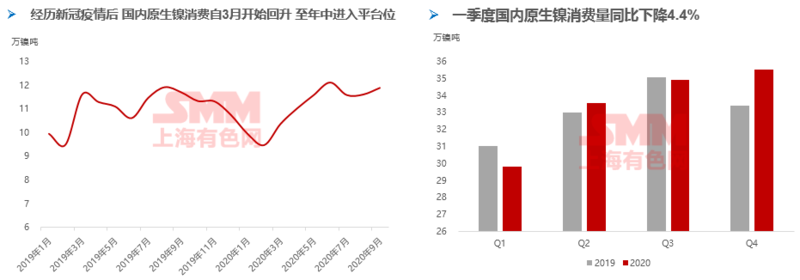

Overview of China's Primary Nickel consumption in 2020: domestic Primary Nickel consumption will gradually pick up after the first quarter

Except that the monthly consumption of primary nickel in China was affected by the Spring Festival and the epidemic in the first quarter, the normal level is about 11-120000 nickel tons per month. The biggest factor affecting the consumption of primary nickel is the production of stainless steel plants, which is huge and stable most of the time.

In 2020, since the middle of the year, the growth rate of domestic primary nickel consumption has entered the platform to show a fluctuating trend, and after recovering from the epidemic, the dividend of replenishment in the lower reaches has gradually faded, and the market in the second half of the year will be more in line with the actual consumption situation downstream.

In terms of quarterly consumption, if the production of domestic stainless steel plants can remain normal, and considering the slow recovery of other nickel downstream, consumption in the fourth quarter of this year will increase slightly compared with the third quarter; the collapse in prices in the fourth quarter of last year is related to the strong intention of stainless steel to go to the warehouse and reduce production to seek to improve profits. This year, the consumption end of stainless steel is slightly weak, which is a major negative factor, but the price of nickel is already in a low range, the supply of raw material nickel pig iron is also sufficient, and the mainstream manufacturers of stainless steel may not significantly reduce production, while the price of raw materials is still depressed, putting pressure on the price of nickel.

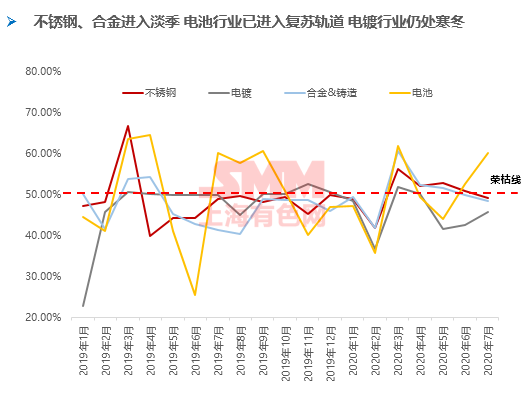

Nickel downstream PMI interpretation: stainless steel and alloy have entered the off-season battery industry and entered the recovery track electroplating industry is still in a cold winter.

Stainless steel: the PMI composite index of the stainless steel industry in July was 49.45%, down 0.81% from the final value in June and below the rise and fall line. The researchers believe that after the domestic epidemic gradually got rid of the influence of the epidemic in the second quarter, the replenishment of the intermediate link and downstream enterprises was basically completed, and after that, there was no new positive appearance in the market for the time being, and the overall consumption form itself was relatively weak in the second half of the year. In July, as a traditional off-season, the overall supply exceeds demand pattern will be more obvious.

Battery: the initial value of the battery industry PMI composite index in July was 60.11%, up 7.59% from the final value in June and higher than the rise and fall line. Due to the stimulation of consumption encouragement policies in Europe and the United States, there has been a certain pick-up in overseas terminal market consumption, resulting in an increase in orders for precursor high-nickel products, ternary material factories and the purchase of raw materials; while the performance of the Ni-MH battery industry is mediocre, except that the leading enterprises have gradually returned to normal, the orders of other peer enterprises have not recovered significantly. Some surveyed companies said that the order situation will continue to improve in July, while for poorer companies, it will only maintain the previous level and will not worsen further, so the battery industry is expected to improve in July compared with June.

Alloy casting: the initial value of the PMI composite index of the alloy industry in July is 48.24%, which is expected to decrease by 0.52% compared with the final value in May, and is expected to remain below the rise and fall line. Among them, the production index dropped to 48.31%, mainly due to environmental protection factors in North China, and some special steel plants are expected to start overhauling one after another in July, which may have a greater impact on the alloy casting production line. The index of new orders fell to 46.02%, and more operators said that after entering the off-season of terminal consumption, the number of orders received in July may be lower than that in the previous period. The raw material index is 46.57%, and the purchasing volume index is 48.76%, which is also correspondingly lowered due to the manufacturer's production schedule.

Electroplating: the initial value of the PMI composite index of the electroplating industry in July is 45.60%, which will still be lower than the rise and fall line. Among them, the production index is 42.06%, and the new order index is 43.74%. After entering the traditional off-season of electroplating, in addition to local environmental protection requirements, it is also affected by high temperature power transfer, so the electroplating industry is more pessimistic about July. At the same time, procurement volume and raw material inventory also dropped to 45.59% and 46.36% due to low operating rate.

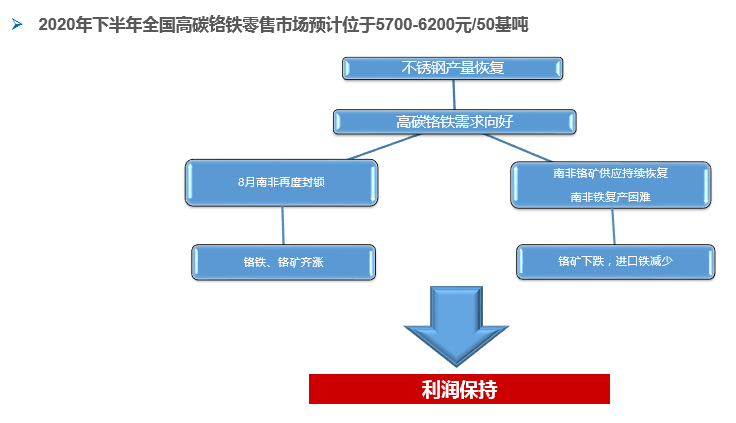

The balance of supply and demand of ferrochromium has been passively improved due to the chrome mine incident in South Africa, but the competition is still fierce in the

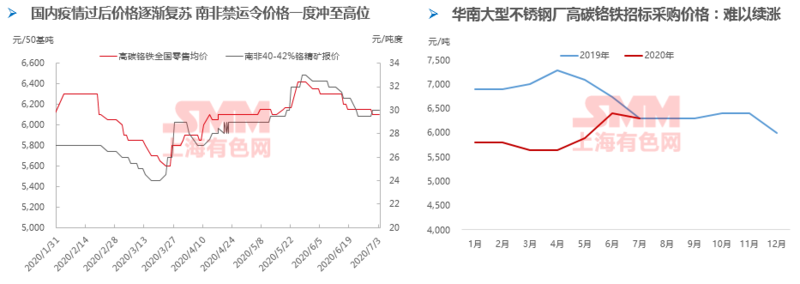

Review of Chromium prices: prices gradually recover after the domestic epidemic. The South African embargo pushed prices to a high at one point.

On the eve of the Spring Festival in 2020, the price of high-carbon ferrochromium has increased slightly due to the demand for stock in the downstream stainless steel factories, but the epidemic has led to a "weak supply and demand" in the manufacturing industry across the country, which has greatly suppressed the price of high-carbon ferrochromium. With the gradual improvement of the domestic epidemic situation and economic situation, the downstream stainless steel market has entered a cyclical peak season, and the price of high-carbon ferrochromium began to pick up.

On March 26, the multinational blockade policy in South Africa brought great uncertainty to the future supply of chromium ore and ferrochrome. The price of ferrochrome rose sharply driven by the price of upstream chromium ore. The retail market price of high carbon ferrochromium rose by about 18%. The bidding price of mainstream stainless steel factories increased by 7.24% from the previous month, and the largest increase of 13.27% during the year.

The impact of the South African incident is still fermenting, but the market has gradually returned to rationality, with the tender price of steel mills falling by 100 yuan / ton in July.

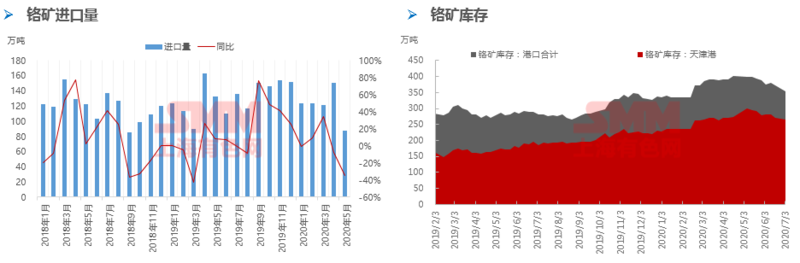

Chrome ore: imports have declined since April due to the South African embargo. Port chrome ore stocks have fallen for eight consecutive weeks.

At the beginning of 2019, the inventory of chromite in China continued to rise, and the highest inventory in history continued to be breached. During the year, the national inventory of chromite increased by 178000 tons compared with the same period last year, while the price of chromite also continued to fall. During the year, 40 per cent of chromite concentrate in South Africa fell by about 16 per cent.

As the Spring Festival entered at the beginning of 2020, the start of construction downstream decreased, and the epidemic delayed the procurement demand for chromium ore in chromite, and the national inventory continued to accumulate, reaching an all-time high of 4.1 million tons in mid-April. however, many countries in South Africa and Zimbabwe imposed a blockade on March 26th due to the impact of the epidemic. Taking the 40-day shipping period as a reference, the arrival of chromium mines in China decreased as scheduled in late April, and the national chromium ore inventory basically decreased for eight consecutive weeks. As of July 3, the national port inventory of 3.53 million tons.

As the impact of the South African embargo is still fermenting, South African ports are inefficient, and it is expected that it will take some time for chromium ore imports to fully return to normal, possibly until August.

Ferrochromium: changes in domestic supply mainly follow the demand for stainless steel production, but the South African embargo has an impact on import supply.

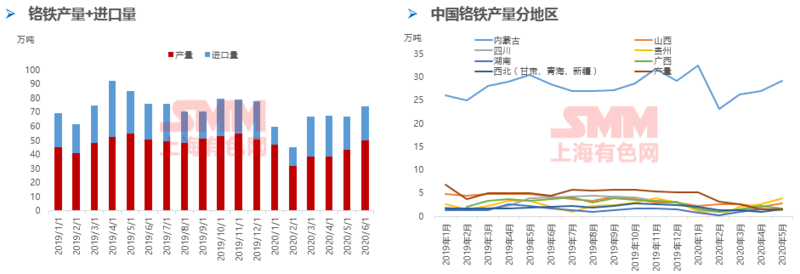

The increase or decrease of high-carbon ferrochromium supply is fully in line with the stainless steel demand cycle, but this year's high-carbon ferrochromium production affected by the epidemic led to an extremely slow resumption of work in February. From February to April, the national average monthly output of high-carbon ferrochromium decreased by 12.13% compared with the same period last year, and the average monthly total supply decreased by 21.58%.

Among them, imports of ferrochromium are affected by blockades by South Africa, Oman, Zimbabwe and other countries. From January to June 2020, imports of high-carbon ferrochromium are expected to be 1.31 million tons, a decrease of 21.55 percent over the same period last year.

In June, the output of domestic high-carbon ferrochromium surged to 498900 tons, an increase of 15.92% from the previous month, a decrease of 1.01% compared with the same period last year, and supply recovered sharply, but the impact of the epidemic in South Africa led to the slow resumption of production of imported ferrochromium enterprises led by Glencore, and the South African region entered winter in July. The rise in electricity prices has led South Africa's iron and mines to enter a cyclical reduction in production, and under double pressure, the overall national supply of ferrochromium may still be lower than last year. There is a big fix for the oversupply in 2019.

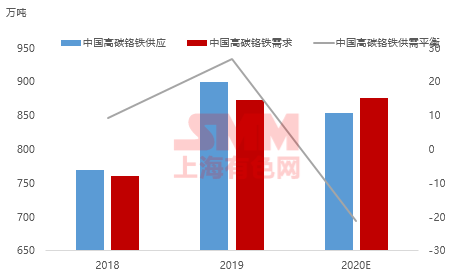

It is estimated that the balance of supply and demand of high-carbon ferrochromium in China will have an annual gap of 213400 tons in 2020 to significantly improve the situation of oversupply in 2019.

Downstream stainless steel has increased significantly since April, while the operating rate of domestic high-carbon ferrochrome in that month was only 48.6%. On March 26, due to the national blockade imposed by South Africa and other countries due to the epidemic, the supply of imported chromite and chromite decreased by more than 20% compared with the same period last year. And the South African government expects to enter the outbreak period in September, when the supply of South African chromite and chromite may be under pressure again.

Under the influence of the epidemic, SMM believes that both domestic production of high-carbon ferrochromium and imported ferrochromium will show negative growth in 2020, and the annual gap between supply and demand of high-carbon ferrochromium in China will be 213400 tons, which will greatly improve the situation of oversupply in 2019.

It is expected that both nickel and stainless steel prices will fluctuate widely. Ferrochromium prices are relatively stable. The price center of gravity in the second half of the year is better than that in the first half.

SMM expects nickel and stainless steel prices to have wide volatility, ferrochromium prices are relatively stable, and the price center of gravity in the second half of the year is higher than that in the first half of the year as a whole.

Quarterly balance sheet: with the increase in the amount of ferronickel returned to Indonesia, the balance sheet of domestic primary nickel supply and demand gradually tends to be loose, but it will not be worse than in the first quarter; in addition, most of the excess range is still dominated by nickel pig iron imports. the actual performance of nickel price also needs to consider the impact of macro factors on the environment of pure nickel consumption.

Annual balance sheet: affected by the epidemic and the rapid commissioning of NPI in Indonesia, the excess supply of primary nickel in China in 2020 is significantly higher than in previous years.

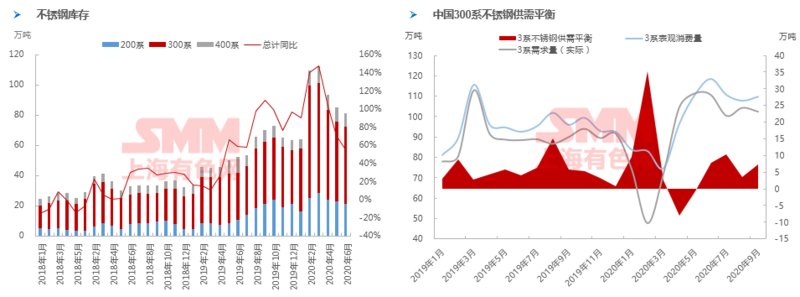

Stainless steel: the trend of going to the warehouse slows down the market and re-enters the situation of small surplus.

After the domestic epidemic, the downstream replenishment demand supports the high and downward inventory, while after the replenishment dividend, the supply continues to exceed demand under the existing domestic demand situation, and the subsequent stainless steel inventory or stop reducing the warehouse even appears the situation of base warehouse.

Under the pressure of high inventory and low profit, the stable production of steel mills in the second half of the year will depend on the sustained low price of raw materials. Under the condition that the raw materials of nickel pig iron are sufficient, the steel mill is more likely to maintain normal operation.

Market Prospect of High-carbon Ferro-Chromium in the second half of 2020: prices fall slightly and profits are expected to pick up

Scan the code and apply to join the SMM Ni-Cr stainless steel AC group.